Vishay Intertechnology (VSH): Valuation Insights After Launching High-Reliability Capacitor for EV and Clean Energy Markets

Reviewed by Simply Wall St

Most Popular Narrative: 11% Overvalued

According to the most widely followed narrative, Vishay Intertechnology is currently considered overvalued by analysts, with the stock trading at a premium relative to their calculated fair value. The narrative brings together future earnings expectations, margin improvements, and sector trends to form this outlook.

"With major multi-year investments in capacity expansion nearing completion, including readiness across nearly all product lines and the ramp of high-growth, higher-profit products, Vishay is well positioned to capture share as demand accelerates in areas like AI, smart grid infrastructure, data centers, and automotive electrification. This supports higher future revenues and improved operating leverage."

Want to know the growth formula behind this bold analyst call? The narrative hints at a dramatic shift powered by profit margin jumps and ambitious revenue targets. Find out what game-changing projections and strategic pivots set the scene for this premium price tag.

Result: Fair Value of $14 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent cash flow strain and reliance on legacy products could derail projections, particularly if profitability challenges or technology shifts occur.

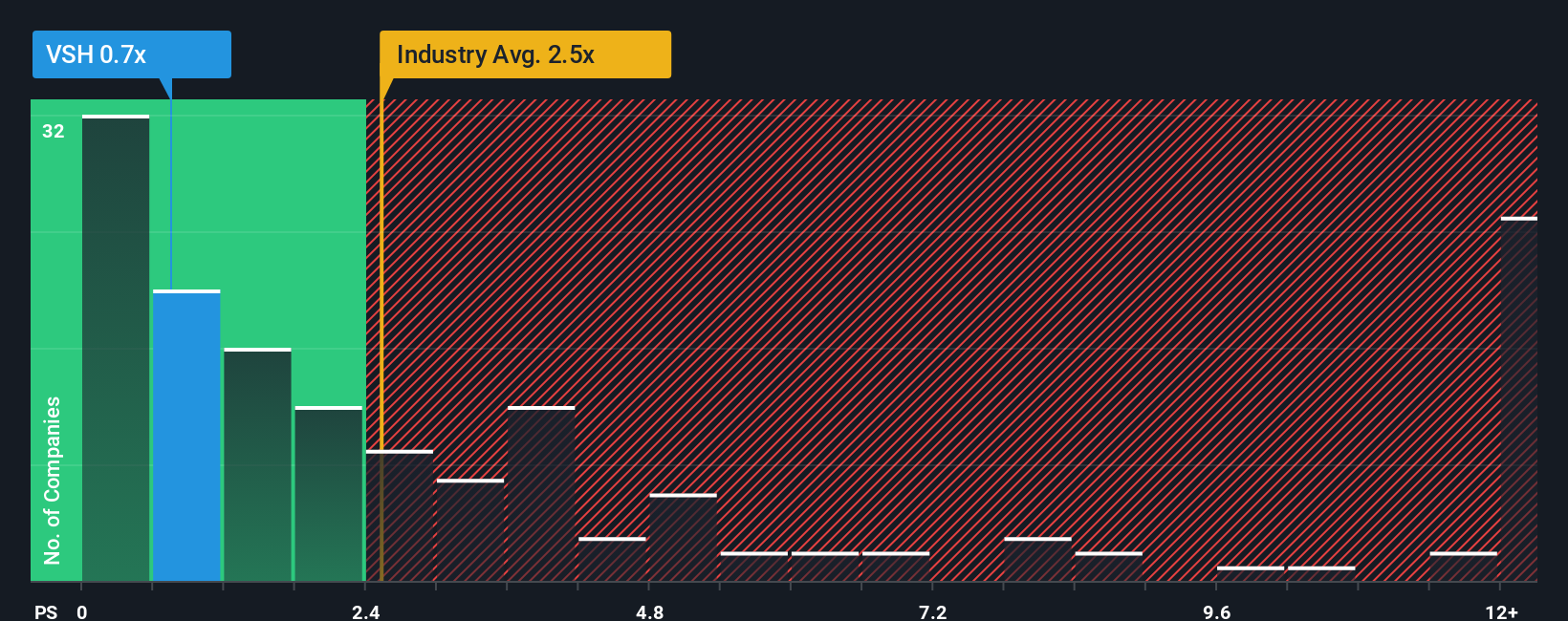

Find out about the key risks to this Vishay Intertechnology narrative.Another View: Market Ratios Tell a Different Story

Looking at Vishay Intertechnology through market ratios shows the stock trading at significantly lower levels than the rest of the industry. This suggests some investors see more value than headline analyst targets imply. Could the market be missing a turnaround, or are the risks more significant than they seem?

See what the numbers say about this price — find out in our valuation breakdown.

Stay updated when valuation signals shift by adding Vishay Intertechnology to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own Vishay Intertechnology Narrative

If you have a different perspective or want to take a hands-on approach with the numbers and story behind VSH, you can shape your own view in just a few minutes. Do it your way.

A great starting point for your Vishay Intertechnology research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don't let opportunity pass you by. Take your investing to the next level using tools designed to surface tomorrow’s leaders, undervalued gems, and big dividend payers before everyone else spots them.

- Spot tomorrow’s success stories by searching for penny stocks with strong financials with strong numbers and resilient performance.

- Access companies shaking up medicine and innovation through our handpicked list of healthcare AI stocks changing healthcare with artificial intelligence.

- Zero in on investment bargains and maximize potential returns by reviewing stocks that are undervalued stocks based on cash flows and still flying under the radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NYSE:VSH

Vishay Intertechnology

Manufactures and sells discrete semiconductors and passive electronic components in the United States, Germany, rest of Europe, Israel, and Asia.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)