- United States

- /

- Logistics

- /

- NYSE:UPS

United Parcel Service (NYSE:UPS) Adds Multiple Co-Lead Underwriters for US$500 Million Offering

Reviewed by Simply Wall St

United Parcel Service (NYSE:UPS) recently announced changes to its fixed-income offering, including the addition of multiple banks as Co-Lead Underwriters for a $500 million offering. This restructuring effort corresponds with broader corporate strategies to strengthen financial foundations. The market's rise of 3.9% in the past week aligns with UPS's 6.4% share price increase, suggesting that while these underwriter additions may have contributed positively, they align with the broader market trend. Additionally, UPS's affirmation of a regular quarterly dividend of $1.64 per share may have further supported investor confidence during this period.

The recent announcement by United Parcel Service (UPS) regarding their fixed-income offering and the addition of Co-Lead Underwriters is positioned to complement broader financial strategies. This realignment of financial resources may bolster UPS's capacity to navigate the anticipated expansion in e-commerce and logistics automation, both key drivers outlined in the company's growth narrative. However, it's crucial to keep in mind potential risks such as rising labor and compliance costs, which could counteract these benefits. Over the past five years, UPS delivered a total return of 23.55%, indicating a solid performance despite the recent underperformance relative to the U.S. market's 11.6% gain over the past year.

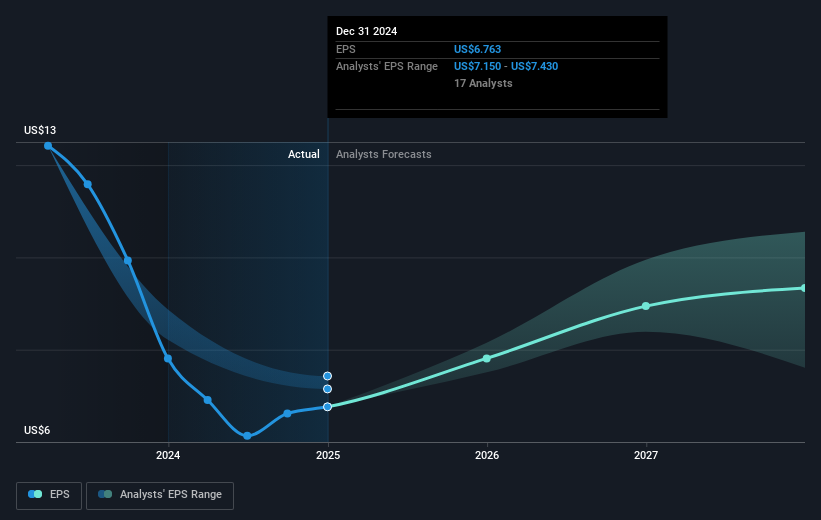

In the short run, UPS's share price exhibited a notable increase of 6.4% within a week, potentially influenced by the market's positive trend and further supported by the quarter's consistent dividend announcement of US$1.64 per share. This is against the backdrop where UPS's revenue is expected to grow at a slower rate than the broader market, emphasizing the importance of their strategic endeavors. The analyst consensus fair value places a price target of approximately US$116.29 on UPS's shares, while the more bullish view sets the target at US$149. With the current share price trailing at US$93.81, this provides a substantial room for potential valuation upside, contingent on achieving future earnings forecasts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade United Parcel Service, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:UPS

United Parcel Service

A package delivery and logistics provider, offers transportation and delivery services.

Undervalued with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives