- Australia

- /

- Diversified Financial

- /

- ASX:YBR

A Quick Analysis On Yellow Brick Road Holdings' (ASX:YBR) CEO Compensation

Mark Bouris is the CEO of Yellow Brick Road Holdings Limited (ASX:YBR), and in this article, we analyze the executive's compensation package with respect to the overall performance of the company. This analysis will also assess whether Yellow Brick Road Holdings pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

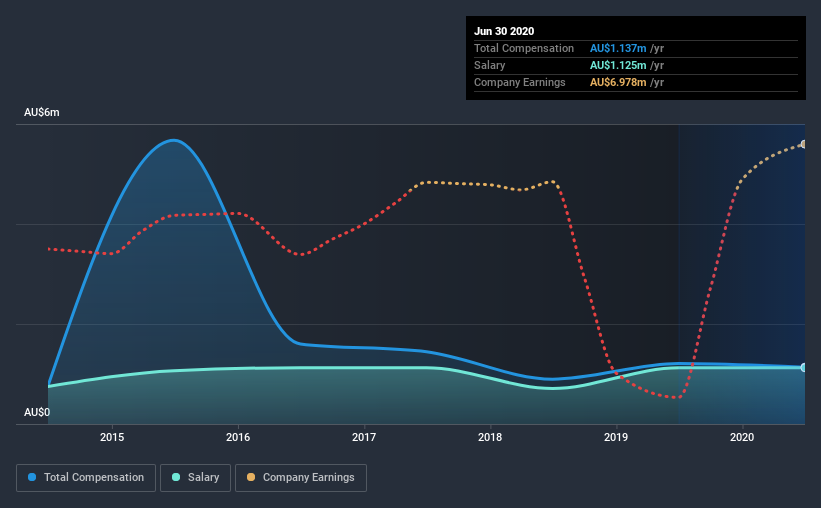

View our latest analysis for Yellow Brick Road Holdings

Comparing Yellow Brick Road Holdings Limited's CEO Compensation With the industry

At the time of writing, our data shows that Yellow Brick Road Holdings Limited has a market capitalization of AU$27m, and reported total annual CEO compensation of AU$1.1m for the year to June 2020. That's a slightly lower by 6.1% over the previous year. In particular, the salary of AU$1.13m, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations under AU$260m, the reported median total CEO compensation was AU$573k. This suggests that Mark Bouris is paid more than the median for the industry. What's more, Mark Bouris holds AU$334k worth of shares in the company in their own name.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | AU$1.1m | AU$1.1m | 99% |

| Other | AU$12k | AU$86k | 1% |

| Total Compensation | AU$1.1m | AU$1.2m | 100% |

Talking in terms of the industry, salary represented approximately 78% of total compensation out of all the companies we analyzed, while other remuneration made up 22% of the pie. Yellow Brick Road Holdings is focused on going down a more traditional approach and is paying a higher portion of compensation through salary, as compared to non-salary benefits. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Yellow Brick Road Holdings Limited's Growth

Yellow Brick Road Holdings Limited's earnings per share (EPS) grew 72% per year over the last three years. In the last year, its revenue is down 13%.

This demonstrates that the company has been improving recently and is good news for the shareholders. While it would be good to see revenue growth, profits matter more in the end. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Yellow Brick Road Holdings Limited Been A Good Investment?

Given the total shareholder loss of 45% over three years, many shareholders in Yellow Brick Road Holdings Limited are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Yellow Brick Road Holdings pays its CEO a majority of compensation through a salary. As we noted earlier, Yellow Brick Road Holdings pays its CEO higher than the norm for similar-sized companies belonging to the same industry. However, the EPS growth is certainly impressive, but we cannot say the same about the uninspiring shareholder returns (over the last three years). Although we'd stop short of calling it inappropriate, we think Mark is earning a very handsome sum.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We've identified 2 warning signs for Yellow Brick Road Holdings that investors should be aware of in a dynamic business environment.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you’re looking to trade Yellow Brick Road Holdings, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Yellow Brick Road Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:YBR

Yellow Brick Road Holdings

Yellow Brick Road Holdings Limited provides various financial services in Australia.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives