The most anticipated IPO in history will hit the market next week. When Elon Musk is involved, opinions tend to be firmly on one side or the other. In the case of the IPO S-1 filing , mention of colonizing Mars and mining asteroids only adds to the division.

Today we are avoiding the spectacle and having a look at what the business is really about: the opportunities, the challenges and what the listing could mean for investors.

What Happened In Markets This Week

Here’s a quick summary of what’s been going on:

🤖 India loses edge as investors flock to Asia’s AI hubs ( CNBC )

-

What happened: India has found itself on the wrong side of more than one trend lately. Energy and fertilizer costs are soaring due to the war in the Strait of Hormuz. Higher costs are hitting consumption, which is a key part of the growth narrative. At the same time investors are rushing to the Asian markets with AI exposure, an area where India lags. In particular, Taiwan and Korea’s markets are now highly concentrated AI bets.

-

How it impacts investors: The way capital is chasing growth and momentum should also be seen as a warning: things can turn very quickly. India is now becoming a contrarian bet in Asia. It may turn out to be an effective diversifier at some point.

-

Next steps: Use the Simply Wall St stock screener to hunt for potential opportunities in India;s equity market.

💸 Alphabet's $80 billion share sale puts capital markets in "unprecedented territory" ( CNBC )

-

What happened: Google's parent company has launched the largest equity offering in corporate history to fund its AI buildout. This is the first time one of the Mag 7’s AI capex ambitions have outgrown its ability to self-fund. Alphabet has raised projected capex for 2026 to between $180 billion and $190 billion, and said further increases in 2027 are likely too.

-

How it impacts investors: Google may also be anticipating a squeeze on capital, with three trillion dollar IPOs on the way, and competitors increasing capex at the same time.

-

Next steps: This is positive for the entire AI infrastructure supply chain. Check out the AI picks and shovels collection and this Powering the AI Revolution: Next-Gen Energy & Grid watchlist for some ideas.

⚡ SoftBank's €75bn french bet exposes Europe's AI power problem ( CNBC )

-

What happened: SoftBank plans to build 3.1 GW of AI data centers in northern France by 2031, including sites in Dunkirk, Bosquel, and Bouchain — its largest AI infrastructure investment in Europe. With over 60% of its power needs met by nuclear energy, France is uniquely placed to handle energy-intensive data center projects at a time when European industrial electricity prices are roughly double those in the US.

-

How it impacts investors: This is a reminder also a blunt reminder that Europe's energy costs remain a liability in the global AI arms race. SoftBank will partner with Schneider Electric on a large-scale industrial production cluster giving France a foothold in the AI supply chain.

-

Next steps: Europe’s tight energy markets make capacity expansion an imperative. You can explore the energy and utilities sectors in Europe with the Simply Wall St stock screener . You can also check the Schneider Electric company report to find peers and competitors.

The SpaceX IPO countdown begins

Let’s start by laying out the key numbers:

The Initial public offering

- Date: 12 June 2026

- Ticker: SPCX

- New shares for sale: 555.6 million, or ~ 4% of the 12.9 billion shares currently outstanding.

- Underwriting syndicate: 21 banks and brokers with option to acquire an additional 83 million shares.

- IPO share price: $135 (fixed price as per roadshow to institutions)

- Capital being raised: $75 billion

- Target market cap: $1.75 trillion market cap (at $135 share price)

The financials (2025):

| Revenue ($ Billions) | Operating profit/loss ($ Billions) | |

| Space (launch) | $4.1 | -$0.6 |

| Connectivity (Starlink) | $11.4 | $4.4 |

| AI (xAI and X) | $3.2 | -$6.4 |

| Total | $18.7 | -$2.6 |

Context for the $1.75 trillion valuation target:

- 95 times 2025 revenue and ~60 times 2026 revenue estimates

- $2.0 trillion to 2.4 trillion: Prediction market estimates for post IPO market cap

- $1.22 trillion: DCF estimate published by Aswath Damodaran (based on Launch and Starlink alone)

- $1.2 trillion: The valuation implied by the merger with xAI

- $800 billion: Implied value at last funding round

- $780 billion: Morningstar’s recent estimate

The Business Segments

SpaceX is known as a space business, but it’s evolving into more of an AI business now. The filing doc identifies a TAM (total addressable market) of $28.5 trillion. Regardless of how realistic that is, less than $2 trillion is related to space and connectivity.

The big vision might be about making ‘life multiplanetary’ and colonizing Mars, the biggest immediate opportunity (and capex) is very much focused on AI. Nevertheless the space and connectivity segments are also crucial cogs.

The Space segment: Launch

The Opportunity

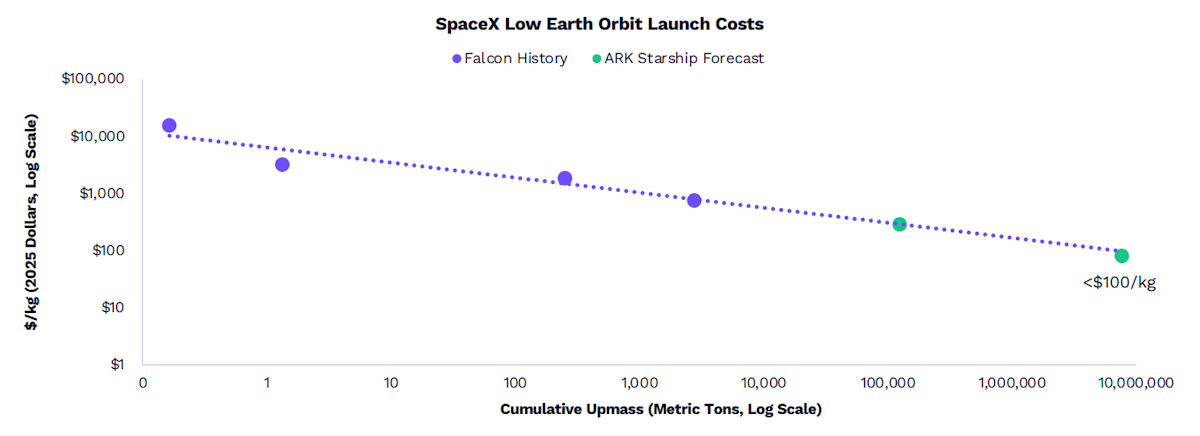

SpaceX effectively dominates the global launch market. The company’s success with reusable boosters, and its ability to scale, have completely changed the economics of getting objects into orbit.

Significantly lower launch costs make more use cases viable for SpaceX and for its customers. And owning the dominant launch business also gives SpaceX a cost advantage for any of its businesses that use the platform.

Challenges and Risks

The launch business is a low margin, and capital intensive business, though it exists to provide a platform for SpaceX’s other ambitions.

The future of SpaceX depends largely on making the massive Starship vehicle fully and rapidly reusable. In particular, the heat shield material needs to repeatedly withstand thermal stress. This is a crucial engineering challenge that hasn’t been solved yet. In fact, the S-1 even warns that the rocket program (amongst other programs) "may never achieve commercial viability"

In addition, the launch business has struggled to get to a reliable launch cadence for its V2 Starlink satellites.

