Quote of the Week: “Many forms of Government have been tried, and will be tried in this world of sin and woe. No one pretends that democracy is perfect or all-wise. Indeed , it has been said that democracy is the worst form of Government, except for all those other forms that have been tried from time to time.” - Winston S Churchill

Donald Trump and the Republican Party made a clean sweep in the US election. Some aspects of Trump’s campaign were a little vague, but we can be fairly certain of lower taxes and deregulation.

That, and the strong US economy, should lead to higher corporate profits. On the other hand, the policies he plans to enact could be inflationary, and US government debt doesn’t look like it’s coming down anytime soon.

This week we are having a look at what a second Trump presidency could mean for investors in the US and elsewhere.

🎧 Would you prefer to listen to these insights? You can find the audio version on our Spotify, Apple Podcasts or our YouTube!

What Happened in Markets this Week?

Here’s a quick summary of what’s been going on:

-

⛏️ Gold price falls most since 2022 as investors pile into equities ( CNBC )

- What’s our take?

- This is a more typical ‘risk on’ reaction.

- Gold has rallied along with stocks throughout 2024, and the price was up 39% YTD before the election. That’s unusual, as gold typically outperforms during periods of uncertainty.

- But gold is also regarded as an inflation hedge. Now that expectations for inflation are rising again, we’ll have to see what that means for the gold price. It’s likely that investors decided to take profits on gold and put that money into more obvious short term trades. If that’s the case they have created an opportunity for gold bulls.

- What’s our take?

-

🪙 iShares Bitcoin ETF is now bigger than its gold counterpart ( CNBC )

- What’s our take?

- This could be a sign of changing tides for cryptocurrencies.

- Trump’s election win has spurred on a Bitcoin rally as the cryptocurrency surged to new all-time highs. Investors were likely encouraged by expectations that the Trump administration could be crypto-friendly, given Trump himself spoke at the 2024 Bitcoin Conference.

- The recent surge could also be explained by investors gravitating towards Bitcoin as a hedge against the US dollar, in the event that Trump’s proposed tariffs have an inflationary effect and ultimately devalue the dollar. Interestingly, the US dollar also hit a 1-year high this week.

- What’s our take?

-

💸 China sells USD bonds in Saudi Arabia ( FT )

- What’s our take?

- The USD remains the go-to currency for lenders and borrowers alike.

- An auction of $2 billion worth of government bonds by the Chinese Finance Ministry was 20 times oversubscribed. The 3 and 5-year bonds were sold with yields only slightly higher than equivalent US treasuries. That could mean investors believe the credit quality of both nations is the same - or that investors are happy with a little more diversification.

- China usually holds bond auctions in Hong Kong but held this one in Saudi Arabia for the first time. This could be an effort to build closer ties with investors in the country.

- This bond issue was tiny compared to China’s overall funding program. But the strong demand shows that appetite for USD denominated bonds is as strong as ever.

- What’s our take?

-

💰 Buffett’s Berkshire Is Being Packaged Into a Leveraged ETF ( Bloomberg )

- What’s our take?

- The Sage of Omaha probably wouldn’t approve.

- When you buy a leveraged instrument, you are effectively borrowing money to increase buying power. Since Berkshire Hathaway is sitting on a huge pile of cash, you would effectively be borrowing cash to invest in… cash.

- On top of that, the funding rate you would effectively be paying would be a hurdle. Unless Berkshire outperforms that funding rate, returns could end up being underwhelming.

- What’s our take?

-

🏗️ Homebuilder deal activity is surging, fueled by major Japanese buyers ( CNBC )

- What’s our take?

- Japanese efficiency could revolutionize the homebuilder market.

- Record-high housing demand in the U.S. has led to a rush of M&A activity among homebuilders. What’s more interesting is that almost half the deals are with Japanese companies according to Whelan Advisory, which makes sense when you consider Japan’s low-growth environment and low cost of capital.

- Japanese firms like Sekisui House are making inroads by acquiring major U.S. builders such as MDC Holdings, hoping to bring their advanced value engineering and efficiency techniques to the American market. It’s likely that other Japanese companies will follow suit, which could shake up the homebuilding processes and make housing more affordable through innovations like 3-D imaging and pre-cut materials.

- What’s our take?

-

📉 US Inflation ticks up while jobless claims fall to lowest in six months ( Reuters )

- What’s our take?

- The rate cut journey won’t be all smooth sailing. Expect a few twists and turns along the way.

- Stubborn inflation and a reduction in first-time unemployment benefit applications are challenging the Federal Reserve's plans for aggressive rate cuts.

- Economists still expect a rate cut in December, but are now expecting a shallower rate-cutting cycle heading in to 2025. It’s expected that tariffs from President-elect Trump's incoming administration will add upward pressure on inflation and complicate the Fed's decision-making process.

- In our view, the Fed is likely to opt for fewer rate cuts in 2025 than previously projected, carefully balancing the risks of persistent inflation against the need to support economic growth.

- What’s our take?

-

⚖️ Meta hit with €797 million EU fine for breaking antitrust rules ( Fortune )

- What’s our take?

- Big tech income statements need a new line item: ‘EU Fines’

- The EU's hefty €797 million fine against Meta for antitrust violations is a huge escalation in regulatory scrutiny over Big Tech's market practices.

- Meta's defense - that users engage with Facebook Marketplace by choice and not compulsion - seems to overlook the EU's concern about automatic access potentially stifling competition, particularly among competitors that advertise on Meta’s platforms.

- EU regulators are well armed in their fight against Big Tech, with major twin laws, the Digital Services Act and the Digital Markets Act, that carry massive financial penalties in the event of infringements. Don’t expect this to be the last time a tech giant butts heads with EU regulators and has to cough up some cash.

- What’s our take?

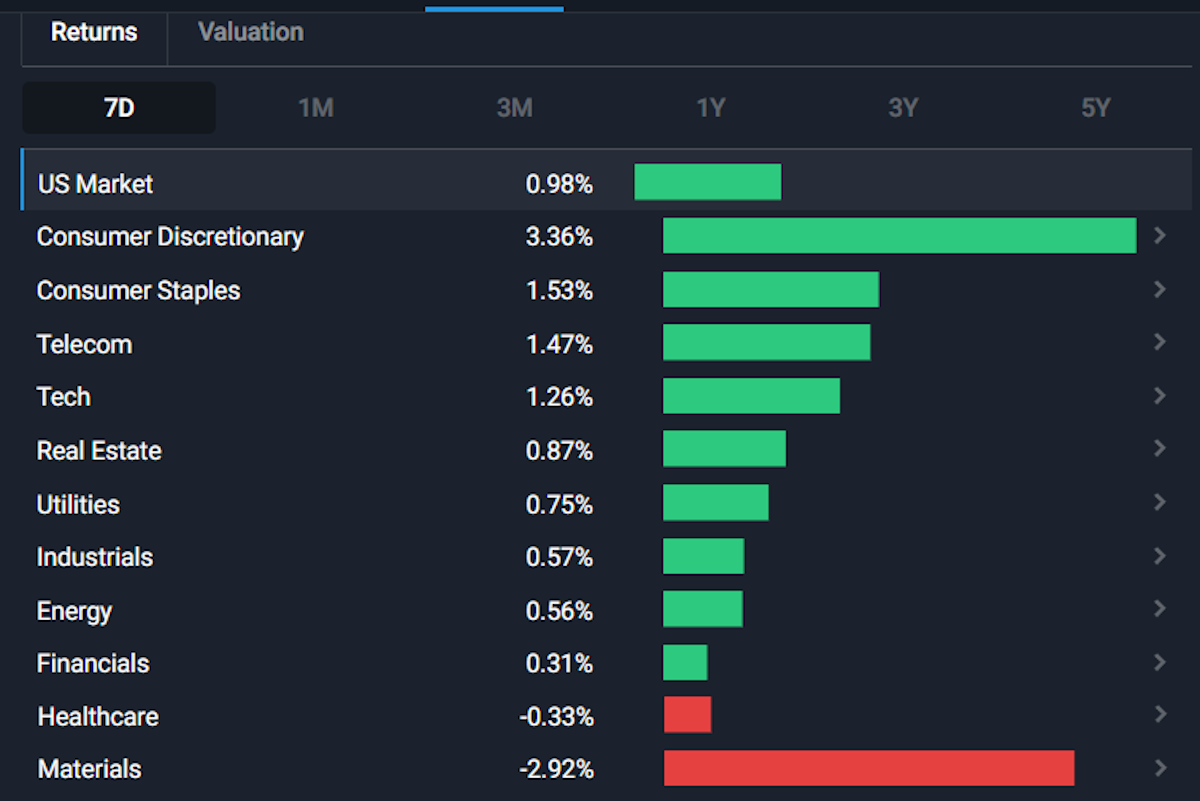

🇺🇸 The Trump 2.0 Stock Market

US equities rallied when it became clear that Donald Trump would be returning to the White House. The market’s response was in part a relief rally after the outcome became clear early on, but some sectors certainly began to price in Trump’s pro-business stance.

As we’ve mentioned previously, elections tend to have less impact on the overall economy and stock market than leaders like to think. But, this election could be more consequential than usual for a few reasons:

- The result gave Donald Trump a clear mandate to govern.

- His campaign platform included some promises that are far more radical than prior elections.

- The GOP controls the White House, the Senate and the House. This will make it easier to pass legislation without votes from Democrats.

- This isn’t his first rodeo. Donald Trump hasn’t wasted any time nominating people for key roles, and he appears to have a plan to hit the ground running on day one.

In short, the market appears to be anticipating higher growth, along with higher inflation and interest rates. The way things actually play out will depend on if, when, and how his policies are implemented.

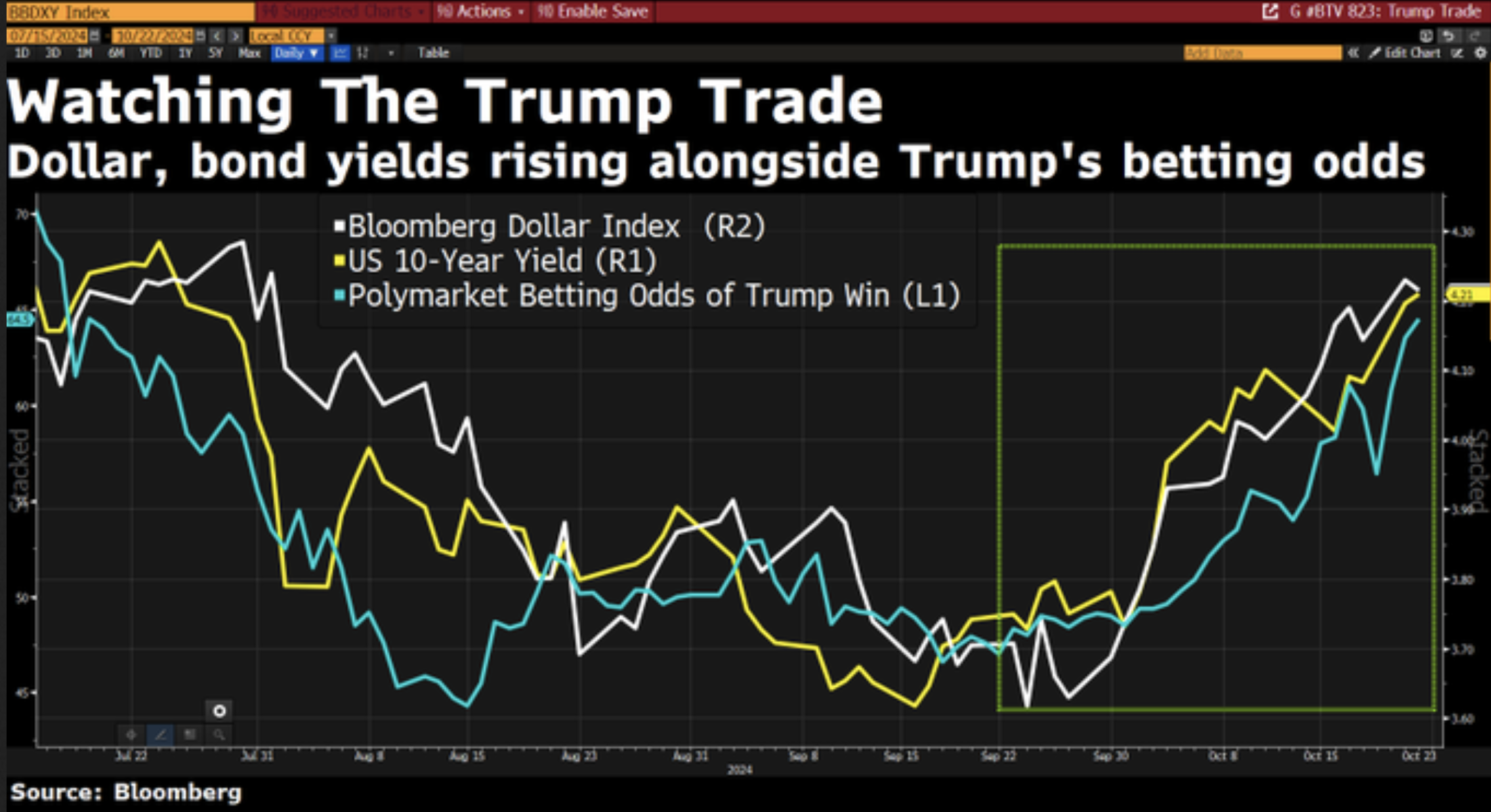

📈 Inflation and Interest Rates

In the run-up to the election, investors were aware that a Trump Presidency could lead to a rebound in inflation. The yield on 10-year treasuries rose as Trump’s poll numbers and the odds on betting platforms rose. This also occurred after the Fed cut rates by 50 basis points.

Two of Donald Trump’s biggest election promises were the mass deportation of illegal immigrants and tariffs on imports to the US. Both would probably be inflationary, depending on how or when they are implemented.

💱 Tariffs

Trump has pledged to impose a 10% tariff on all imports, and a 60% tariff on goods from China. Tariffs would result in higher prices for US businesses and consumers. Tariffs would also incentivize local manufacturing, but it’s unlikely that prices would be competitive with low-cost manufacturing hubs, even with the tariff.

Import duties result in a one-time increase in inflation, but inflation tends to ripple through the entire economy. The inflationary effect could also be offset - or amplified - by whatever happens to energy prices and the USD at the time.

✨ A new round of tariffs could also result in trade partners responding with tariffs of their own. That would hurt US exporters - but could also lead to new trade deals being negotiated.

🛫 Mass Deportations

It’s estimated that there are 10 million or more undocumented immigrants in the US, many of whom are part of the labor force. Plans to deport these people at a time when the unemployment rate is historically low could result in a labor shortage. That would be good news for US workers, particularly those in low-paying jobs.

However, it would also be inflationary, and could leave companies struggling to replace workers.

The sectors that would be most affected include hospitality , construction , and agriculture where most undocumented immigrants work.

In the case of both tariffs and deportations, the impact will depend on how far and how fast the administration implements these policies. The market will probably be quick to react, in which case implementation may be reassessed.

Which companies would be shielded or benefit from these policies? Companies with little exposure to imports, and those that benefit from higher interest rates. would be best positioned. This includes smaller companies, banks and technology companies.

✨ On the losing side of the equation, the valuations on growth stocks with high multiples and little to no earnings may need to adjust to higher discount rates.

