Imagine a world where you could borrow money at an interest rate between 0% to 1%, and invest that in a treasury note (i.e. “risk-free”) returning 3% to 4%. Would you do it?

The answer… probably yes.

And believe it or not, that’s how the world functioned for many years.

Japan’s interest rate was far below that of the US, Canada, the UK, and many other countries for decades, and governments, institutions, and individuals all over the world made the most of it.

But what happens if Japan finally raises rates?

What happened in the markets this week?

📈 AI rally pushes US markets to fresh highs, Micron enters $1T territory ( Reuters )

- What happened: The S&P 500 and Nasdaq closed at record highs as enthusiasm around AI lifted semiconductor stocks. Micron surged 19% after UBS sharply raised its price target, pushing the company above a US$1 trillion market value for the first time.

- How it impacts investors: AI-linked momentum is continuing to drive broader market gains, especially across semiconductors and infrastructure plays. Valuation and multiples may start to become stretched so investors may need to be more vigilant.

- Next steps: Dive into our High Growth Tech & AI investing ideas to explore companies benefiting from the AI buildout. Check Micron’s company report to see whether it’s worth its new 13-figure valuation.

🏭 China’s factory profits rebound despite trade and deflation pressures ( Reuters )

- What happened: China’s industrial profits rose 24.7% in April from a year earlier, marking the fastest monthly growth in more than two years. The rebound was driven by stronger manufacturing activity and government support measures, even as exporters continued to face tariff pressures and weak domestic demand.

- How it impacts investors: The jump in profits could improve sentiment toward Chinese equities and industrial sectors, but ongoing deflation risks and trade uncertainty still point to a fragile recovery.

- Next steps: Learn more about the government support backing China’s growth in a previous edition of Market Insights .

💰 Hong Kong is now the world’s largest wealth hub ( Reuters )

- What happened: Hong Kong overtook Switzerland as the world’s top cross-border wealth management hub. The shift was driven by rising Chinese wealth flows and a strong IPO market, helping Hong Kong reach US$2.95 trillion in offshore assets.

- How it impacts investors: This reinforces Asia’s growing influence in global capital flows and wealth management. Investors may increasingly look toward Asian financial centres exposed to regional wealth growth.

- Next steps: Explore our prebuilt investing ideas for Hong Kong .

🧠 SK Hynix also joins the trillion-dollar club ( Reuters )

- What happened: Korea’s SK Hynix surpassed US$1 trillion in market cap for the first time, joining Samsung Electronics and Micron as AI-driven chip demand continues to push memory prices higher.

- How it impacts investors: The story highlights how AI infrastructure spending is reshaping the semiconductor industry, with memory chipmakers emerging as some of the biggest beneficiaries. It also raises expectations for continued earnings strength across the broader AI supply chain.

- Next steps: Compare global semiconductor leaders using our Semiconductor screener. Also check out SK Hynix’s company report to see if the valuation is justified.

