Advertisement

- United States

- /

- Wireless Telecom

- /

- NYSE:TDS

How Investors May Respond To Telephone and Data Systems (TDS) Struggles With Debt and Negative Free Cash Flow

Simply Wall St

Reviewed by Sasha Jovanovic

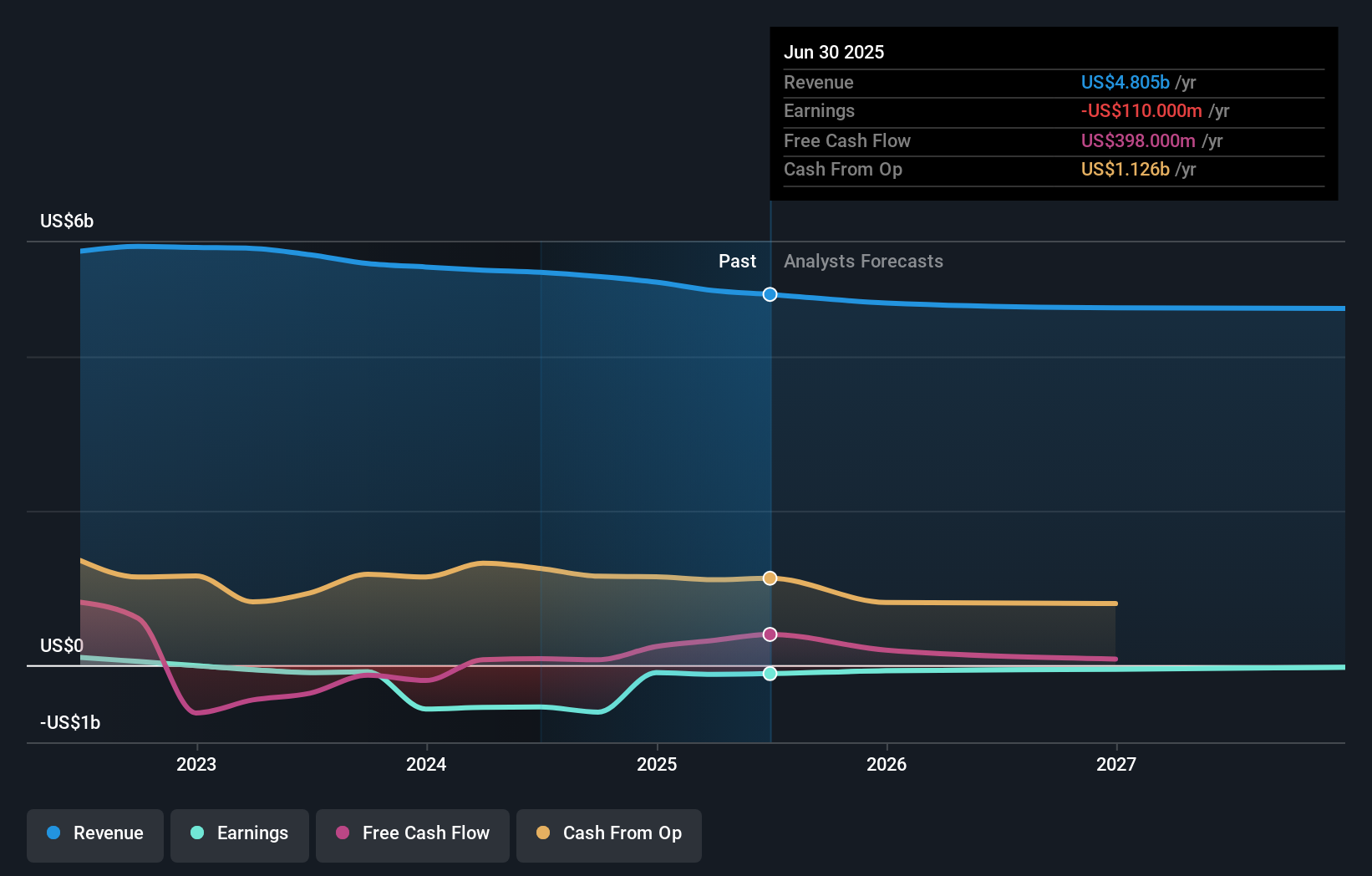

- In recent days, Telephone and Data Systems has faced continued investor concerns following news of consecutive yearly sales declines, significant debt burdens, and weak interest coverage reported up to October 2025.

- A particularly important insight is that despite some growth in earnings before interest and taxes, the company has generated substantial negative free cash flow over the last three years, amplifying the risks associated with its elevated leverage.

- We'll examine how the company's ongoing struggle with negative free cash flow and high leverage could reshape its investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Telephone and Data Systems Investment Narrative Recap

To be a shareholder in Telephone and Data Systems today, one must believe in management’s ability to transition the business beyond declining legacy revenues toward a more competitive fiber and tower-focused model, while effectively managing significant debt. The recent news of ongoing sales declines and negative free cash flow does not materially alter the biggest catalyst, the potential for fiber expansion and asset monetization, but it does highlight the immediate risk of strained financial flexibility and weak interest coverage.

Among recent company announcements, the move in August to fully pay off all indebtedness under several credit agreements stands out. While this action led to a $9 million termination penalty, it temporarily reduces financing costs and underscores management’s efforts to manage leverage, an especially relevant step as TDS navigates persistent negative cash flow and prepares for upcoming fiber investments.

In sharp contrast, investors should be aware that continued high capital expenditure for fiber, if not matched by subscriber growth and returns, could...

Read the full narrative on Telephone and Data Systems (it's free!)

Telephone and Data Systems' narrative projects $4.6 billion revenue and $577.2 million earnings by 2028. This requires a 1.7% annual revenue decline and a $687.2 million earnings increase from current earnings of -$110.0 million.

Uncover how Telephone and Data Systems' forecasts yield a $52.00 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members offered two fair value estimates for TDS, ranging widely from US$9.82 to US$52. With this broad spectrum of community views, consider how sustained negative free cash flow signals ongoing operational risk and warrants careful evaluation of the company’s forward strategy.

Explore 2 other fair value estimates on Telephone and Data Systems - why the stock might be worth as much as 36% more than the current price!

Build Your Own Telephone and Data Systems Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Telephone and Data Systems research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Telephone and Data Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Telephone and Data Systems' overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Telephone and Data Systems might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TDS

Telephone and Data Systems

A telecommunications company, provides communications services to consumer, business, and government in the United States.

Fair value with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor