Advertisement

- United Arab Emirates

- /

- Insurance

- /

- DFM:NGI

National General Insurance (P.J.S.C.)'s (DFM:NGI) Dividend Will Be Increased To AED0.45

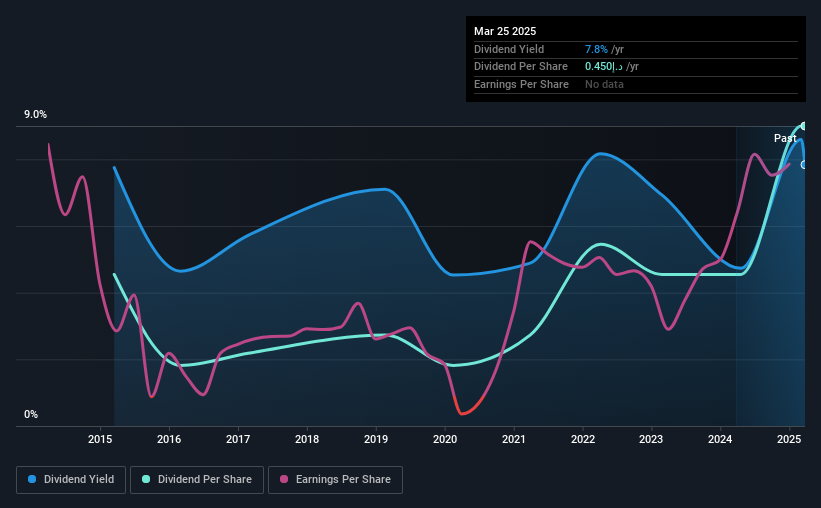

National General Insurance Co. (P.J.S.C.)'s (DFM:NGI) dividend will be increasing from last year's payment of the same period to AED0.45 on 1st of January. This will take the dividend yield to an attractive 7.8%, providing a nice boost to shareholder returns.

National General Insurance (P.J.S.C.)'s Payment Could Potentially Have Solid Earnings Coverage

If the payments aren't sustainable, a high yield for a few years won't matter that much. Prior to this announcement, National General Insurance (P.J.S.C.)'s dividend was only 58% of earnings, however it was paying out 277% of free cash flows. This signals that the company is more focused on returning cash flow to shareholders, but it could mean that the dividend is exposed to cuts in the future.

Looking forward, earnings per share could rise by 48.8% over the next year if the trend from the last few years continues. Assuming the dividend continues along recent trends, we think the payout ratio could be 41% by next year, which is in a pretty sustainable range.

View our latest analysis for National General Insurance (P.J.S.C.)

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2015, the annual payment back then was AED0.227, compared to the most recent full-year payment of AED0.45. This means that it has been growing its distributions at 7.1% per annum over that time. We like to see dividends have grown at a reasonable rate, but with at least one substantial cut in the payments, we're not certain this dividend stock would be ideal for someone intending to live on the income.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. National General Insurance (P.J.S.C.) has seen EPS rising for the last five years, at 49% per annum. National General Insurance (P.J.S.C.) is clearly able to grow rapidly while still returning cash to shareholders, positioning it to become a strong dividend payer in the future.

Our Thoughts On National General Insurance (P.J.S.C.)'s Dividend

In summary, while it's always good to see the dividend being raised, we don't think National General Insurance (P.J.S.C.)'s payments are rock solid. While National General Insurance (P.J.S.C.) is earning enough to cover the payments, the cash flows are lacking. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've identified 2 warning signs for National General Insurance (P.J.S.C.) (1 can't be ignored!) that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if National General Insurance (P.J.S.C.) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DFM:NGI

National General Insurance (P.J.S.C.)

Engages in underwriting various classes of life and general insurance, and reinsurance businesses in the United Arab Emirates.

Excellent balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|24.5% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|45.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|57.0% undervalued

AX

Community Contributor