Why Japan’s bond yields matter

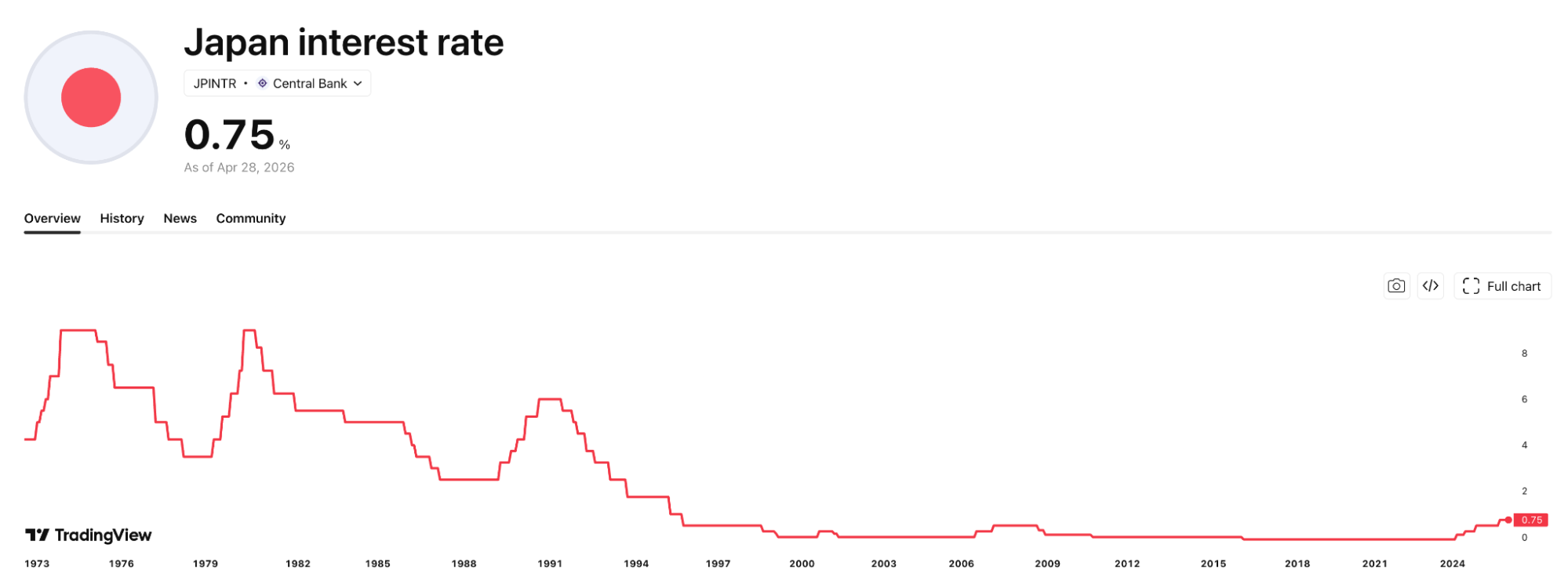

Since the burst of Japan’s asset bubble in the 90’s, the Bank of Japan (BOJ) kept the country’s interest rate at a range between -0.1% to 0.5%.

For 30 years, the country maintained its quantitative easing stance to support a slowing economy and a population scarred by the crisis.

That created a very unusual setup. While many countries offered higher yields, Japan remained one of the cheapest places in the world to borrow money. So investors did what investors tend to do when they see an opportunity.

They borrowed yen, converted that money into another currency, and invested it somewhere with a higher return, doing what’s known as the ‘carry trade’.