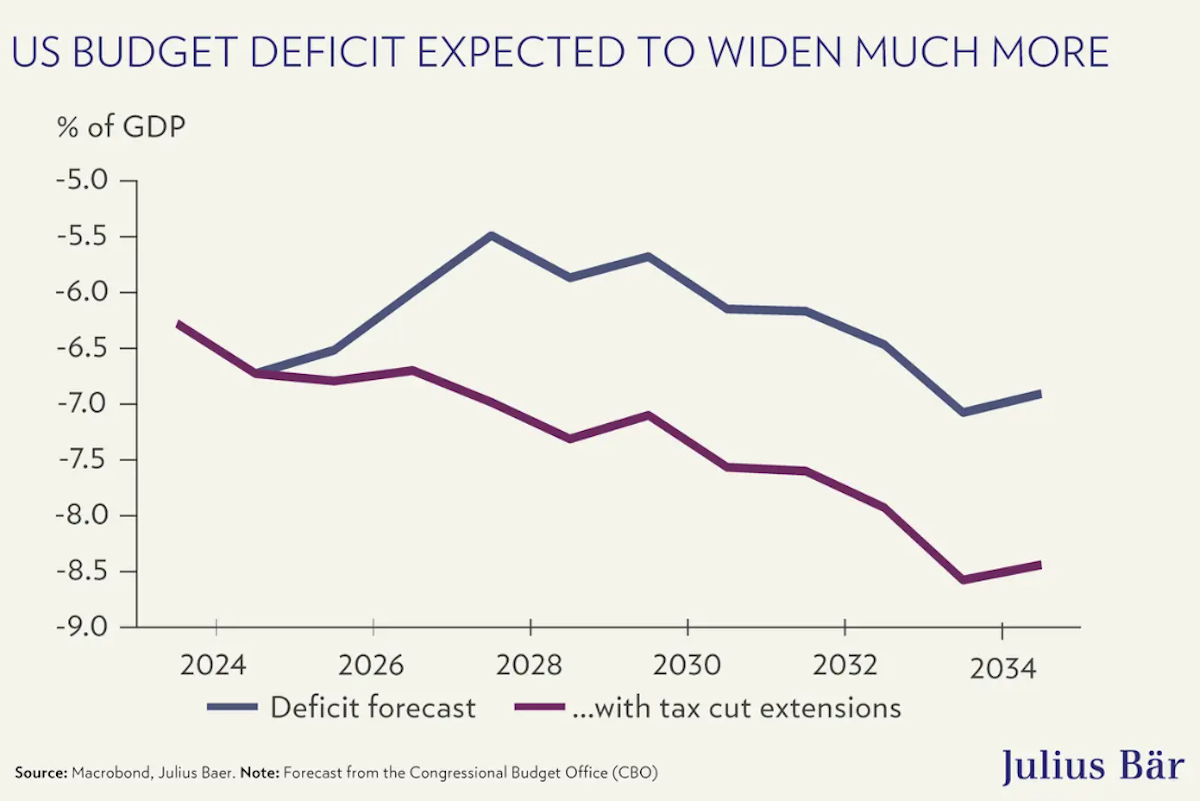

💰 Tax Cuts and Deficits

The US national debt used to be a big talking point for politicians. The topic barely came up during this election cycle, and it looks like it will be a problem for the winner of the 2028 election to deal with.

Tax cuts were another key part of Trump’s campaign. He intends to extend the tax cuts he made in 2017 which are due to expire at the end of 2025. He has also pledged to make other tax cuts for individuals and businesses.

With Republicans in control of both branches of Congress, there should be little resistance to these extensions and new tax cuts. That means the budget deficit will widen unless corresponding spending cuts are made.

Trump has also pledged to cut wasteful and unnecessary spending, but it's unlikely that spending cuts will offset lower tax rates. So unless corporate profits and incomes rise enough to offset the lower tax rates, US government debt is going to continue to rise.

Higher deficits mean more supply in the bond market (i.e. higher yields), and rising inflation expectations also mean higher yields. Let’s hope there’s still an appetite for those bonds.

⚡ Energy

It’s no surprise to see Trump pledging to drill, drill, drill, and increase US oil and gas production. OPEC members can’t be happy about that as they cut production to support the price.

Oil and gas stocks responded positively to Trump’s win, but we will have to see how it actually translates to profits. More supply would result in lower oil and gas prices, and the largest oil producers are currently aiming to be leaner and more profitable, rather than as big as possible.

Still, it’s probably inevitable that new investments in production and refining capacity will be made. This could be good news for oil and gas service companies - have a look at this Oil and Gas screener for some ideas in that space.

It’s also no surprise to see renewable energy stocks on the back foot. Trump isn’t a fan of wind or solar, and he’s also pledged to unwind the Inflation Reduction Act which makes funding and tax credits available for clean energy production. Ending this legislation may be tricky, as some of its programs are popular and have created jobs.

Regardless of what happens to the IRA, it's probably safe to say that there won’t be many new incentives for solar and wind energy. We will have to see what happens to tax credits for EVs now that Elon Musk is an advisor to the incoming administration. Early reports seem to indicate that the Trump administration wants to kill off the EV tax credits , which is interesting, as that’d actually impact American EV manufacturers more than it would foreign competitors.

Solar and wind projects have already reached a point where subsidizing them was becoming too expensive. It’s now a question of market dynamics. Some of the leading solar panel manufacturers have already moved production to the US - which means tariffs on Chinese imports help them.

Solar stocks have been among the worst performers of 2024 - at some point the price might be right.

The re-emerging nuclear energy industry could benefit during the Trump presidency. Trump is in favor of nuclear - and of deregulation. This is a key point as nuclear projects face regulatory hurdles - many of which have nothing to do with safety. Amazon’s proposed deal with Talen Energy was recently blocked by regulators. Be sure to check out our screener for US Nuclear stocks that could be big winners with greater deregulation.

🪙 The Bitcoin President

After previously calling Bitcoin a scam, Donald Trump has now embraced the world of cryptocurrencies. He’s hinted at building a strategic reserve of 1 million Bitcoin. The US government already controls 200,000 Bitcoin which were confiscated from Silk Road, so that leaves another 800,000 which is most of what's left to be mined.

Building up a reserve like that would probably force other countries, or their central banks, to do the same. But they would also need to accept the potential volatility and work out how to fund those purchases.

For the rest of the crypto industry, a more accommodating stance would also be very welcome. The lack of clear policies and regulations is holding the industry back as much as it’s preventing wider adoption. Proper regulation would allow traditional assets to be tokenized, and bring cryptocurrencies into the mainstream financial system.

How far Trump plans to go isn’t clear yet - but there could be big changes on the horizon.

