Advertisement

- United States

- /

- Logistics

- /

- NYSE:FDX

Is FedEx’s Valuation Attractive After CEO’s High-Profile China Business Trip?

Simply Wall St

Reviewed by Simply Wall St

If you are watching FedEx stock right now, you have probably noticed it has been a rollercoaster. After a difficult run over the past year, with the stock down about 22% in total return, many investors are asking if all the bad news is priced in or if there is still some rough air ahead. Even so, not everything about FDX is headed south. In the last three months, the stock has shown signs of life with a 4% gain, which stands out against a challenging logistics sector.

Part of the recent action comes from major headlines, like CEO Rajesh Subramaniam leading a top-level U.S. executive trip to China, and ongoing internal shake-ups in FedEx’s leadership team. Meanwhile, the company’s push into automation, such as warehouse robots handling the heavy lifting, is aimed at cutting costs and boosting efficiency for the long run. Investors are watching closely to see if these changes will really move the profit needle.

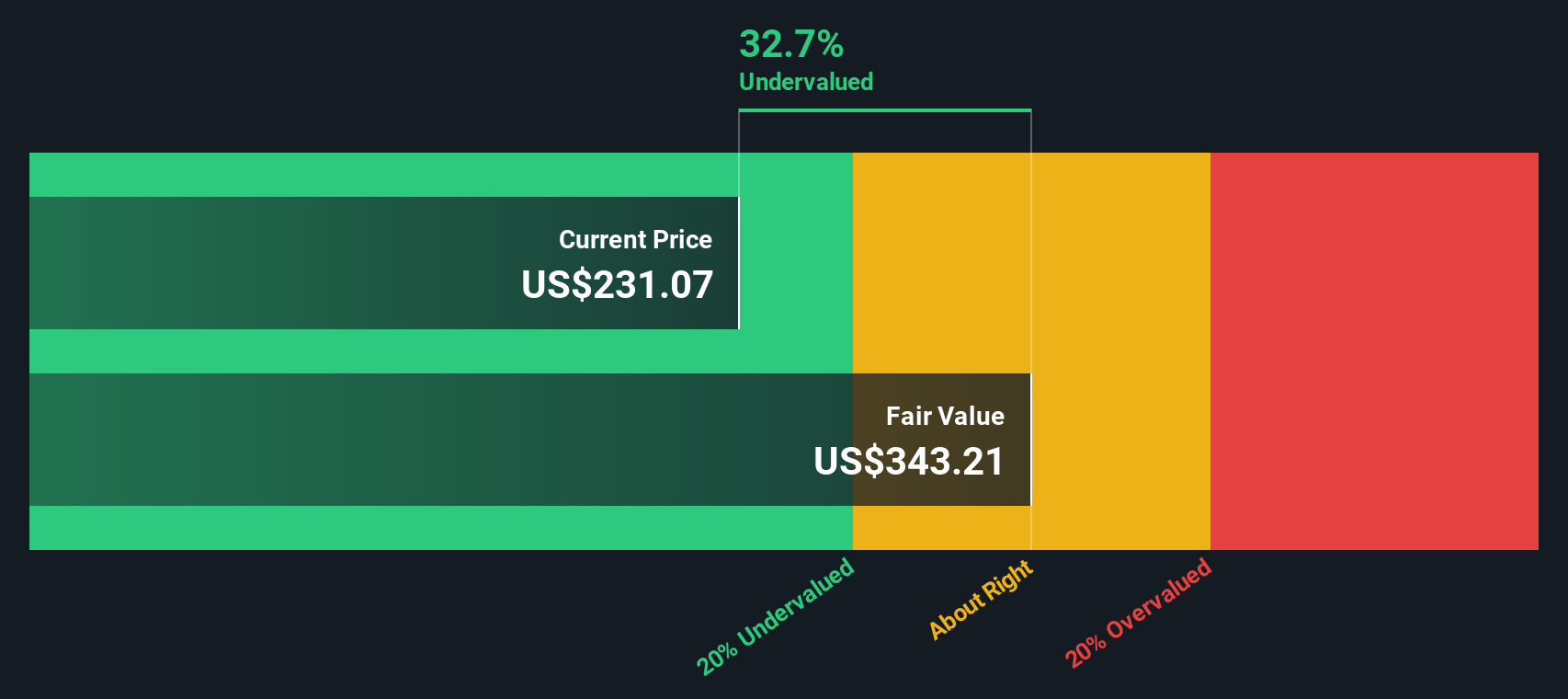

Of course, all eyes are on the numbers. Right now, FedEx trades at about $225, nearly 18% below the average analyst price target and with a hefty 34.2% discount to its own estimated intrinsic value. Our valuation screening puts FedEx at 5 out of 6 checks for being undervalued, which is no small feat in today’s market. So how do you actually decide what to do with FDX, especially if you care about value and not just momentum?

Coming up, we will dig into each valuation approach to show exactly where FedEx stands. Then we will share a broader perspective that makes valuation analysis even more actionable than you might expect.

FedEx delivered -21.8% returns over the last year. See how this stacks up to the rest of the Logistics industry.Approach 1: FedEx Cash Flows

The Discounted Cash Flow (DCF) model is designed to forecast how much cash a business will generate in the future, then discount that stream of cash back to its present value. This approach helps investors assess whether a stock’s current price fairly reflects its long-term earning potential.

For FedEx, current Free Cash Flow stands at just under $2 billion. Analysts see this cash flow increasing steadily, reaching almost $4.48 billion within five years and projecting further growth through 2035. Using a Two-Stage Free Cash Flow to Equity model, these projections yield an estimated intrinsic value of $342.39 per share.

With FedEx shares recently trading around $225, the DCF model suggests the stock is 34.2% undervalued compared to projected future cash flows. This indicates that FedEx’s long-term profit potential may not be fully reflected in its current market price and may present a margin of safety for value-oriented investors.

Result: UNDERVALUED

Approach 2: FedEx Price vs Earnings (PE)

