Advertisement

- United States

- /

- Transportation

- /

- NYSE:NSC

Norfolk Southern (NSC): Assessing Valuation After a Quiet Month of Share Price Gains

Simply Wall St

Reviewed by Simply Wall St

Norfolk Southern (NSC) shares have quietly pushed higher over the past month, and that steady climb is starting to draw fresh attention from investors comparing rail stocks to the broader market.

See our latest analysis for Norfolk Southern.

That recent strength sits on top of a solid run, with the share price now at $294.05 and a robust year to date share price return suggesting momentum is still building rather than fading, backed by a steady multi year total shareholder return profile.

If Norfolk Southern’s climb has you thinking more broadly about transport and industrial trends, it could be a good moment to explore auto manufacturers as another way to find potential opportunities.

With shares near record highs, solid double digit returns, and only a modest gap to analyst targets, investors now face the key question: is Norfolk Southern still undervalued or has the market already priced in its future growth?

Most Popular Narrative Narrative: 6% Undervalued

With Norfolk Southern last closing at $294.05 against a narrative fair value near $311.68, the prevailing view leans toward upside still being on the table.

The commitment to $150 million in productivity and cost reduction initiatives over three years is being propelled by better labor productivity and fuel efficiency, which are anticipated to sustain EPS growth even if revenue growth slows. The company's focus on increasing customer confidence through consistent service improvements is leading to meaningful market share gains, particularly in merchandise and intermodal segments, which could bolster future revenue growth.

Curious how modest revenue growth, shifting margins, and a richer future earnings multiple combine to support that price tag? The narrative’s assumptions may surprise you.

Result: Fair Value of $311.68 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, storm related restoration costs and weaker export coal pricing could pressure margins and volumes, challenging the optimistic earnings and valuation assumptions embedded in this narrative.

Find out about the key risks to this Norfolk Southern narrative.

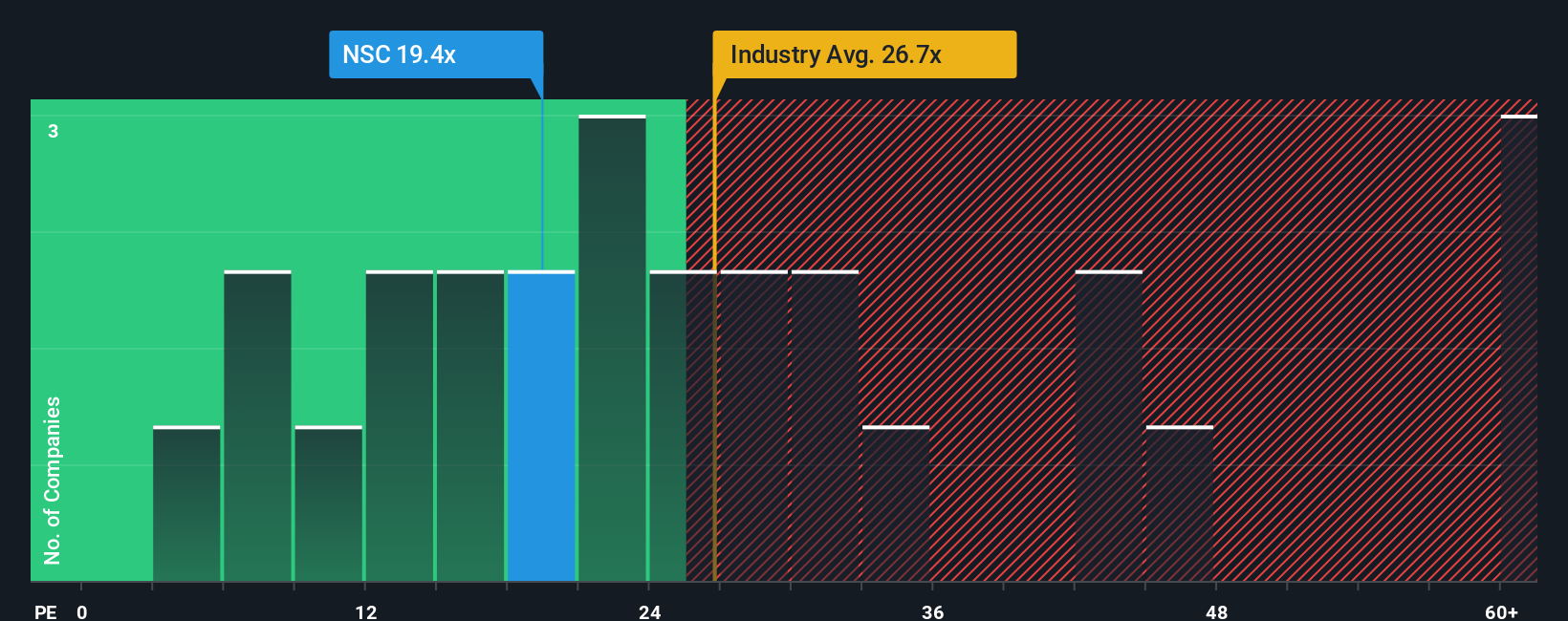

Another View: Market Ratios Flash a Caution Light

While the narrative fair value points to upside, our earnings based lens tells a more cautious story. NSC trades on a 22.3x P/E versus a fair ratio of 18.2x and only slightly above peers at 22.1x, suggesting limited margin for error if growth disappoints.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Norfolk Southern Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in just minutes. Do it your way.

A great starting point for your Norfolk Southern research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, put Simply Wall Street’s powerful Screener to work so you do not miss stocks that match your strategy and risk profile.

- Explore these 3571 penny stocks with strong financials that already show strong underlying financial health instead of mere speculative hype.

- Look into these 25 AI penny stocks that combine expansion with earnings strength in automation and intelligent software.

- Review these 919 undervalued stocks based on cash flows that markets may be mispricing relative to their long-term fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Norfolk Southern might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NSC

Norfolk Southern

Engages in the rail transportation of raw materials, intermediate products, and finished goods in the United States.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

35 followersusers have followed this narrative

6 commentsusers have commented on this narrative

10 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

113 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative