- United States

- /

- Tech Hardware

- /

- NYSE:PSTG

Pure Storage (PSTG) Raises Revenue Guidance and Completes US$390 Million Share Buyback

Reviewed by Simply Wall St

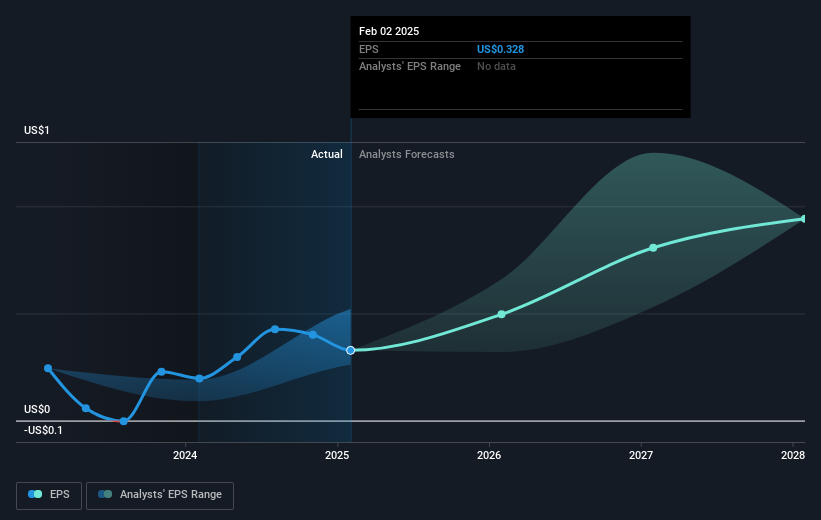

Pure Storage (PSTG) experienced a price increase of 14% over the last quarter, potentially influenced by several key developments. The company's recent financial guidance, which raised fiscal year revenue expectations and reported strong second-quarter results, showcased its resilient performance. The revision of FY2026 guidance and announcements of innovative products in storage management may have further bolstered market sentiment. Despite these developments, it's important to note that the broader market also saw gains with major indexes, such as the S&P 500 and Nasdaq, setting record highs, suggesting that Pure Storage's stock performance could have aligned with overall market trends.

We've discovered 1 weakness for Pure Storage that you should be aware of before investing here.

Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

The recent developments at Pure Storage, including revised fiscal guidance and innovative product announcements, could positively influence the company’s market penetration and operational scale, as suggested in the narrative. The design win with a top hyperscaler presents a significant opportunity to escalate deployment and revenue potential, especially with the anticipated tenfold rise in AI-driven data demand. Over the past five years, Pure Storage's total shareholder return, including share price gains and dividends, was 304.65%. This historical performance reflects robust shareholder value creation, offering important context for the recent share price movement in the last quarter.

When comparing the company’s recent performance to the industry, Pure Storage outperformed the US Tech industry, which returned 2.4% over the past year. This strength could be attributed to both the broader market's rally and the company's strategic actions. However, challenges such as geopolitical risks and slower deal closures could pressure the margins and revenue growth in future forecasts. The current share price of US$60.86 remains below the consensus price target of US$70.61, suggesting potential upside if the market aligns with analysts’ expectations of improved earnings and revenue growth driven by the company’s aggressive expansion into AI-related storage solutions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PSTG

Pure Storage

Provides data storage and management technologies, products, and services in the United States and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)