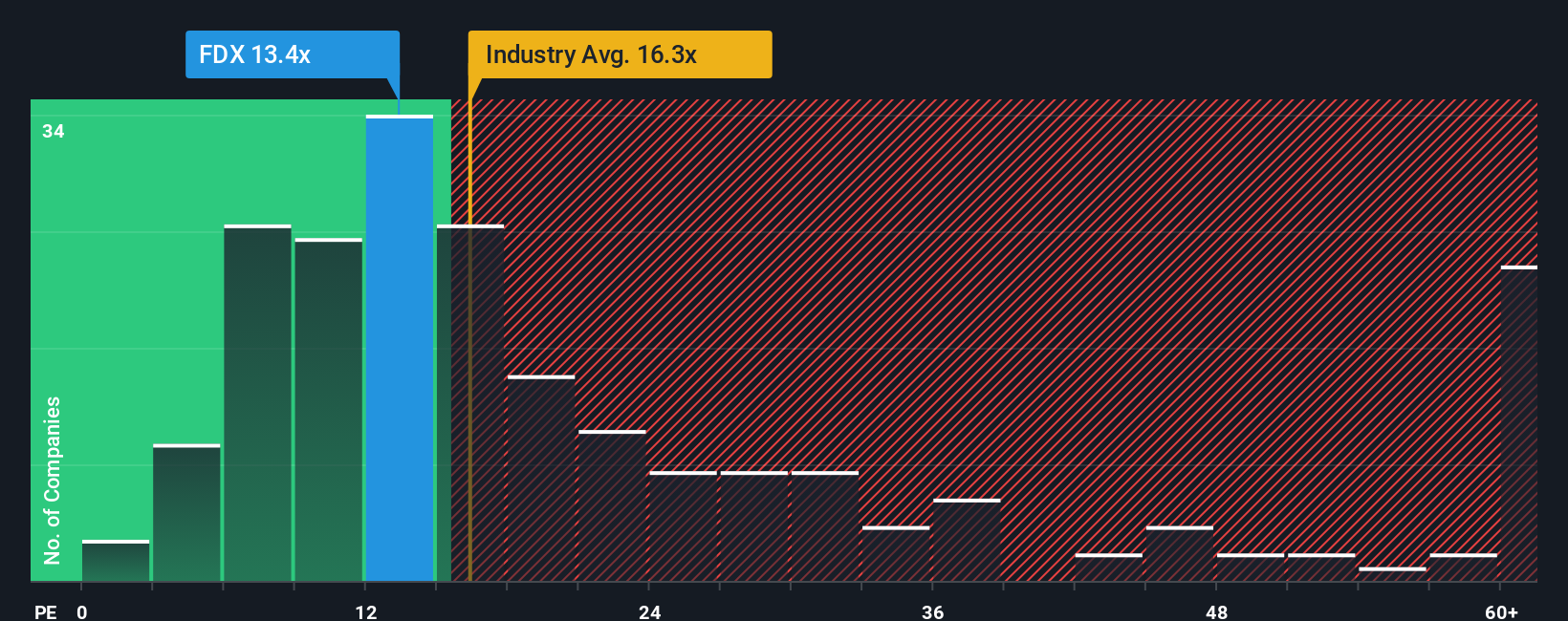

The Price-to-Earnings (PE) ratio is a classic tool for evaluating profitable companies like FedEx because it connects the company’s share price directly to its current earnings power. A lower PE can signal value if the underlying business is stable. Higher growth or lower risk often justify pricier multiples.

For FedEx, the current PE ratio stands at 13.0x. This is noticeably below both the logistics industry average of 16.2x and the peer group average of 17.8x, highlighting a valuation gap. However, what constitutes a “fair” PE multiple is not one-size-fits-all, since fast-growing or less risky companies often trade at richer valuations. To add clarity, we refer to the Fair Ratio, a custom benchmark that blends FedEx’s own growth prospects, profitability, scale, and risk profile.

FedEx’s Fair Ratio comes out at 16.8x. This suggests that based on its fundamentals, the market could reasonably assign it a higher multiple than where it trades today. Since the current PE (13.0x) is materially below the fair value benchmark, this analysis signals that the market may be undervaluing FedEx’s earnings potential right now.

Result: UNDERVALUED

Upgrade Your Decision Making: Choose your FedEx Narrative

A Narrative is your personalized story about a company, connecting the “why” behind your investment outlook to the financial numbers, such as future revenue, earnings, and margins. It then ties them all together to reach your view of fair value.

Rather than relying solely on standard ratios, Narratives let you factor in your perspectives on FedEx’s strategy, risks, and opportunities. This approach bridges the gap between headline news and financial forecasts. On Simply Wall St, Narratives are easy to create and refine. Millions of users share their perspectives and compare how different outlooks impact fair value estimates versus today’s price.

Narratives also make decision making easier by showing when your view of FedEx’s fair value is higher or lower than the current price. This information helps you decide whether it might be time to buy or sell. Best of all, Narratives update automatically as new data, earnings results, or news comes in, keeping your outlook current.

For example, one investor sees FedEx’s price target as high as $320.00, citing efficiency gains and cost-saving initiatives. Another investor, however, targets just $200.00 due to the threat of contract and economic headwinds. This is a reminder that your Narrative is dynamic and entirely your own.

Do you think there's more to the story for FedEx? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FDX

FedEx

Provides transportation, e-commerce, and business services in the United States and internationally.

Undervalued established dividend payer.

Market Insights

Advertisement

Community Narratives

Gaxos.ai: Early-Stage AI Innovator in Gaming & Health

Fair Value US$2.21|6.3% undervalued

JO

Community Contributor

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value US$500.00|0.9% overvalued

PI

Community Contributor

Amazon's Future Rises as Stock Price Falls: A Long-Term Investment Vision

Fair Value US$234.75|2.9% undervalued

ZW

Community Contributor