Advertisement

- Australia

- /

- Trade Distributors

- /

- ASX:REH

Is Undervaluation and Profit Growth Potential Altering the Investment Case for Reece (ASX:REH)?

Simply Wall St

Reviewed by Sasha Jovanovic

- Recent analysis highlights Reece Limited is trading below its intrinsic value, with profit projected to grow by 23% in coming years.

- This combination of perceived undervaluation and strong profit outlook has drawn heightened investor interest in the company.

- We'll explore how signs of undervaluation and a robust profit growth forecast could influence Reece's investment narrative going forward.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Reece Investment Narrative Recap

To be a Reece Limited shareholder, you need to be confident in the company's ability to recover margins and return to profit growth, particularly as it leverages ongoing investments in digital initiatives and U.S. expansion. The recent news of Reece trading below intrinsic value with a projected 23% profit growth is significant, but it does not override the immediate risk from continued softness in the core end markets, especially given lingering challenges in residential construction and related volume pressures. Among recent announcements, the share buyback program for up to A$400 million stands out as particularly relevant; it may provide some near-term support to the share price and signals confidence from the Board, but it does not directly address the headwinds facing earnings or market demand. However, investors should also be aware that near-term optimism is tempered by the reality of persistent revenue headwinds if core segments remain weak and...

Read the full narrative on Reece (it's free!)

Reece's narrative projects A$9.8 billion revenue and A$389.1 million earnings by 2028. This requires 3.1% yearly revenue growth and an earnings increase of A$72.2 million from the current earnings of A$316.9 million.

Uncover how Reece's forecasts yield a A$11.82 fair value, a 4% upside to its current price.

Exploring Other Perspectives

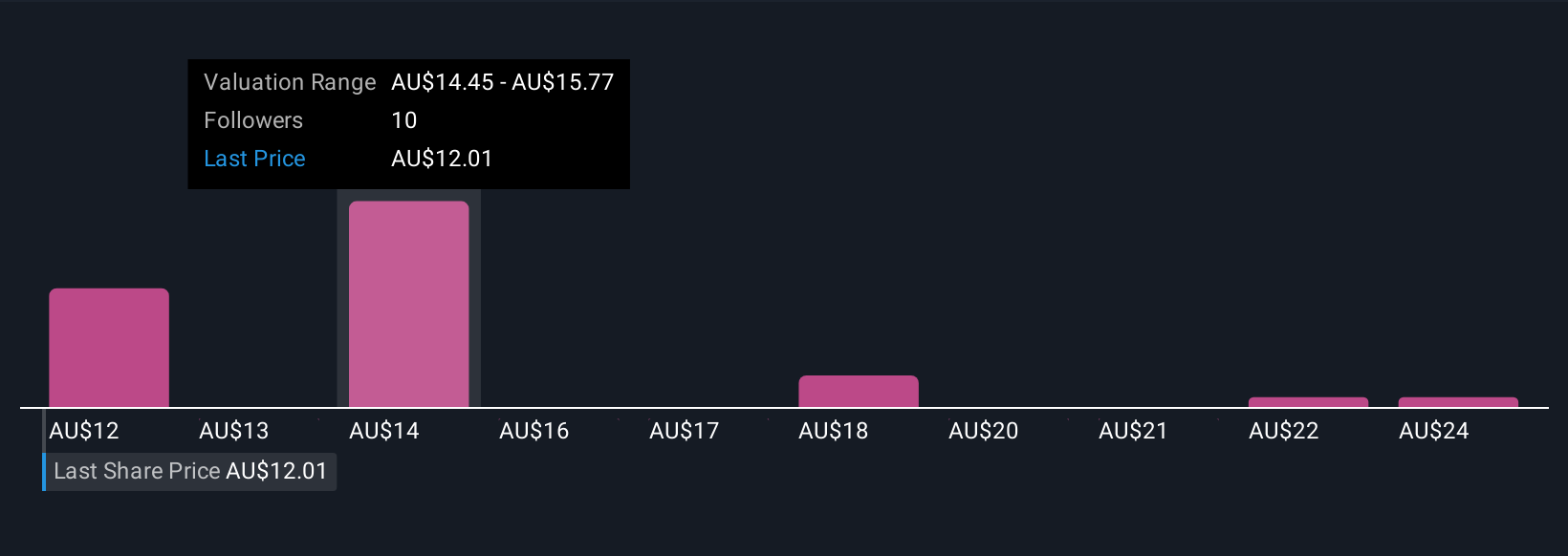

Fair value estimates from 5 Simply Wall St Community members span from A$11.82 to A$25.00 per share. These varied views stand alongside current analyst concerns about persistent core end market softness, reminding you to explore several alternative viewpoints.

Explore 5 other fair value estimates on Reece - why the stock might be worth just A$11.82!

Build Your Own Reece Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Reece research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Reece research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Reece's overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:REH

Reece

Engages in the distribution of plumbing, waterworks, heating, ventilation, air-conditioning, and refrigeration products to commercial and residential customers in Australia, New Zealand, and the United States.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor