Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:SMR

ASX Penny Stocks Spotlight: Generation Development Group And 2 More To Watch

Amidst a cautious atmosphere on the ASX, driven by geopolitical uncertainties, Australian shares have seen modest gains. In such a climate, investors often look beyond established giants to explore opportunities in lesser-known sectors. Penny stocks, while an older term, continue to represent smaller or newer companies with potential for growth and value; focusing on those with solid financials can uncover promising investment opportunities.

Top 10 Penny Stocks In Australia

| Name | Share Price | Market Cap | Rewards & Risks |

| West African Resources (ASX:WAF) | A$3.15 | A$3.6B | ✅ 5 ⚠️ 0 View Analysis > |

| LaserBond (ASX:LBL) | A$0.57 | A$67.37M | ✅ 4 ⚠️ 1 View Analysis > |

| Regal Partners (ASX:RPL) | A$2.50 | A$923.5M | ✅ 4 ⚠️ 2 View Analysis > |

| Praemium (ASX:PPS) | A$0.66 | A$321.73M | ✅ 5 ⚠️ 1 View Analysis > |

| Australian Ethical Investment (ASX:AEF) | A$4.45 | A$506.54M | ✅ 2 ⚠️ 1 View Analysis > |

| EDU Holdings (ASX:EDU) | A$0.75 | A$93.71M | ✅ 4 ⚠️ 1 View Analysis > |

| Integrated Research (ASX:IRI) | A$0.30 | A$54.18M | ✅ 3 ⚠️ 3 View Analysis > |

| Kingsgate Consolidated (ASX:KCN) | A$4.62 | A$1.23B | ✅ 3 ⚠️ 2 View Analysis > |

| CTI Logistics (ASX:CLX) | A$1.825 | A$143.26M | ✅ 4 ⚠️ 2 View Analysis > |

| Cogstate (ASX:CGS) | A$2.17 | A$371.05M | ✅ 4 ⚠️ 1 View Analysis > |

Click here to see the full list of 400 stocks from our ASX Penny Stocks screener.

We'll examine a selection from our screener results.

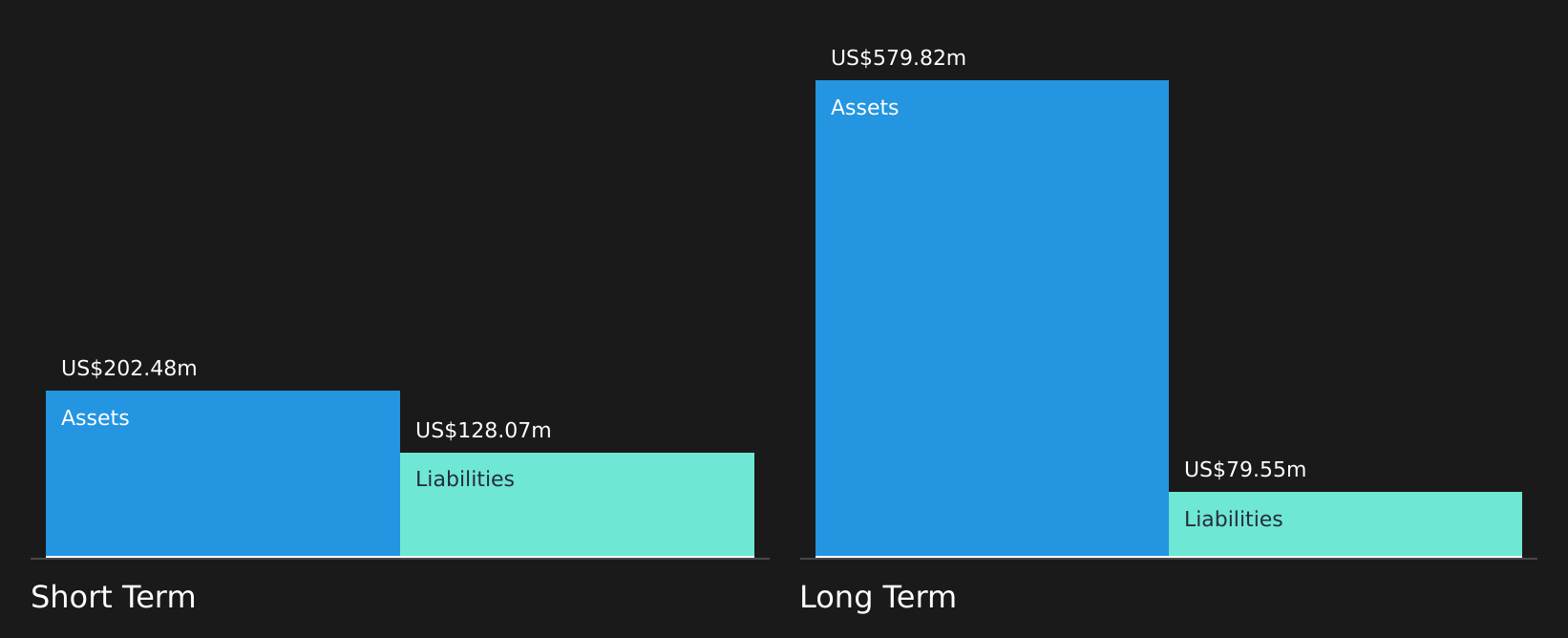

Generation Development Group (ASX:GDG)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Generation Development Group Limited operates in the diversified financial services sector in Australia with a market capitalization of A$1.64 billion.

Operations: The company generates revenue from its Benefit Funds segment, which amounts to A$423 million.

Market Cap: A$1.64B

Generation Development Group, with a market cap of A$1.64 billion, operates in the diversified financial services sector and is currently unprofitable. Despite this, analysts anticipate significant earnings growth at 44.11% annually. The company's debt is well-managed, covered by operating cash flow and EBIT, though its return on equity remains negative. Recent earnings showed a net income decline to A$6.85 million for the half-year ended December 2025 compared to the previous year’s A$78.88 million, yet it continues to distribute dividends with a recent fully franked dividend announcement of A$0.01 per share payable in April 2026.

- Dive into the specifics of Generation Development Group here with our thorough balance sheet health report.

- Evaluate Generation Development Group's prospects by accessing our earnings growth report.

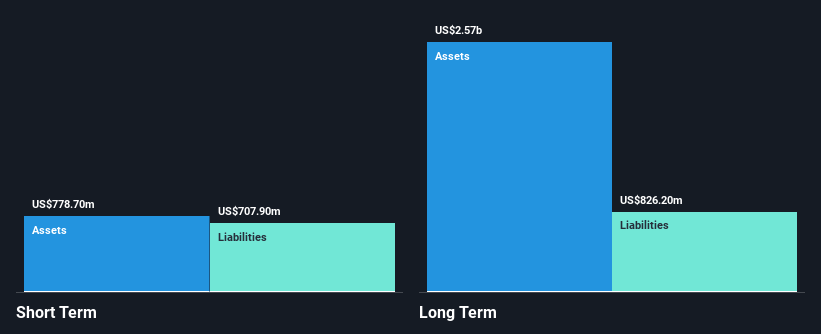

Mesoblast (ASX:MSB)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Mesoblast Limited, along with its subsidiaries, focuses on developing regenerative medicine products across Australia, the United States, Singapore, and Switzerland, with a market cap of A$2.83 billion.

Operations: The company generates $65.38 million from its cell technology platform development for commercialization.

Market Cap: A$2.83B

Mesoblast Limited, with a market cap of A$2.83 billion, is focused on regenerative medicine and has shown significant revenue growth, reporting US$51.34 million for the half-year ended December 2025 compared to US$3.16 million a year ago. Despite being unprofitable with a negative return on equity of -16.42%, it maintains more cash than total debt and has not diluted shareholders recently. The company anticipates Ryoncil net revenue between US$110 million and US$120 million for fiscal 2026, supported by FDA approval for pediatric use in steroid-refractory acute graft-versus-host disease and ongoing trials for adult applications.

- Click to explore a detailed breakdown of our findings in Mesoblast's financial health report.

- Learn about Mesoblast's future growth trajectory here.

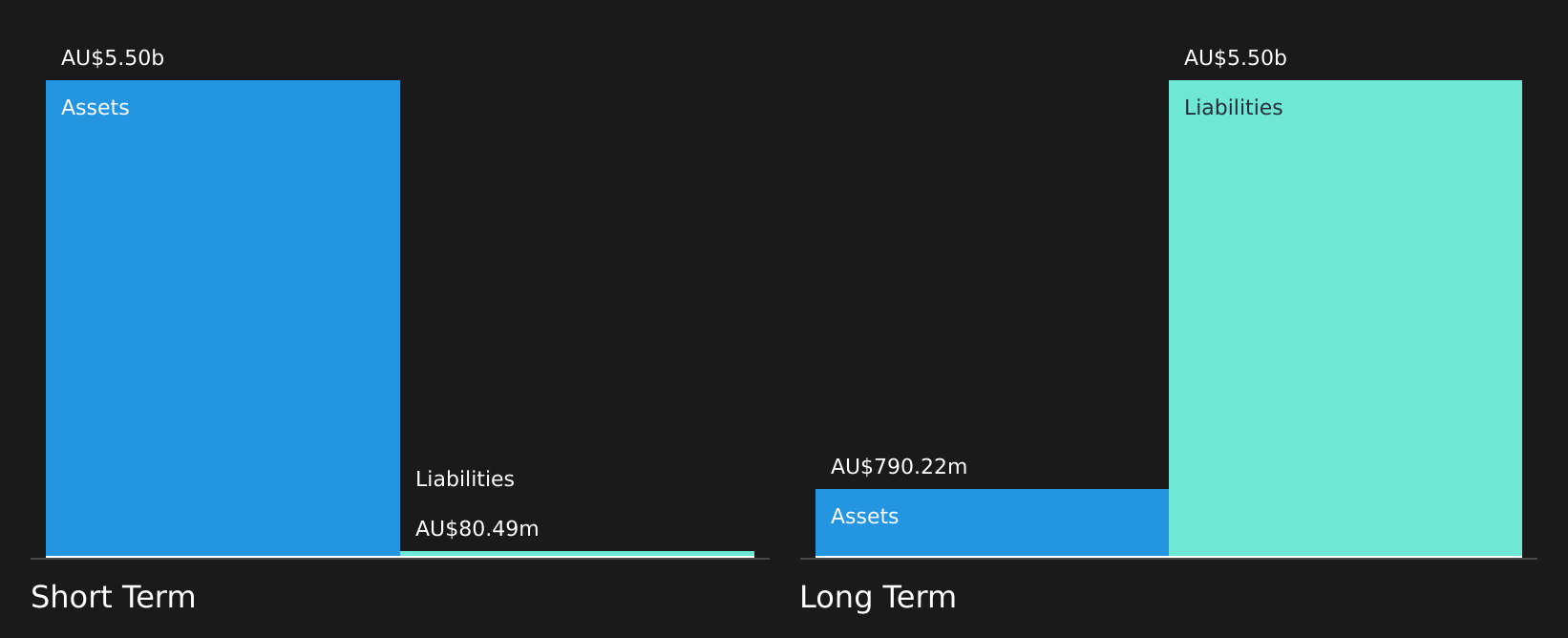

Stanmore Resources (ASX:SMR)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Stanmore Resources Limited is an Australian company involved in the exploration, development, production, and sale of metallurgical coal with a market cap of A$2.54 billion.

Operations: The company generates revenue of $1.88 billion from the production and sale of metallurgical and thermal coal.

Market Cap: A$2.54B

Stanmore Resources, with a market cap of A$2.54 billion, reported a net loss of US$47.2 million for 2025 despite generating US$1.89 billion in revenue from coal sales, reflecting a decline from the previous year’s figures. The company remains unprofitable with a negative return on equity but benefits from satisfactory debt levels and operating cash flow that covers its debt well. Although trading significantly below estimated fair value and not diluting shareholders recently, its dividend is not well covered by earnings. Production guidance for 2026 indicates stable operations with saleable production expected between 12.8 Mt to 13.4 Mt.

- Click here to discover the nuances of Stanmore Resources with our detailed analytical financial health report.

- Assess Stanmore Resources' future earnings estimates with our detailed growth reports.

Summing It All Up

- Gain an insight into the universe of 400 ASX Penny Stocks by clicking here.

- Interested In Other Possibilities? Uncover 11 companies that survived and thrived after COVID and have the right ingredients to survive Trump's tariffs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:SMR

Stanmore Resources

Engages in the exploration, development, production, and sale of metallurgical coal in Australia.

Very undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

13 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on American Resources ·

American Resources, $263M Market Cap + 19% ReElement Stake, From Coal to Critical Minerals

Fair Value:US$557.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on EPB Group Berhad ·

EPB: Strong Shareholder Backing, Continuous Insider Buying and Growth Opportunities Ahead

Fair Value:RM 0.548.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YO

youwakeup on Harvest Strategy Enhanced High Income Shares ETF ·

MSTE: Turning Bitcoin Volatility Into Monthly Cash Flow

Fair Value:CA$11.7579.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

58 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative