Last Update 11 Dec 25

Fair value Decreased 6.04%OKTA: Future Identity Data Compliance And AI Security Will Drive Performance

Analysts have modestly reduced their price target on Okta, trimming fair value estimates by about $7 to reflect slightly slower projected revenue growth and a lower future earnings multiple, even as profit margin expectations edge higher.

Analyst Commentary

Bullish Takeaways

- Bullish analysts note that management's guidance still implies solid mid-teens top-line expansion over the medium term, which supports a premium to slower-growing security peers despite the lower price target.

- Expectations for remaining performance obligation growth of around 10 percent year over year, with a credible upside scenario toward 13 percent, reinforce the view that demand for Okta's platform remains resilient.

- Improving margin trends and a clearer path to sustainable profitability are cited as key offsets to the modestly slower revenue outlook, which helps underpin current valuation levels.

- Analysts see continued adoption of identity security and consolidation of point solutions as structural tailwinds that can sustain Okta's growth and justify a higher multiple if execution remains consistent.

Bearish Takeaways

- Bearish analysts highlight that trimming the price target signals diminished confidence in Okta's ability to reaccelerate growth, which could cap near term multiple expansion.

- The base case for remaining performance obligation growth near 10 percent is viewed as a step down from prior years, raising concerns that competitive intensity and macro headwinds may be weighing on new business.

- Some are cautious that any upside scenario for growth, such as reaching 13 percent remaining performance obligation expansion, may require stronger than expected execution around large enterprise deals and cross selling.

- There is concern that investors may already be pricing in a meaningful improvement in profitability, leaving limited room for error if margins or billings volatility disappoint against expectations.

What's in the News

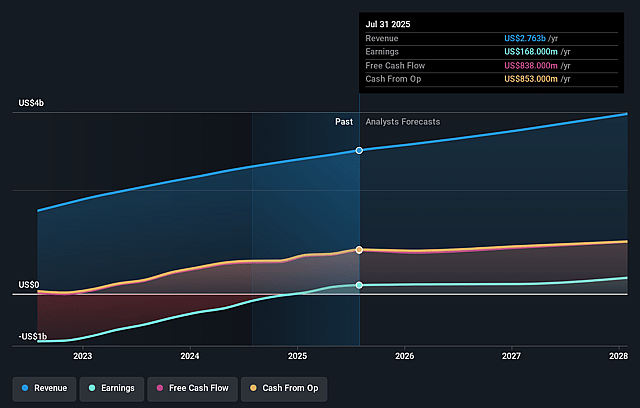

- Issued updated guidance for fiscal 2026, projecting total revenue of $2.906 billion to $2.908 billion, up 11 percent year over year, and fourth quarter revenue growth of about 10 percent with current RPO growth of 9 percent (Corporate guidance).

- Announced a new full service Okta cell in Canada to keep customer identity data in country, support data residency, provide enhanced disaster recovery with a five minute recovery target, and expand French language product support for Quebec and Francophone users (Business expansion).

- Introduced new Okta and Auth0 platform capabilities to secure AI agents and enable tamper proof verifiable digital credentials, aiming to provide centralized, standards based identity security for both human and non human identities (Product related announcement).

- Enabled Fullpath to launch a Single Sign On integration with Okta, giving auto dealerships streamlined and secure access to customer data and tighter permission management via existing enterprise identity providers (Client announcement).

- Expanded integration with MIND to link Okta identity signals with AI driven data security controls, helping enterprises automatically enforce context aware policies and mitigate insider risk at scale (Client announcement).

Valuation Changes

- Fair Value: Reduced modestly from about $118.80 to $111.62 per share, reflecting a slightly more conservative outlook.

- Discount Rate: Edged down marginally from roughly 9.12 percent to 9.04 percent, implying a slightly lower required return.

- Revenue Growth: Trimmed from approximately 9.62 percent to 8.98 percent, indicating a small downgrade to long term growth expectations.

- Net Profit Margin: Increased slightly from about 11.45 percent to 11.53 percent, reflecting incremental improvement in projected profitability.

- Future P/E: Lowered from roughly 70.7x to 66.9x, suggesting a modestly lower valuation multiple on expected earnings.

Key Takeaways

- Okta benefits from growing demand for unified cloud identity platforms and rising security needs amid complex digital transformations, driving durable revenue and larger contracts.

- Expansion into AI-driven security and broadening platform offerings increases cross-sell opportunities, supporting margin improvement and long-term profitability.

- Intensifying competition, integration risks, limited new customer growth, selective international focus, and evolving technologies threaten Okta's revenue growth, pricing power, and long-term margins.

Catalysts

About Okta- Operates as an identity partner in the United States and internationally.

- Okta is positioned to capture expanding demand as enterprises globally accelerate cloud migration and digital transformation, with increasing complexity and fragmentation in identity systems driving large organizations to consolidate onto a unified, cloud-native platform-supporting multi-year revenue growth and larger average contract values (ACV).

- The proliferation of AI agents and nonhuman identities is creating new, urgent security use cases that require sophisticated identity governance, privileged access management, and policy controls-areas where Okta is innovating (Cross App Access, Auth0 for AI Agents, Axiom acquisition), opening incremental growth avenues and potential margin expansion through higher value and differentiated products.

- The rising frequency and sophistication of cyberattacks, combined with tightening regulatory mandates (especially in the public sector and large enterprises), are establishing identity as a mission-critical, recurring investment category; this aligns with Okta's increased penetration in federal and enterprise verticals, which enhances revenue durability and long-term earnings visibility.

- Okta's expanding platform breadth beyond workforce IAM-including customer identity, security posture management, threat protection, and suites-improves cross-sell and upsell opportunities, supporting top-line acceleration and leveraging existing sales channels for improved operating leverage and net margin improvement as specialization in go-to-market teams boosts sales productivity.

- Global adoption of Zero Trust security frameworks and the movement toward SaaS-native security stacks favor independent, extensible platforms with broad integration ecosystems, allowing Okta's neutral, open approach to capture wallet share as customers seek to avoid vendor lock-in from larger, bundled security suites-sustaining long-term revenue growth and profitability.

Okta Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Okta's revenue will grow by 9.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.1% today to 11.4% in 3 years time.

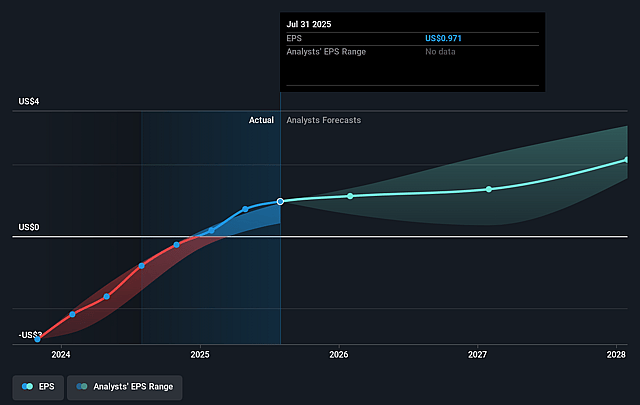

- Analysts expect earnings to reach $414.2 million (and earnings per share of $2.51) by about September 2028, up from $168.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $592.1 million in earnings, and the most bearish expecting $34 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 74.3x on those 2028 earnings, down from 94.2x today. This future PE is greater than the current PE for the US IT industry at 32.4x.

- Analysts expect the number of shares outstanding to grow by 3.78% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.89%, as per the Simply Wall St company report.

Okta Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing consolidation of the cybersecurity and identity markets-exemplified by platform companies like Palo Alto entering the space-could pressure Okta's market share and negotiating leverage, especially if large enterprises increasingly prefer integrated multi-function security suites over independent identity specialists; this trend risks long-term revenue growth and may impact Okta's ability to maintain pricing power.

- Okta's strategy of frequent product expansion (e.g., acquisition of Axiom Security and rapid feature rollout) introduces elevated product integration and execution risk; difficulties integrating new technologies and teams or falling behind in essential innovations (such as passwordless authentication or AI agent management) could erode Okta's competitive differentiation, putting downward pressure on revenue growth and gross margins.

- The continued focus on upsell and cross-sell to existing large enterprise and public sector customers, rather than driving robust new customer growth, may signal potential limitations in Okta's addressable market expansion; if new customer pipeline falters or churn increases due to past breaches or competitive switching, recurring revenue and long-term earnings durability could be negatively affected.

- International market expansion is being prioritized only in select top-10 countries to avoid spreading resources too thin; however, if Okta encounters increased regulatory complexity, data localization requirements, or stiffer competition from local or global players (especially with tightening global privacy laws), international growth may underperform, constraining total revenue and operating margin expansion opportunities.

- The rise of decentralized identity technologies (such as blockchain-based identity) and the growing commoditization of identity and access management tools via open-source or low-cost solutions could increase price-based competition and reduce Okta's revenue per customer; failure to differentiate sufficiently in this evolving landscape may suppress average contract values and compress net margins over time.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $120.917 for Okta based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $142.0, and the most bearish reporting a price target of just $75.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.6 billion, earnings will come to $414.2 million, and it would be trading on a PE ratio of 74.3x, assuming you use a discount rate of 8.9%.

- Given the current share price of $89.82, the analyst price target of $120.92 is 25.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Okta?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.