Advertisement

- United States

- /

- Telecom Services and Carriers

- /

- NasdaqCM:SIFY

Here's What's Concerning About Sify Technologies' (NASDAQ:SIFY) Returns On Capital

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Having said that, from a first glance at Sify Technologies (NASDAQ:SIFY) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Sify Technologies is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

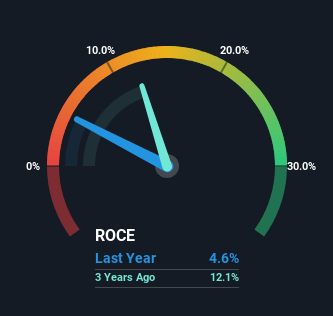

0.046 = ₹2.2b ÷ (₹71b - ₹23b) (Based on the trailing twelve months to March 2024).

Therefore, Sify Technologies has an ROCE of 4.6%. In absolute terms, that's a low return but it's around the Telecom industry average of 5.6%.

View our latest analysis for Sify Technologies

In the above chart we have measured Sify Technologies' prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for Sify Technologies .

The Trend Of ROCE

The trend of ROCE doesn't look fantastic because it's fallen from 11% five years ago, while the business's capital employed increased by 207%. However, some of the increase in capital employed could be attributed to the recent capital raising that's been completed prior to their latest reporting period, so keep that in mind when looking at the ROCE decrease. Sify Technologies probably hasn't received a full year of earnings yet from the new funds it raised, so these figures should be taken with a grain of salt.

On a side note, Sify Technologies has done well to pay down its current liabilities to 33% of total assets. So we could link some of this to the decrease in ROCE. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.

What We Can Learn From Sify Technologies' ROCE

In summary, Sify Technologies is reinvesting funds back into the business for growth but unfortunately it looks like sales haven't increased much just yet. Unsurprisingly, the stock has only gained 9.9% over the last five years, which potentially indicates that investors are accounting for this going forward. So if you're looking for a multi-bagger, the underlying trends indicate you may have better chances elsewhere.

One more thing: We've identified 2 warning signs with Sify Technologies (at least 1 which is significant) , and understanding these would certainly be useful.

While Sify Technologies may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:SIFY

Sify Technologies

Offers information and communication technology solutions and services in India and internationally.

High growth potential and overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2540.2% undervalued

91 followersusers have followed this narrative

0 commentsusers have commented on this narrative

22 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$481.8% overvalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5453.8% undervalued

57 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$827.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

WE

WealthAP on Alphabet ·

The "Easy Money" Is Gone: Why Alphabet Is Now a "Show Me" Story

Fair Value:US$386.435.2% undervalued

71 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

KE

Kentaiga on Microsoft ·

Microsoft Are Industry Leaders at a Heavy Discount

Fair Value:US$50022.7% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.529.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.9% undervalued

83 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5453.8% undervalued

57 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

MW

mwod31 on Greatland Resources ·

A great comment, WSB have not done the research imo. I intend to buy more shares in 2026.

0

|0