- United States

- /

- Banks

- /

- NYSE:WAL

3 US Stocks That May Be Trading Below Estimated Value

Reviewed by Simply Wall St

As the U.S. stock market continues to navigate a mixed landscape with major indices showing varied movements, investors are keenly observing earnings reports and economic indicators for cues on potential opportunities. In such an environment, identifying stocks that may be trading below their estimated value can offer strategic entry points, particularly when the broader market exhibits signs of recovery or volatility.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Clear Secure (NYSE:YOU) | $27.08 | $53.36 | 49.2% |

| NBT Bancorp (NasdaqGS:NBTB) | $50.99 | $99.93 | 49% |

| First National (NasdaqCM:FXNC) | $23.66 | $46.63 | 49.3% |

| Peoples Financial Services (NasdaqGS:PFIS) | $58.76 | $115.39 | 49.1% |

| Synovus Financial (NYSE:SNV) | $58.67 | $115.67 | 49.3% |

| Equity Bancshares (NYSE:EQBK) | $49.21 | $98.42 | 50% |

| Pinterest (NYSE:PINS) | $30.51 | $59.52 | 48.7% |

| South Atlantic Bancshares (OTCPK:SABK) | $15.42 | $30.27 | 49.1% |

| Nutanix (NasdaqGS:NTNX) | $72.80 | $143.80 | 49.4% |

| Snap (NYSE:SNAP) | $11.60 | $22.72 | 49% |

We'll examine a selection from our screener results.

KeyCorp (NYSE:KEY)

Overview: KeyCorp is a holding company for KeyBank National Association, offering a range of retail and commercial banking products and services in the United States, with a market cap of approximately $19.43 billion.

Operations: The company generates revenue from its Consumer Bank segment, totaling $3.09 billion, and its Commercial Bank segment, amounting to $2.85 billion.

