- United States

- /

- Transportation

- /

- NYSE:UBER

Uber Technologies (UBER) Partners With Sephora For On-Demand Beauty Delivery Across North America

Uber Technologies (UBER) recently announced a partnership with Sephora to offer beauty products through Uber Eats. This collaboration enhances the company's platform and likely contributed to the stock's 10% rise last quarter, coinciding with other partnerships such as those with Best Buy and Dollar Tree. Additionally, a positive Q2 earnings report and share repurchase activities further supported investor confidence. While the broader market also saw an upswing, marked by record highs in the S&P 500 and Nasdaq, Uber's specific initiatives in retail expansion and delivery services augmented its stock performance amid a positive market trend.

The recent partnership between Uber Technologies and Sephora, alongside collaborations with Best Buy and Dollar Tree, underscores Uber's intent to diversify its offerings and capture a wider consumer base. This initiative could enhance future revenue streams by fulfilling consumer demand for convenient delivery options, potentially boosting both revenue and earnings forecasts. As Uber seeks to integrate more retail partners into its platform, these collaborations complement its core mobility and delivery services, possibly offsetting pressures from lower-margin segments.

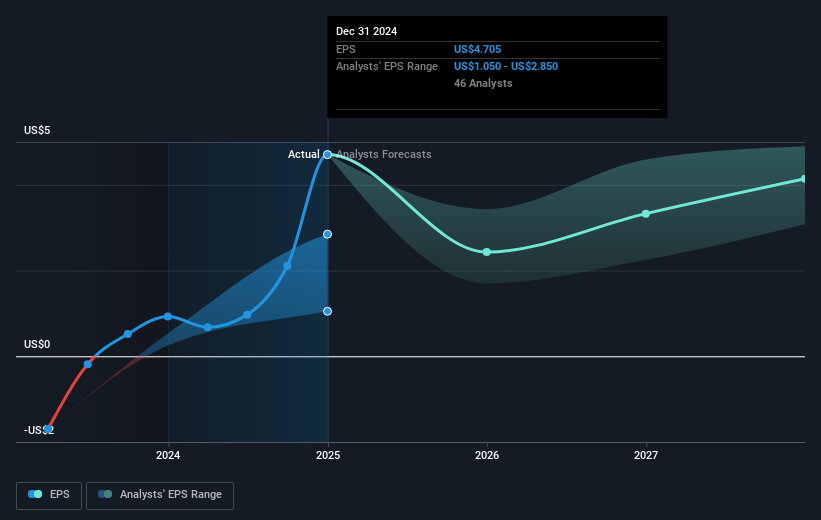

Over a three-year period, Uber's total shareholder return, including dividends, was 204.76%. This performance showcases significant appreciation relative to analysts' price target projections, indicating that the stock not only met but outperformed expectations. While Uber's share price is currently at $95.45, the consensus price target is $106.43, suggesting potential appreciation as analysts forecast revenue growth of 12.3% annually despite anticipated earnings decline over the next three years.

In the last year, Uber exceeded the US market return, which stood at 20%, positioning it favorably within the broader industry context. Despite the forecasted decline in earnings, the company's strategic ventures into high-margin services and cross-platform integration suggest a focus on sustaining competitive advantages. The ongoing scalability in autonomous vehicles and electrification efforts might shape its long-term earnings potential, which analysts anticipate could reach $9.7 billion by 2028. However, price target alignment with current valuation indicates room for market re-assessment based on evolving industry dynamics and operational execution.

Jump into the full analysis health report here for a deeper understanding of Uber Technologies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:UBER

Uber Technologies

Develops and operates proprietary technology applications in the United States, Canada, Latin America, Europe, the Middle East, Africa, and the Asia Pacific.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

When GPS fails: this small cap is fixing a $54B drone problem

Why Amdocs is a high conviction Buy for me?

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Recently Updated Narratives

302 Million Oz Silver Project in Mexico: Low Cost Underground Giant Ready to Explode

7/8/26 — Oscar Health: Trading 95.4% below Fair Value with +2070.2% Upside Potential

Procter & Gamble - A Fundamental Valuation

Popular Narratives

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

A wonderful business at reasonable price.

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Trending Discussion