Advertisement

- United States

- /

- Logistics

- /

- NYSE:UPS

United Parcel Service (NYSE:UPS) Is Paying Out A Larger Dividend Than Last Year

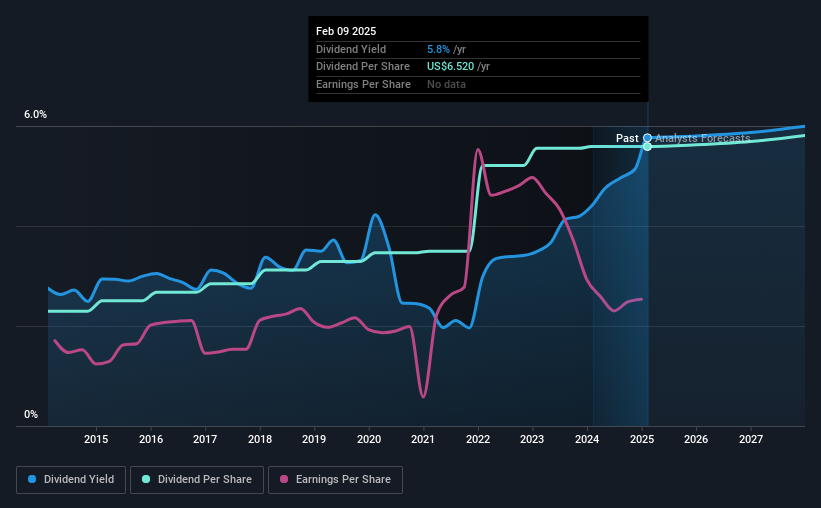

The board of United Parcel Service, Inc. (NYSE:UPS) has announced that the dividend on 6th of March will be increased to $1.64, which will be 0.6% higher than last year's payment of $1.63 which covered the same period. This makes the dividend yield 5.8%, which is above the industry average.

Check out our latest analysis for United Parcel Service

United Parcel Service's Future Dividend Projections Appear Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Based on the last payment, the dividend made up 90% of cash flows, but a higher proportion of net income. This indicates that the company could be more focused on returning cash to shareholders than reinvesting to grow the business.

Over the next year, EPS is forecast to expand by 38.7%. If recent patterns in the dividend continues, the payout ratio in 12 months could be 76% which is a bit high but can definitely be sustainable.

United Parcel Service Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2015, the dividend has gone from $2.68 total annually to $6.52. This means that it has been growing its distributions at 9.3% per annum over that time. Dividends have grown at a reasonable rate over this period, and without any major cuts in the payment over time, we think this is an attractive combination as it provides a nice boost to shareholder returns.

United Parcel Service May Have Challenges Growing The Dividend

The company's investors will be pleased to have been receiving dividend income for some time. It's encouraging to see that United Parcel Service has been growing its earnings per share at 5.7% a year over the past five years. Although per-share earnings are growing at a credible rate, the massive payout ratio may limit growth in the company's future dividend payments.

United Parcel Service's Dividend Doesn't Look Sustainable

In summary, while it's always good to see the dividend being raised, we don't think United Parcel Service's payments are rock solid. Although they have been consistent in the past, we think the payments are a little high to be sustained. This company is not in the top tier of income providing stocks.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. For instance, we've picked out 3 warning signs for United Parcel Service that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:UPS

United Parcel Service

A package delivery and logistics provider, offers transportation and delivery services.

Very undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Gaxos.ai: Early-Stage AI Innovator in Gaming & Health

Fair Value US$2.21|17.6% undervalued

JO

Community Contributor

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value US$500.00|1.1% overvalued

PI

Community Contributor

Amazon's Future Rises as Stock Price Falls: A Long-Term Investment Vision

Fair Value US$234.75|4.7% undervalued

ZW

Community Contributor