- United States

- /

- Wireless Telecom

- /

- NasdaqGS:TMUS

T-Mobile (TMUS): Exploring Valuation After Landmark Southwest WiFi Deal and Launch of SuperMobile Plan

Reviewed by Simply Wall St

If you’re holding or considering T-Mobile US (TMUS), there’s a fresh development that might shape your next move. The company just inked its first-ever deal with Southwest Airlines to deliver free, unlimited WiFi to all Rapid Rewards Members on every Southwest flight. This isn’t just a one-time perk. T-Mobile is expanding its connectivity footprint, making it possible for millions of travelers to stay connected at no extra charge, regardless of their wireless provider. The timing follows the launch of T-Mobile’s new SuperMobile business plan, which combines advanced 5G, satellite coverage, and built-in security for enterprise customers.

All this arrives amid slow and steady gains for T-Mobile’s stock over the past year. TMUS is up 26% for the year and has returned over 72% in the past three years, with recent moves hinting at building momentum despite only modest rises in the past month. The company’s continued innovation, such as the Southwest WiFi partnership and enterprise advances, is keeping TMUS in the spotlight and may shift risk and growth perceptions for investors sizing up the stock’s next chapter.

So, with customer-friendly partnerships and new business offerings stacking up, is T-Mobile still trading at a discount, or are investors already paying up for its future growth?

Most Popular Narrative: 20% Overvalued

According to WallStreetWontons, the current valuation puts T-Mobile in overvalued territory when compared to its own long-term growth profile and market estimates.

Catalysts, Products or Services Impacting Sales or Earnings: T-Mobile (TMUS) has several key products and services that could significantly impact its sales and earnings: • 5G Network Expansion: T-Mobile’s aggressive rollout of its 5G network is a major growth driver. The company has been leading in 5G coverage and performance, which attracts more customers and increases service revenues.

Ready to peek behind the curtain of this premium valuation? The story centers on T-Mobile’s evolving growth assumptions, including earnings and revenue models, margin expansion, and future profit multiples. Curious why this narrative values T-Mobile like a growth powerhouse? Explore the specifics and see what numbers really fuel this conclusion.

Result: Fair Value of $201.69 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, operational hiccups from the Sprint merger or a surge in competitive pressure could quickly change how investors view T-Mobile’s current valuation.

Find out about the key risks to this T-Mobile US narrative.Another View: Discounted Cash Flow Model Tells a Different Story

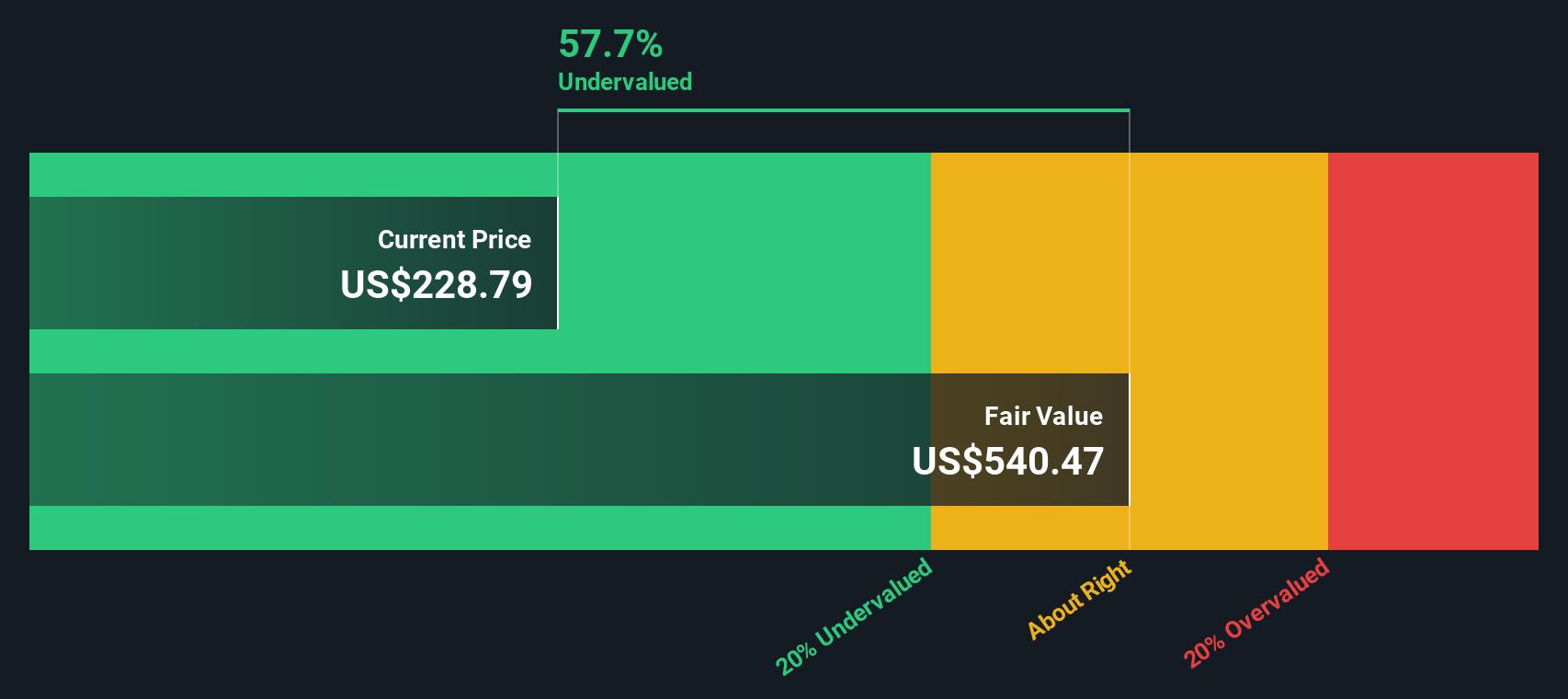

While the narrative based on growth assumptions sees T-Mobile as overvalued, our DCF model presents a contrasting analysis, suggesting the stock is trading at a meaningful discount. Which perspective better reflects reality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out T-Mobile US for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own T-Mobile US Narrative

If you’d rather draw your own conclusions or want to dig deeper into the numbers, you can craft a personalized T-Mobile outlook in just a few minutes. Do it your way.

A great starting point for your T-Mobile US research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Opportunities?

Unlock your edge and don't miss a chance to uncover stocks that match your ambitions. Use Simply Wall Street’s screeners to target opportunities you won’t find anywhere else.

- Capture consistent returns with income powerhouses yielding above 3% by checking out dividend stocks with yields > 3% built for yield-seekers.

- Tap into tomorrow’s breakthroughs in medicine and patient care through healthcare AI stocks designed for the future of healthcare innovation.

- Seize underappreciated gems with high upside by navigating undervalued stocks based on cash flows, perfect for bargain hunters who won’t settle for average.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if T-Mobile US might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:TMUS

T-Mobile US

Provides wireless communications services in the United States, Puerto Rico, and the United States Virgin Islands.

Good value with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)