- South Africa

- /

- Pharma

- /

- JSE:APN

Aspen Pharmacare Holdings Limited (JSE:APN) Analysts Just Cut Their EPS Forecasts Substantially

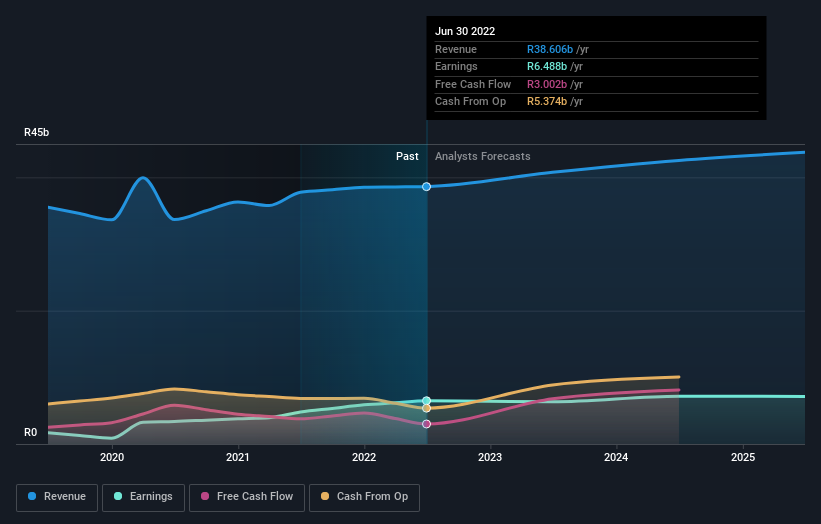

Market forces rained on the parade of Aspen Pharmacare Holdings Limited (JSE:APN) shareholders today, when the analysts downgraded their forecasts for this year. Both revenue and earnings per share (EPS) estimates were cut sharply as analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

After the downgrade, the three analysts covering Aspen Pharmacare Holdings are now predicting revenues of R41b in 2023. If met, this would reflect an okay 5.6% improvement in sales compared to the last 12 months. Statutory earnings per share are supposed to decrease 4.3% to R13.91 in the same period. Previously, the analysts had been modelling revenues of R49b and earnings per share (EPS) of R17.20 in 2023. Indeed, we can see that the analysts are a lot more bearish about Aspen Pharmacare Holdings' prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

View our latest analysis for Aspen Pharmacare Holdings

The consensus price target fell 9.2% to R199, with the weaker earnings outlook clearly leading analyst valuation estimates. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Aspen Pharmacare Holdings analyst has a price target of R210 per share, while the most pessimistic values it at R180. Still, with such a tight range of estimates, it suggests the analysts have a pretty good idea of what they think the company is worth.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Aspen Pharmacare Holdings' past performance and to peers in the same industry. One thing stands out from these estimates, which is that Aspen Pharmacare Holdings is forecast to grow faster in the future than it has in the past, with revenues expected to display 5.6% annualised growth until the end of 2023. If achieved, this would be a much better result than the 1.4% annual decline over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 5.0% per year. So while Aspen Pharmacare Holdings' revenues are expected to improve, it seems that it is expected to grow at about the same rate as the overall industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Aspen Pharmacare Holdings. There was also a drop in their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Aspen Pharmacare Holdings analysts - going out to 2025, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you're looking to trade Aspen Pharmacare Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:APN

Aspen Pharmacare Holdings

Manufactures and supplies specialty and branded pharmaceutical products worldwide.

Excellent balance sheet with reasonable growth potential.