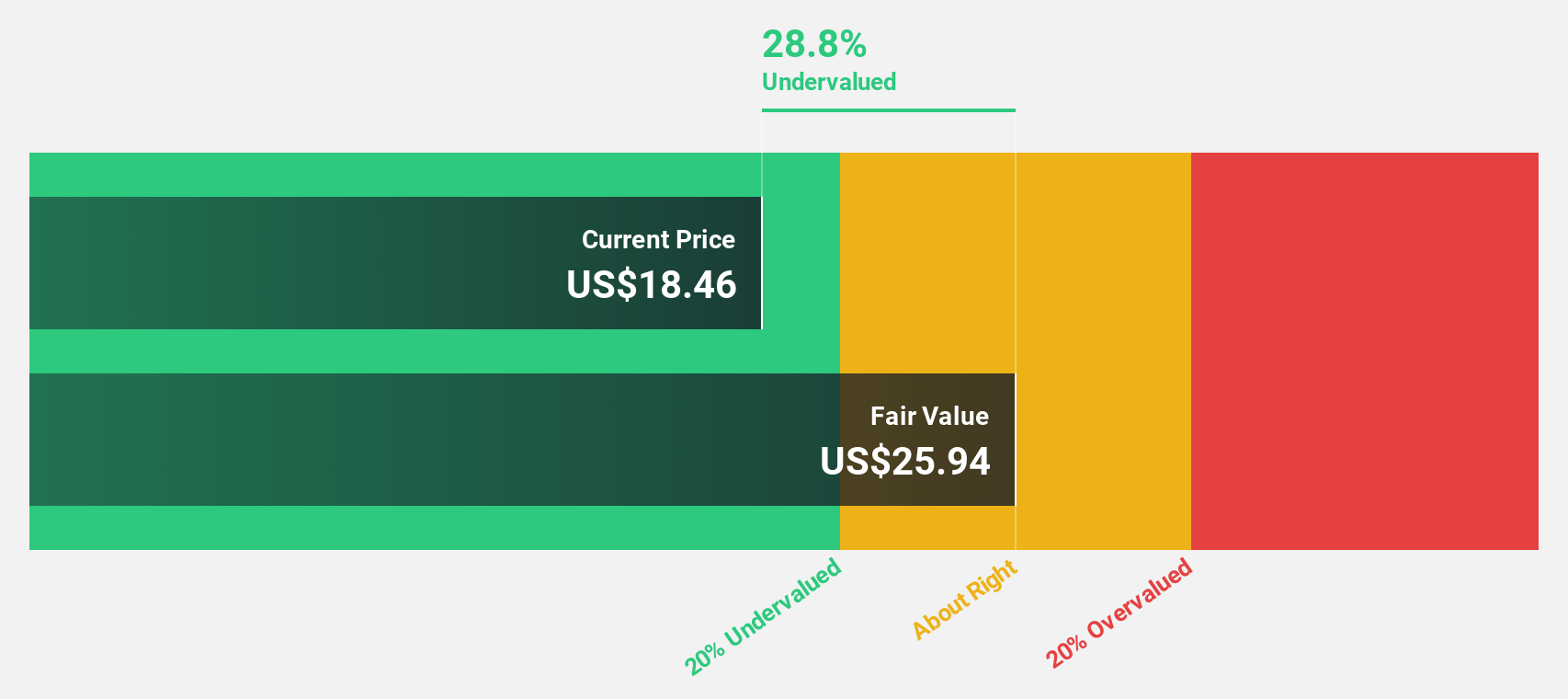

Estimated Discount To Fair Value: 28.5%

KeyCorp is trading at US$19.81, significantly below its estimated fair value of US$27.72, suggesting potential undervaluation based on discounted cash flow analysis. Despite a recent net loss and shareholder dilution, earnings are forecast to grow substantially at 71.7% annually, outpacing the market average. However, the current dividend yield of 4.14% may not be sustainable given coverage concerns and past profit margin declines from 18.8% to negative figures this year.

- In light of our recent growth report, it seems possible that KeyCorp's financial performance will exceed current levels.

- Click here and access our complete balance sheet health report to understand the dynamics of KeyCorp.

RXO (NYSE:RXO)

Overview: RXO, Inc. offers full truckload freight transportation brokering services and has a market cap of approximately $4.56 billion.

Operations: The company's revenue is primarily derived from its transportation segment, specifically trucking, which generates $3.86 billion.

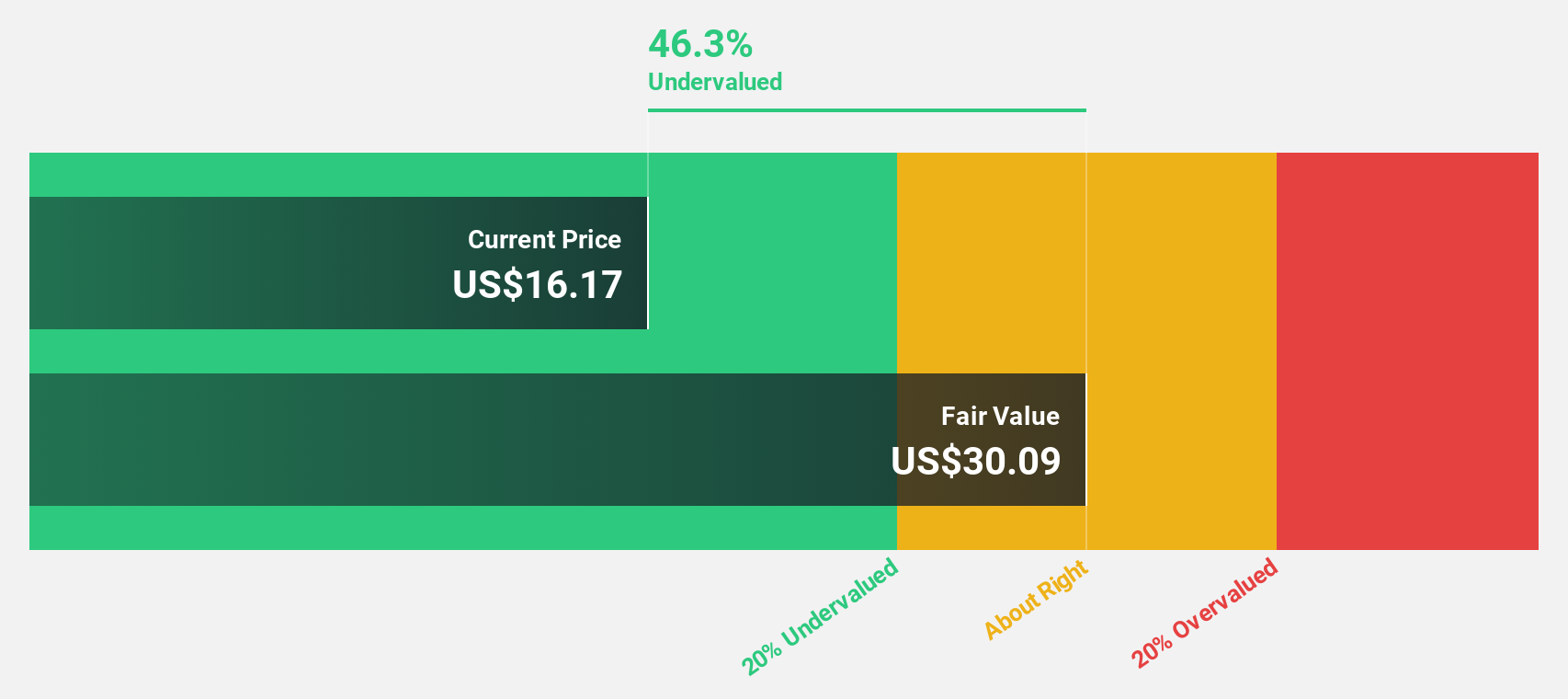

Estimated Discount To Fair Value: 22%

RXO, Inc. is trading at US$30.42, below its estimated fair value of US$39.01, indicating it may be undervalued based on discounted cash flow analysis. Despite recent net losses and shareholder dilution, RXO's revenue is projected to grow 22.4% annually, surpassing the market average of 8.9%. The company is expected to achieve profitability within three years with earnings growth forecasted at over 100% per year, although its future return on equity remains relatively low at 7.5%.

- Insights from our recent growth report point to a promising forecast for RXO's business outlook.

- Dive into the specifics of RXO here with our thorough financial health report.

Western Alliance Bancorporation (NYSE:WAL)

Overview: Western Alliance Bancorporation is a bank holding company for Western Alliance Bank, offering a range of banking products and services mainly in Arizona, California, and Nevada, with a market capitalization of approximately $10.21 billion.

Operations: Western Alliance Bancorporation's revenue is primarily derived from its Commercial segment at $1.19 billion and Consumer Related segment at $1.62 billion, with additional contributions from Corporate & Other at $106.60 million.