The Connectivity Segment: Starlink

The Opportunity

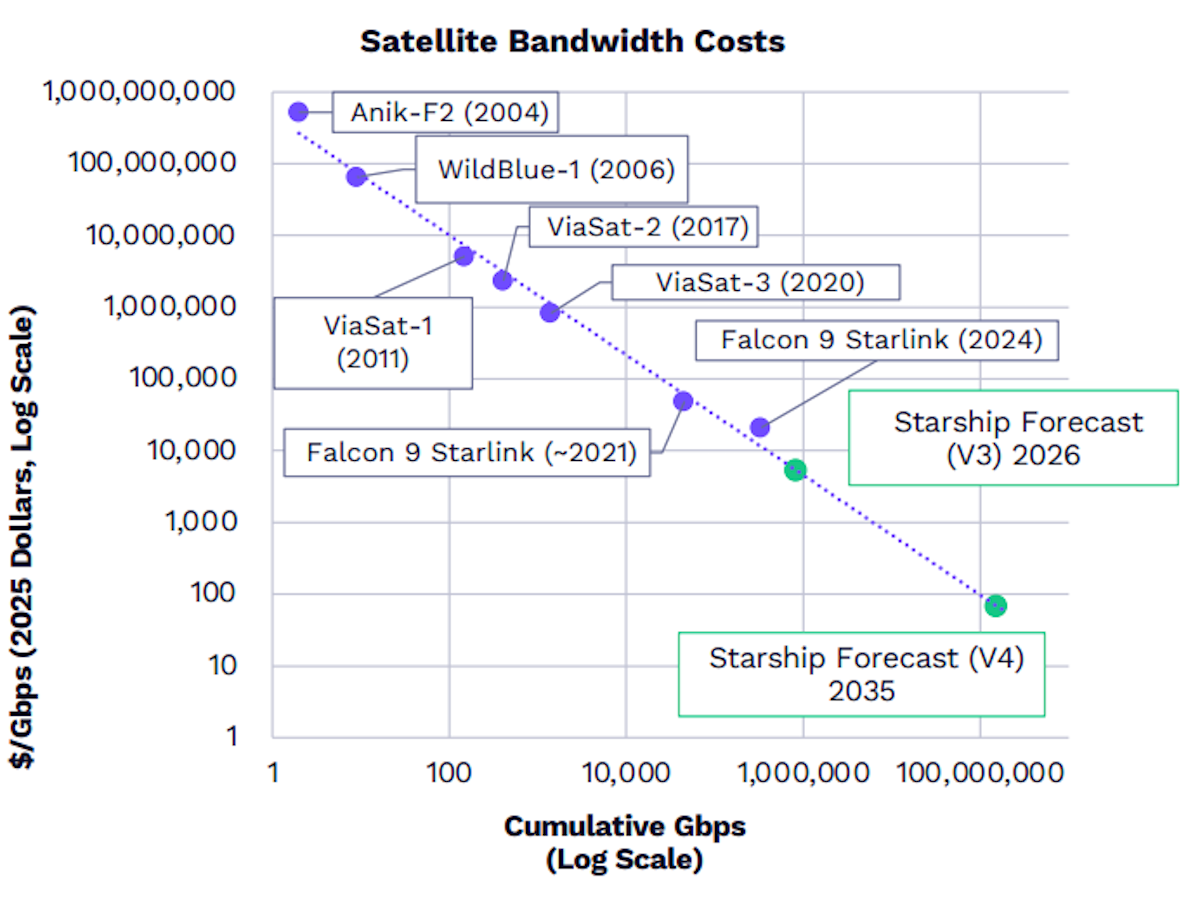

Starlink, which provides fixed broadband and direct-to-cell connectivity via satellite, is the most profitable segment. Falling launch costs have resulted in falling bandwidth costs, allowing Starlink to target a larger market.

Starlink currently has 10 million subscribers, a fraction of its potential market . In particular, parts of the world that are underserved by mobile and terrestrial networks are key opportunities. Africa’s mobile penetration rate is below 50%, with mobile internet penetration at 28% (i.e. ~400 million people).

Direct-to-cell connections (which don’t require special hardware) mean mobile carriers around the world could ultimately be disrupted. SpaceX has also acquired spectrum licenses from EchoStar, expanding its footprint substantially.

Competition in this space is increasing, but Starlink has a major scale and cost advantage.

Challenges and Risks

Starlink has several challenges, on the technical, financial and regulatory front:

- The satellites are ‘consumable’ by design, and only last for 5 years. This means they can be upgraded, but it also means 20% of the fleet must be replaced each year, at a cost of $2.7 billion. This is where Starlink's 2025 EBITDA ( aka operating earnings ) of $7.1 billion is a little misleading, as it strips out depreciation, which is a real and ongoing cost for Starlink.

- Low Earth Orbit (LEO) satellites are susceptible to urban congestion when too many users share the same satellite ‘beam’.

- Mobile bandwidth licences are typically awarded to networks by regulators. Technically, this doesn’t affect Starlink but governments can criminalize the hardware or use of satellite connections. Several countries in Africa and Asia are already blocking the network for a range of reasons.

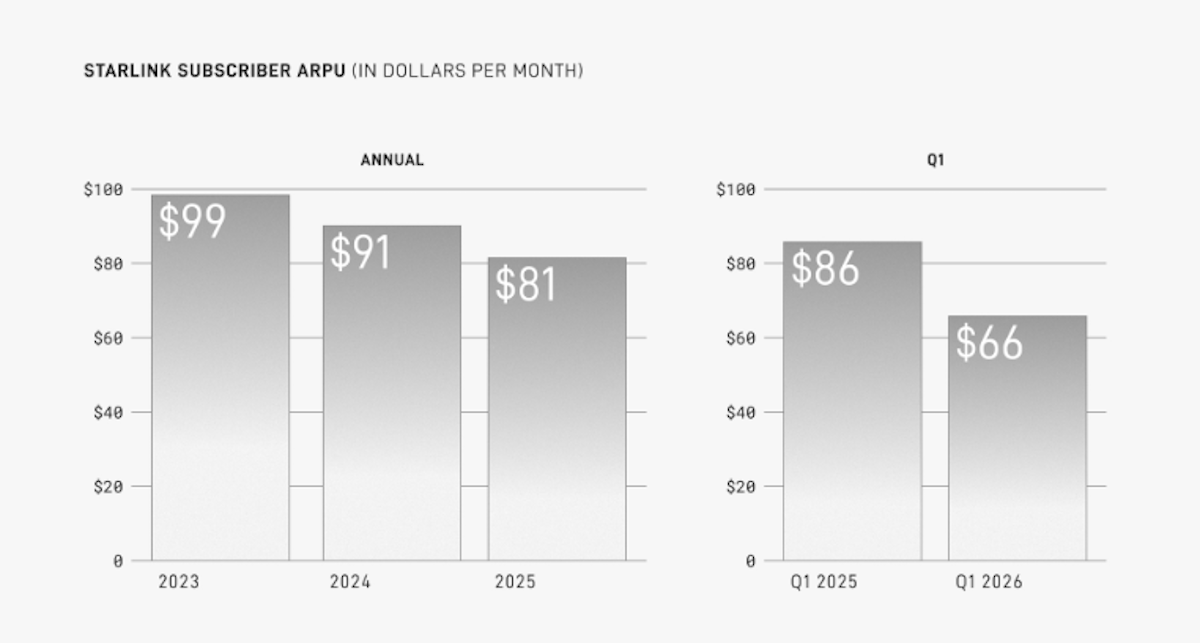

- Starlink’s monthly average revenue per user has already fallen from $99 in 2023 to $66 in Q1 2026. It’s likely to keep falling, as the company targets developing economies, and as competition increases.

The AI Segment: xAI, Grok, X, COLOSSUS

The Opportunity

Whether by accident or design, AI has become the core opportunity for SpaceX. Demand for AI compute power is surging, as shown by xAI’s recent deal with Anthropic.

Anthropic will be paying $1.25 billion per month for compute power from the Colossus 1 data center. This implies that xAI doesn’t anticipate enough demand for its own Grok LLM, but it's not a bad plan B, and almost doubles the company’s revenue.

If demand for AI compute does continue to grow, then SpaceX is building the full AI stack:

- The Grok series of LLMs , trained with the help of massive quantities of data from X.com .

- Logic and memory chips, eventually designed and manufactured at Terafab , a joint venture with Tesla , xAI and Intel .

- Training and inference at the COLOSSUS datacenters . xAI is also providing compute to Cursor, collaborating on models, and potentially acquiring the company for $60 billion .

- Orbital, solar-powered, data centers in space. Unproven and unprecedented, these together with the SpaceX launch platform would complete the vertically integrated AI stack, with cost advantages at every level.

The chart below shows TSMC’s net margin, which is currently 46%, and it’s been above 30% for the past 10 years. This is a key part of the SpaceX strategy. Every bit of margin that SpaceX can avoid paying is an opportunity to gain a cost advantage.

Challenges and Risks

This incredibly ambitious plan obviously comes with incredibly big challenges. These are the most notable ones:

- The AI business is already burning cash: $6 billion in 2025 and $2.5 billion in Q1 2026. Every part of the AI business is incredibly capital intensive. The Terafab is set to cost $55 billion initially, $119 billion for the full build out, and eventually trillions, apparently!

- Even if AI demand continues to grow, it might be quite cyclical, which will make raising capital tricky, and possibly expensive.

- Manufacturing semiconductor chips is one of the most complex processes in the world, and few companies have managed to do it.

- Orbital data centers are an unproven idea. Conducting heat away from the server stacks in a vacuum is seen as the biggest challenge.

- The Grok models are currently lagging rivals, both in terms of performance benchmarks and usage . To fully capitalize on the opportunity, xAI needs to use its own hardware and models.

Beyond SpaceX: The potential impact of the IPO

This IPO is unprecedented in size, and is likely to have implications for the broader market. Based on closing prices on 3rd June, and a $1.75 billion market cap, SpaceX would rank as #9 in the global market cap table. Coincidentally this is just ahead of Tesla.

The Trillion Dollar Club

| No. | Company | Market cap (US$ Billions) | S&P 500 weight | Nasdaq 100 weight | Price to sales (P/S) ratio | Net income margin |

| 1 | Nvidia | $5,220 | 8.4% | 8.6% | 21 | 63% |

| 2 | Apple | $4,540 | 6.9% | 7.1% | 10 | 27% |

| 3 | Alphabet | $4,330 | 6.0% | 6.7% | 10 | 38% |

| 4 | Microsoft | $3,160 | 5.3% | 5.4% | 10 | 39% |

| 5 | Amazon | $2,670 | 3.9% | 5.1% | 3.6 | 12% |

| 6 | Broadcom | $2,290 | 3.3% | 3.5% | 34 | 37% |

| 7 | TSMC | $2,200 | n/a | n/a | 17 | 47% |

| 8 | Saudi Aramco | $1,760 | n/a | n/a | 4 | 22% |

| 9 | SpaceX | ~$1,750 | TBC | TBC | ~95 | -26% |

| 10 | Tesla | $1,590 | 1.8% | 3.3% | 16 | 4% |

Bending the Index Rules

Based on market cap alone, SpaceX belongs in major indexes like S&P 500 and Nasdaq 100. But index providers usually have other rules, covering free float size, months listed and profitability.

This time, some index providers seem to be going out of their way to accommodate SpaceX:

- Nasdaq-100: The brand new ‘Fast Entry rule’ means the stock will be in the index after 15 trading days. For context, it took Facebook seven months, and Tesla 3 years. Approximately $400 billion tracks this index, but because of the restrictive amount of free float of around 4.3% of company shares, the 3x float cap will reduce the effective weighted market cap of ~$225 billion. This would imply flows of ~$3 billion to $4 billion into SpaceX.

- S&P has ruled out fast-tracked index inclusion. SpaceX would need to be publicly listed for a minimum of 12 months and be profitable for inclusion.

- Other indexes will be affected too, but these are the ones with large AUM (assets under management) tracking them.

If the S&P inclusion goes ahead a year later, hedge funds will be attempting to pre-empt the rotation, which could be easier said than done.

If SpaceX does go into the S&P 500 index, anyone invested in any product tracking that index will end up with SpaceX, whether they like it or not, and whether they like the price, at the time of inclusion, or not. It’s worth noting the anticipated price-to-sales ratio of 94 times sales. The highest comparable ratios are Broadcom (34 times sales) and Palantir (65 times sales) both of which are growing and very profitable.

Some are anticipating a move to equal weighted index funds. If this works out badly for ETF investors that could be the case.

Market Liquidity

The implications for index funds will take a while to unfold. In the meantime,

$75 billion is a massive amount of liquidity to be absorbed by the market. The combination of unknown demand, unknown supply from existing shareholders, and a potential liquidity squeeze in other markets, means extreme volatility could be on the cards.

The Tesla Scenarios

There’s a lot of speculation around Tesla, and a potential merger of Musk’s two companies. An amended IPO filing doc included the following text: “may issue a significant amount of equity in connection with future transactions” which only added to the speculation.

There are good reasons for a merger, but it may be worth keeping an open mind. Some analysts have pointed out that it might be more difficult to raise further capital after a merger, and terms for a deal would be difficult to negotiate.

Whether it happens or not this could become a major part of the narrative around Tesla share price. Check the Tesla Community Page to see what others are saying about the outlook.

The Space and AI Ecosystems

Some of the capital being raised will stay within SpaceX. But a lot will ultimately flow to suppliers and partners. Based on the capex plans, the AI ecosystem is in line for the bigger share. That means companies supplying GPUs, CPUs, networking, and energy infrastructure equipment.

But the developments are also positive for the broader aerospace and defense industry , which is also smaller, and getting a lot of attention now. The Beyond the Moon watchlist includes the key space related companies, large and small.

💡 The Insight: Investing in optionality

It really isn’t surprising to see the market so divided on the valuation and outlook for SpaceX.

The bull thesis combines innovation, vertical integration, economies of scale and a (currently) very real demand story. If everything goes right, the competitive advantages stack up quickly. But that thesis also includes unproven ideas and problems that still need to be solved.

If you base your thesis only on proven technologies, revenue and margins, the price tag won’t make sense.

The reality for capital intensive businesses is that things take longer and cost more than expected. All the hurdles that need to be overcome or solved, are milestones that need to be ticked off.

- As each gets ticked off, the long term goal becomes more probable. This means the company earns a higher valuation.

- When a milestone is missed, the valuation needs to be reset for a longer time horizon.

If you pay for all the success upfront, there’s no margin for error, and possibly no upside either.

Key Events Next Week

Tuesday

- 🇨🇳 China Trade Balance

- ➡️ Forecast: $89 billion Previous : $84.8 billion

- ➡️ Why it matters: Weak imports would signal softening domestic demand, which may weigh commodity prices.

Wednesday

- 🇺🇸 US Inflation Rate

- ➡️ Forecast: 3.9%, Previous : 3.8%

- ➡️ Why it matters: A print any higher than expected makes rate cuts this year unlikely.

- 🇨🇦 Bank of Canada Interest Rate Decision

- ⏸️ Forecast: 2.25% Previous : 2.25%

- ➡️ Why it matters : Expected hold; a surprise hike on oil-driven inflation would catch markets off-guard.

Thursday

- 🇪🇺 ECB Interest Rate Decision

- 📈 Forecast: Deposit Rate 2.25%, Previous : 2.00%

- ➡️ Why it matters: Hike is fully priced in, but the market will be following commentary closely.

Friday

- 🇬🇧 UK GDP MoM

- 📉 Forecast: 0.1% Previous : 0.3%

- ➡️ Why it matters: Expected cooling after the fuel-price shock.

Quite a few smaller companies are still due to report Q1 earnings, but amongst the large caps it’s just Oracle and Adobe this week.

Editor's note: A previous version of this article implied the potential for ~$20 billion in Nasdaq-100 index flows. This was calculated on the total market capitalization rather than the effective "weighted" market cap that applies when public free float is less than 20% (which is expected to be the case for SpaceX). This has been amended to reflect the potential flows of $3 billion to $4 billion once the 3x float cap rule is applied.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.