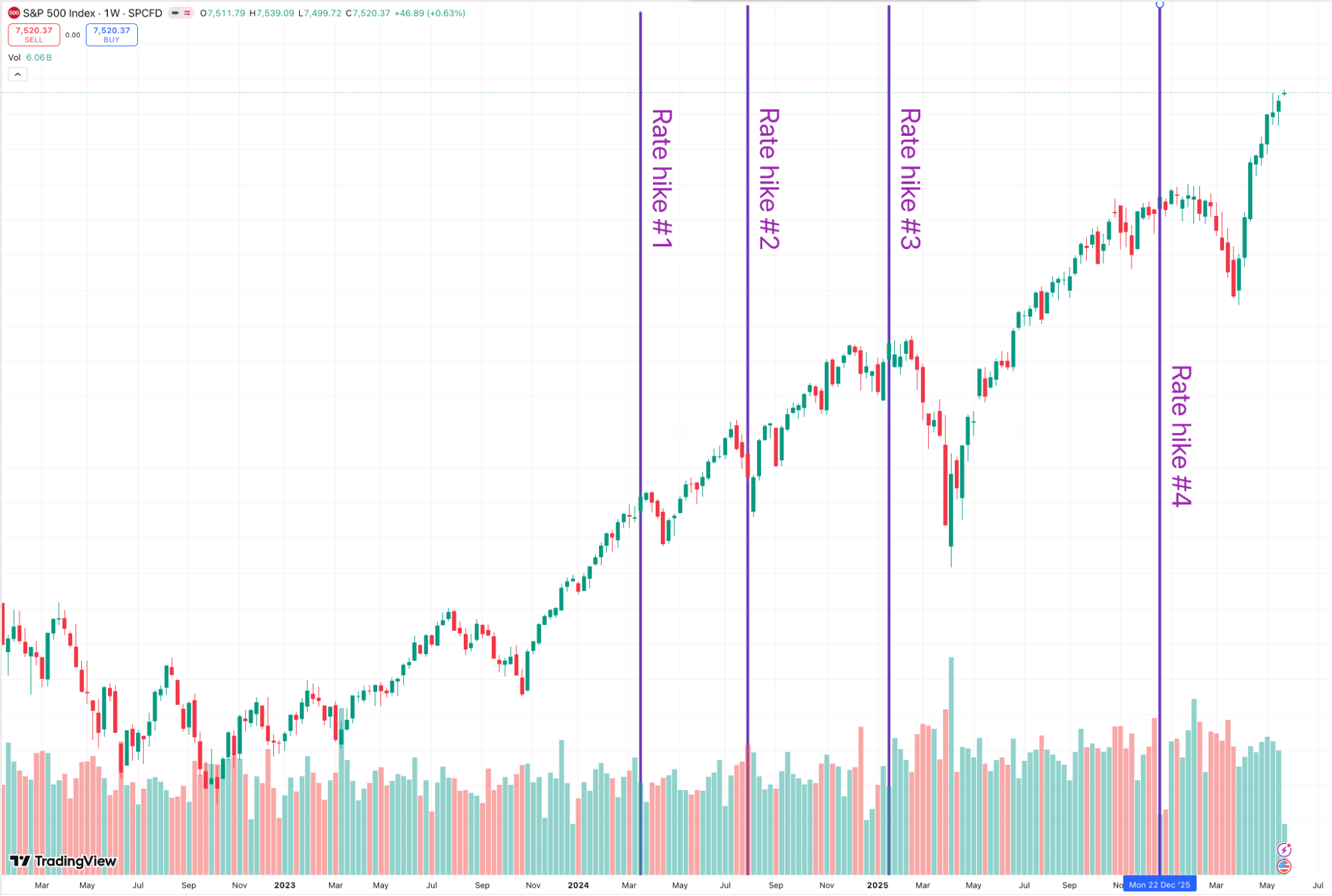

But change began in 2024. The BOJ hiked rates for the first time in years, ending the era with a negative interest rate. In less than two years, Japan’s interest rate increased from -0.1% to 0.75% (across four rate hikes).

On top of that, today’s story was triggered by a key event. Last month, Japan’s 10-year bond yield hit 2% for the first time since 1999. The 30-year bond yield went over 4% for the first time since it was created, also in 1999.

Bond yields are generally considered a proxy measure for the market’s expectations of where a country’s rates will go in those time periods.

Coupled with Japan’s falling Yen, expectations of higher inflation , and rising fuel prices , many signals are implying that the 0.85% rate hike was just the beginning of the BOJ’s long-term move.

Why the end of “cheap Japanese money” matters

While the carry trade was a major investment strategy for many, it was only one of the effects of Japan’s three decades of Japan’s ultra-low interest rates. Here are other areas that will be impacted by rising interest rates.

- Companies that relied on Japan for funding

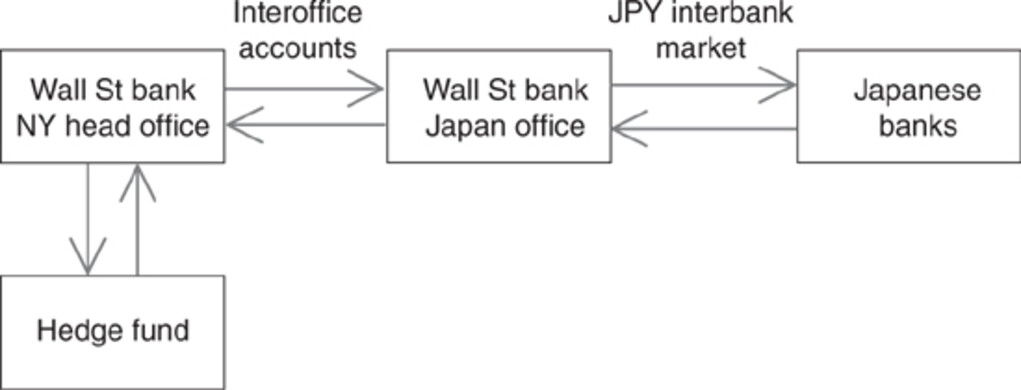

The IMF’s research back in 2009 (when the GFC happened) illustrated how foreign firms took advantage of Japan’s lower rates to fund the US mortgage credit market by using a Japanese subsidiary to borrow from Japanese banks, then sending those funds over to the US.

The IMF’s findings proved just how much Japanese creditors funded the US:

" Although the yen carry trade has traditionally been viewed in narrow terms purely as a foreign exchange transaction, we have argued that they hold broader implications for the workings of the financial system and for monetary policy. ”

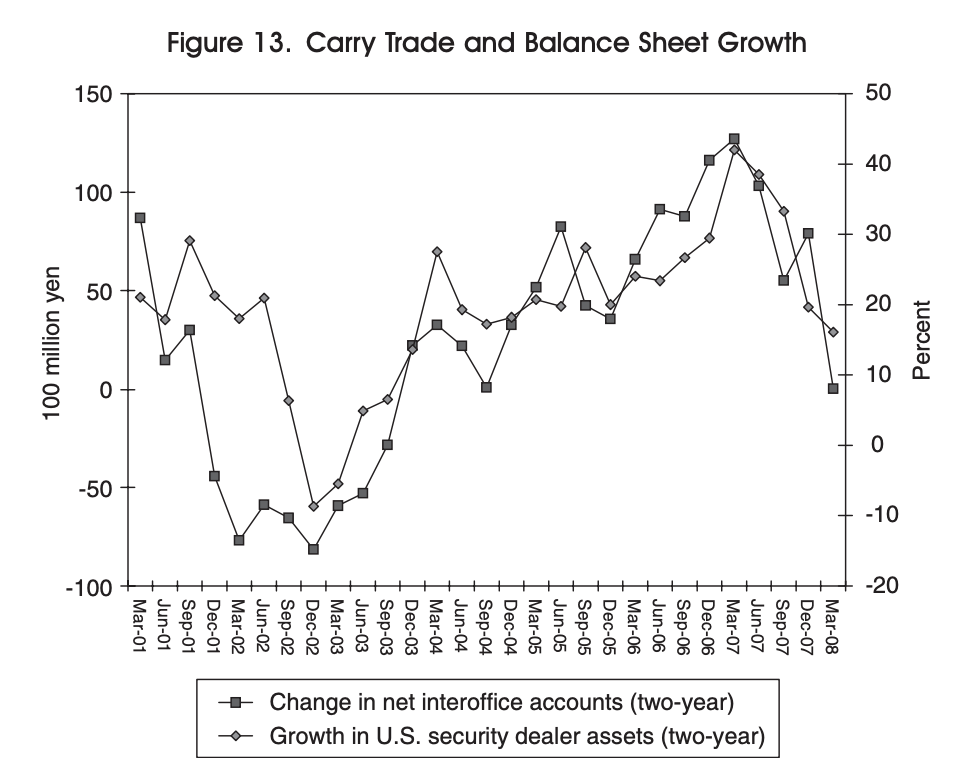

And indeed, the chart below shows the correlation between the carry trade (net interoffice accounts, which shows the net flow of funds into the US) and US balance sheets.

While it’s difficult to find more recent data, it’s more than likely that the IMF’s findings continued to hold true while Japan’s rates remained low.

A proxy indicator is Japan’s net investment position (i.e. the value of Japan’s overseas assets minus foreign claims on Japan), which has grown over time and currently sits at $3.85 trillion .

The chart shows just how much Japanese firms and individuals have invested outside of Japan.

With Japan’s interest rate rising, the gain derived from using Japanese borrowing will shrink, potentially hurting the balance sheets of foreign companies and tightening funding for capital investments.

Similarly, earnings may suffer as interest expenses start to bite into the bottom line.

- Investments from Japan will shrink

Japan held roughly $1.2 trillion in US treasuries earlier this year, making it the US government’s largest foreign creditor by a wide margin.

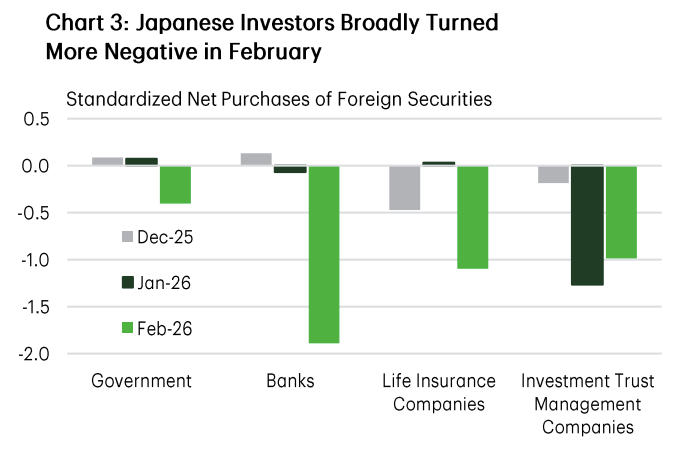

But that’s set to change. Japanese institutions have begun offloading foreign securities as Japan’s rising bond yield has made domestic investments more appealing.

Previously holding nearly 9% of all US treasury a decade ago, Japan’s share has now shrunk to just around 4%.

The situation is starting to flip. Japanese companies are starting to get funding from overseas now, raising $132 billion in foreign currency bonds and loans last year.

All these changes have combined to make Japan go from being the world’s largest net creditor to now falling below China and Germany . Prior to this, it held the top spot for 34 years.

For stock investors, the key risk is indirect: less Japanese demand for foreign assets can push global yields higher, which pressures valuations.

- Carry trades are slowly unwinding

While the yen carry trade may look like a simple investment strategy at the individual or institutional level, its scale has become large enough that any major shift in the trade can ripple through global markets and economies.

This is because the carry trade is not driven by interest rate differentials alone, currency movements also matter.

For example, imagine borrowing ¥140 million to invest in a $1 million bond (exchange rate of $1 = ¥140). If you later choose to repay that loan, but the JPY is now at an exchange rate of $1 = ¥80, the initial $1 million you received will now only convert to ¥80 million, requiring you an additional $750,000 to repay the full loan. Even a 5% return on the bond wouldn’t suffice for the currency loss.

You can see from this situation that those who leveraged the JPY for a carry trade will lose out if the JPY appreciates in value (i.e. the external currency can buy less yen).

Now going back to the current situation. Economic theory shows that rate hikes also generally lead to currency appreciation . That means for those that have carry trades, rate hikes are a warning signal.

And true enough, the correlation of the BOJ’s rate hikes and the S&P 500 speaks volumes about the scale of the Yen carry trade…

Statistics have shown that a portion of carry trades have been unwinded (i.e. positions sold and debt repaid) since the rate hikes began.

But statistics also point to a high possibility that a significant portion of global markets are still funded by borrowed yen as the interest rate difference between the US and Japan remains substantial. Additionally, the yen remains weak despite the BOJ’s moves.

Analysts believe that there will be two major catalysts to further unwinding of the Yen carry trade:

- Drop in the value of the invested assets

- Rebound in the JPY

When that happens, it’s highly likely we’ll be seeing a major impact on global markets.

The Insight: So how do we invest from here?

To summarize this article: Japan’s interest rates are no longer anchored near zero. Cheap yen funding is becoming less cheap, Japanese investors have more reason to keep capital at home, and markets that benefited from 30 years of easy Japanese money will likely have to adjust.

For investors, it means being vigilant and keeping an eye on these key areas:

The most exposed companies are those that relied on low global interest rates for growth and sustainability. That includes companies with high debt, regular refinancing needs, weak free cash flow, or valuations based heavily on profits far into the future.

US credit is another area to watch. Japanese institutions have long been major buyers of US bonds, including corporate debt. If that demand fades, companies may need to pay more to borrow, and weaker borrowers may face wider credit spreads.

It’s also worth watching the movement of the JPY . Outside of the carry trade’s unwinding, a weaker yen can also hurt foreign companies that earn revenue in Japan, because those sales translate back into fewer dollars or euros. On the flip side, a stronger yen can pressure Japanese exporters, because overseas earnings become worth less when converted back into yen.

The better positioned companies in this environment are likely to be the opposite: Low debt, strong free cash flow, less reliance on external funding, and earnings driven mainly by domestic demand.

In short, the end of cheap Japanese money is not just a Japan story, but a global liquidity story.

Key events next week

Tuesday

- 🇪🇺 Inflation Rate YoY Flash

- Forecast: 3.4%, Previous: 3.0%

- Why it matters: A rebound in eurozone inflation could reduce the chances of near-term ECB rate cuts and keep pressure on borrowing costs across the region.

Wednesday

-

🇦🇺 GDP Growth Rate QoQ

-

Forecast: 0.5% , Previous: 0.8%

-

Why it matters: Slower economic growth could strengthen expectations for further RBA easing, particularly if consumer spending and business activity continue softening.

-

Thursday

- 🇦🇺 Balance of Trade

- Forecast: A$-3.0B, Previous: A$-1.841B

- Why it matters: Australia’s trade balance can provide insight into export demand and commodity market strength, particularly for iron ore and energy exports.

Friday

- 🇺🇸 Unemployment Rate

- Forecast: 4.4% , Previous: 4.3%

- Why it matters: A rising unemployment rate may signal a cooling labour market, which could ease inflation pressures and influence the Fed’s next move.

- 🇨🇦 Unemployment Rate

- Forecast: 6.9%, Previous: 6.9%

- Why it matters: Labour market data could influence expectations around future Bank of Canada policy decisions and the outlook for the Canadian economy.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Mitch Lawler and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Mitchell Lawler

Mitchell Lawler is a Senior Investment Editor at Simply Wall St, where he oversees Market Insights and the platform’s published editorial content. He also leads The Foxhole, a daily forum for contrarian investment ideas and constructive debate, drawing on nearly a decade of personal investing experience and more than five years in professional equity research and financial publishing.