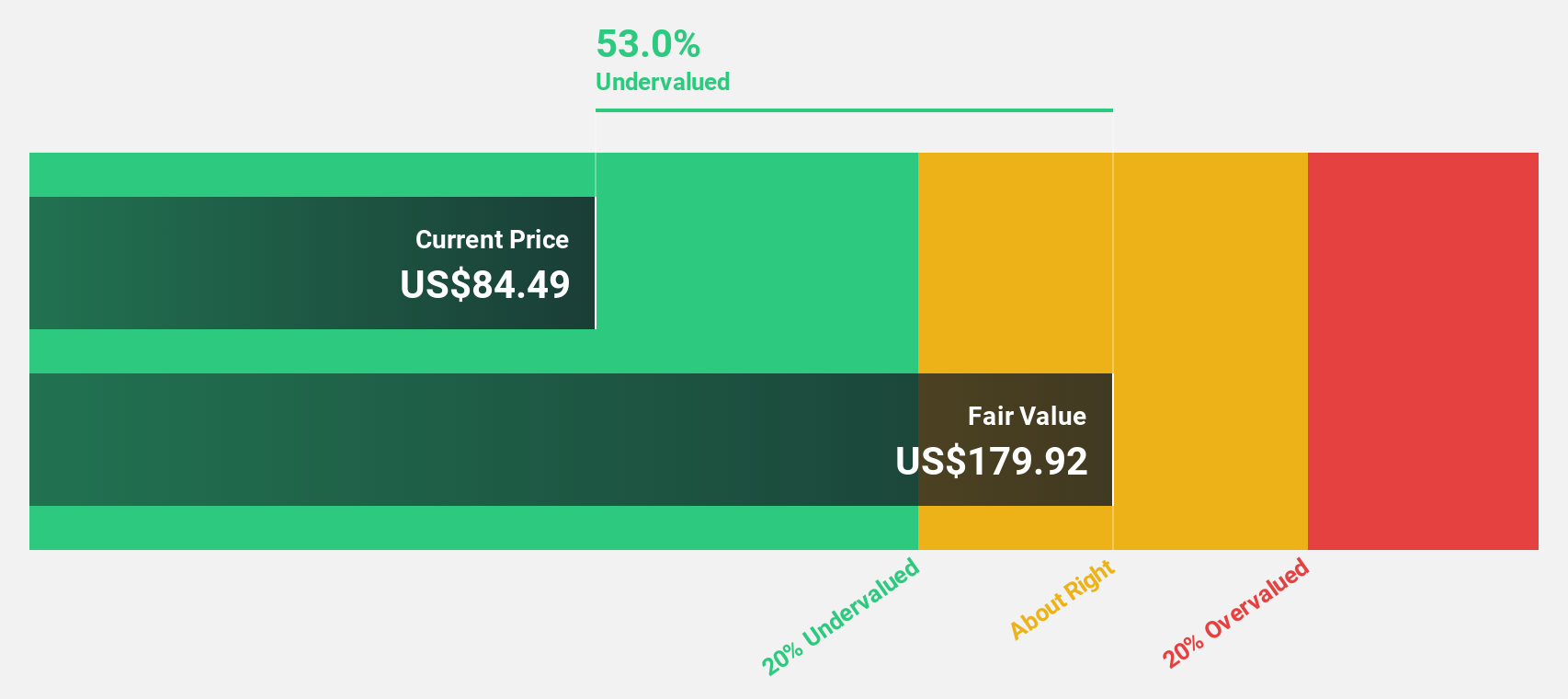

Estimated Discount To Fair Value: 43.3%

Western Alliance Bancorporation, trading at US$95.66, is significantly undervalued with a fair value estimate of US$168.63 based on discounted cash flows. Despite low return on equity forecasts (14.6%), its earnings are projected to grow 22.7% annually, outpacing the US market's growth rate of 15.4%. Recent earnings show net interest income growth but a slight decline in net income year-over-year, while insider selling has been significant in the past quarter.

- Our comprehensive growth report raises the possibility that Western Alliance Bancorporation is poised for substantial financial growth.

- Navigate through the intricacies of Western Alliance Bancorporation with our comprehensive financial health report here.

Make It Happen

- Unlock more gems! Our Undervalued US Stocks Based On Cash Flows screener has unearthed 192 more companies for you to explore.Click here to unveil our expertly curated list of 195 Undervalued US Stocks Based On Cash Flows.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Western Alliance Bancorporation might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WAL

Western Alliance Bancorporation

Operates as the bank holding company for Western Alliance Bank that provides various banking products and related services primarily in Arizona, California, and Nevada.

Excellent balance sheet and good value.