Advertisement

- United States

- /

- Transportation

- /

- NYSE:UHAL

The Bull Case For U-Haul Holding (UHAL) Could Change Following Rising Revenue But Weakening Profitability

Simply Wall St

Reviewed by Sasha Jovanovic

- U-Haul Holding Company recently reported its second quarter and six-month earnings for 2025, showing higher revenue of US$1.72 billion for the quarter and US$3.35 billion for the six months but a significant decline in net income compared to the prior year.

- Alongside these results, U-Haul closed its long-operating Little Rock repair shop while opening a new, larger facility in North Little Rock, signaling a shift in regional operations and workforce allocation.

- With net income declining despite revenue growth, we'll assess how these results and operational changes could influence U-Haul's investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

U-Haul Holding Investment Narrative Recap

To be a shareholder in U-Haul Holding, you need to believe the company can balance rising revenue with improved profitability, even as ongoing competitive and cost pressures bear down on margins. The recent news of higher revenue but sharply lower net income in the second quarter does not appear to alter the most important short-term catalyst, the company's ability to address fleet and cost management, while highlighting that escalating operational expenses remain the biggest immediate risk. For now, the impact of these developments on the broader investment thesis is not material but highlights the need for careful cost discipline.

One recent announcement that stands out is the opening of U-Haul's new 30,000-square-foot repair shop in North Little Rock, which replaces the long-running Little Rock facility. This move underscores how U-Haul is shifting resources to support fleet operations, which ties directly into the company's efforts to resolve fleet imbalances, a key catalyst for future performance.

By contrast, investors should be aware that sustained increases in personnel and operating costs could still...

Read the full narrative on U-Haul Holding (it's free!)

U-Haul Holding's narrative projects $6.3 billion in revenue and $709.9 million in earnings by 2028. This requires 2.8% yearly revenue growth and a $342.8 million earnings increase from $367.1 million today.

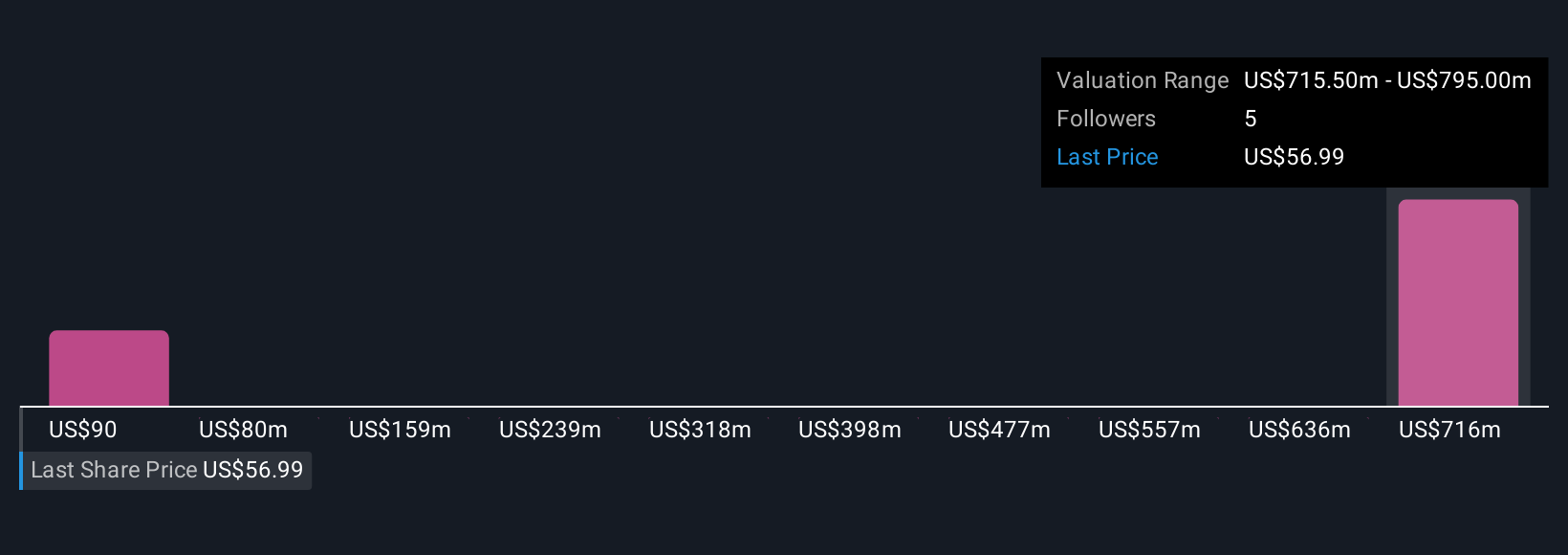

Uncover how U-Haul Holding's forecasts yield a $89.84 fair value, a 74% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community fair value estimates for U-Haul range from US$4.72 to US$89.84 across 2 analyses. With persistently higher operating costs weighing on recent results, your outlook may vary widely from others in the market.

Explore 2 other fair value estimates on U-Haul Holding - why the stock might be worth less than half the current price!

Build Your Own U-Haul Holding Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your U-Haul Holding research is our analysis highlighting 3 important warning signs that could impact your investment decision.

- Our free U-Haul Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate U-Haul Holding's overall financial health at a glance.

Seeking Other Investments?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:UHAL

U-Haul Holding

Operates as a do-it-yourself moving and storage operator for household and commercial goods in the United States and Canada.

Low risk with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor