Advertisement

- United States

- /

- Software

- /

- NasdaqGS:PEGA

There's Reason For Concern Over Pegasystems Inc.'s (NASDAQ:PEGA) Price

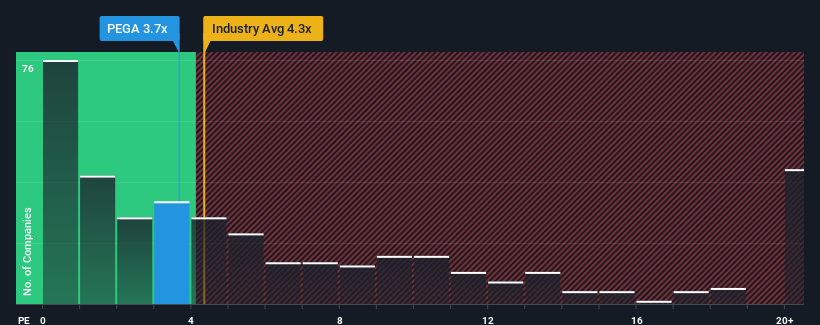

With a median price-to-sales (or "P/S") ratio of close to 4.3x in the Software industry in the United States, you could be forgiven for feeling indifferent about Pegasystems Inc.'s (NASDAQ:PEGA) P/S ratio of 3.7x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Pegasystems

What Does Pegasystems' Recent Performance Look Like?

With revenue growth that's inferior to most other companies of late, Pegasystems has been relatively sluggish. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Pegasystems.Do Revenue Forecasts Match The P/S Ratio?

The only time you'd be comfortable seeing a P/S like Pegasystems' is when the company's growth is tracking the industry closely.

If we review the last year of revenue growth, the company posted a worthy increase of 13%. Pleasingly, revenue has also lifted 35% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 8.6% per year over the next three years. With the industry predicted to deliver 15% growth each year, the company is positioned for a weaker revenue result.

In light of this, it's curious that Pegasystems' P/S sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

What We Can Learn From Pegasystems' P/S?

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Given that Pegasystems' revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. A positive change is needed in order to justify the current price-to-sales ratio.

And what about other risks? Every company has them, and we've spotted 5 warning signs for Pegasystems (of which 1 is significant!) you should know about.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:PEGA

Pegasystems

Develops, markets, licenses, hosts, and supports enterprise software in the United States, rest of the Americas, the United Kingdom, rest of Europe, the Middle East, Africa, and the Asia-Pacific.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8229.7% undervalued

72 followersusers have followed this narrative

5 commentsusers have commented on this narrative

34 likesusers have liked this narrative

WO

woodworthfund on Bumble ·

Swiped Left by Wall Street: The BMBL Rebound Trade

Fair Value:US$960.1% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Duolingo ·

Duolingo (DUOL): Why A 20% Drop Might Be The Entry Point We've Been Waiting For

Fair Value:US$268.6441.8% undervalued

43 followersusers have followed this narrative

5 commentsusers have commented on this narrative

9 likesusers have liked this narrative

AN

andre_santos on Ferrari ·

Ferrari's Intrinsic and Historical Valuation

Fair Value:€243.5626.4% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on Adobe ·

Adobe - A Fundamental and Historical Valuation

Fair Value:US$357.0514.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LE

LeStockPicker on Novo Nordisk ·

Probably the best stock I've seen all year.

Fair Value:DKK 90058.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DE

Deep_Insights on Hims & Hers Health ·

Hims & Hers Health aims for three dimensional revenue expansion

Fair Value:US$173.0281.9% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8229.7% undervalued

72 followersusers have followed this narrative

5 commentsusers have commented on this narrative

34 likesusers have liked this narrative

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.3% undervalued

72 followersusers have followed this narrative

15 commentsusers have commented on this narrative

23 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25464.9% overvalued

75 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

WA

Wane_Investment_House on Airtel Africa ·

Airtel Africa Plc – Recalibrated Valuation Highlights Compelling Relative Value Equity analysts highlight that Airtel’s stock remains undervalued relative to regional peers, presenting an attractive entry point for investors seeking exposure to a resilient, data-driven telecom business. Strategic Insights • Revenue Mix Transformation: The transition from voice to data highlights Airtel’s alignment with global telecom trends and positions the company to capture higher-margin opportunities in mobile data and digital services. • Operational Levers: Subscriber growth, tariff adjustments, and disciplined cost management provide a solid foundation for near-term growth. • Valuation Drivers: Adjustments to the equity risk premium (13.8% vs. 14.3%) and lower yields on Nigeria’s 10-year Eurobond (7.7% vs. 10.4%) have slightly tempered valuation, but the fundamentals remain strong. Analyst Commentary • Near-term Upside: The revised target price suggests significant potential gains, particularly given Airtel’s operational resilience and structural growth in data usage. • Investment Considerations: Investors seeking exposure to defensive growth in telecom should view Airtel as a long-term opportunity, with upside supported by undervaluation relative to regional peers. • Risk Factors: Currency appreciation (Naira strength), potential regulatory changes, and macroeconomic volatility remain key considerations for risk-adjusted returns. Conclusion Airtel Africa Plc combines robust operational performance, a favorable shift to data revenue, and strategic macro positioning with an undervalued stock price relative to peers. Despite muted market response in 2025, the recalibrated target price and potential upside of 72% underscore Airtel’s attractiveness for long-term investors seeking resilient, growth-oriented exposure in the African telecom sector.

0

|0