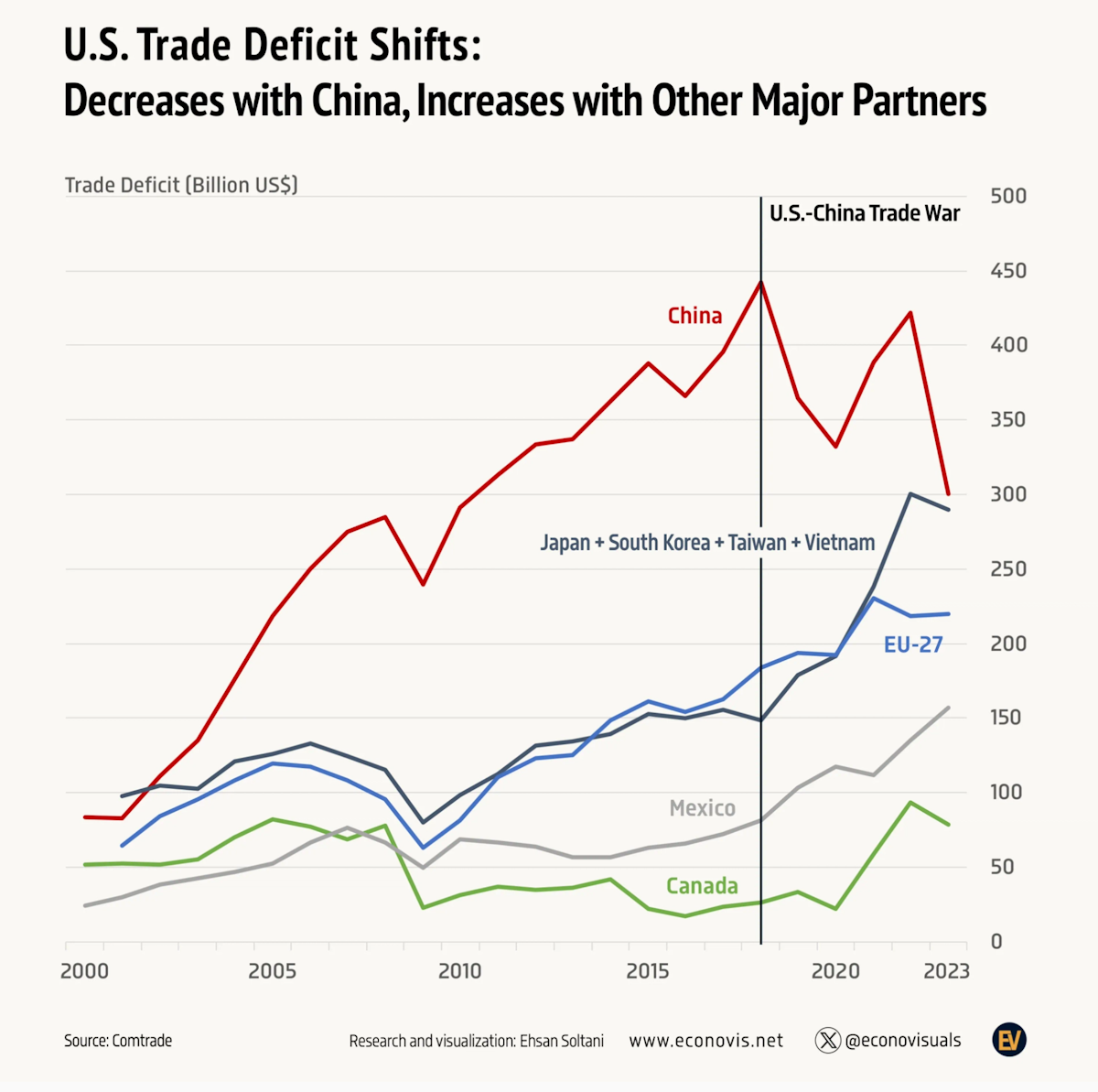

🌏 The Global Economy

Trump’s first trade war with China resulted in less trade between the two countries, but it also led to more trade with other partners, and particularly with other low-cost manufacturing hubs like Mexico, Vietnam, and Indonesia.

What happens now will depend on the next round of tariffs. If a 60% duty is imposed on China, with just 10% on imports from elsewhere, it could be a positive for countries like Mexico. If tariffs are equal across the board it’ll probably hurt a lot of global business.

✨ Emerging economies are also contending with a strong USD (which makes their imports more expensive) and the prospects of higher rates. This is happening just as those countries were hoping for lower rates and increasing demand.

Trump’s election is ushering in another round of de-globalization. That means companies and countries with less dependence on US trade may be better off. India is one country that stands out, as it’s less exposed to US trade and has a growing local economy. Elsewhere, companies with a local focus like banks, retailers, and food producers should be less exposed.

💡 The Insight: Expect The Unexpected

As mentioned, this could be one of the more consequential elections for the US economy and for the global economy. But market forces sometimes get in the way of policy implementation.

For investors, it’s worth treading cautiously rather than assuming any particular outcome. The higher for longer scenario for inflation and interest rates seems likely - but the outlook for cryptocurrencies, energy and other parts of the economy could be quite fluid.

Dollar-cost averaging is a good way to approach a changing market environment. By staggering your buys and sells, you take trying to ‘time the market’ off the table, and you can adjust your plan if necessary.

There are some sectors and industries that we haven't mentioned here, including healthcare and defense. Right now, there isn’t a lot of clarity on what Trump’s second term could mean for those sectors. The potential impact of deregulation will also depend on who ultimately gets appointed to key positions. We will do a follow-up in the new year if, or when, there is more clarity.

Key Events During The Next Week

Tuesday

- 🇨🇦 Canada’s inflation rate is expected to come in at 1.9%, up from 1.6% last month.

- 🇺🇸 US building permits are expected to rise from 1.42 million to 1.49 million.

Wednesday

- 🇬🇧 UK inflation is also forecast to edge higher. Economists expect year on year inflation to be 2%, compared to 1.7% in September.

Friday

- 🇬🇧 UK retail sales data will be published.

- 🇺🇸 The US Michigan Consumer Sentiment index is forecast to rise from 70 to 73.

Nvidia reports on Wednesday, so this week probably qualifies as the peak of earnings season. Retailers and cloud software companies are also beginning to report their numbers for Q3.

The biggest companies reporting include:

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.