- United States

- /

- Tech Hardware

- /

- NYSE:HPE

Will Nokia Partnership and RAN Automation Push Transform Hewlett Packard Enterprise’s (HPE) AI Growth Narrative?

Reviewed by Sasha Jovanovic

- On October 2, 2025, Nokia announced it had entered a global licensing agreement with Hewlett Packard Enterprise (HPE) to integrate HPE's RAN Intelligent Controller with Nokia's MantaRay SMO platform, deepening their collaboration in AI-driven radio access network automation; the agreement also saw the transfer of the associated HPE development team to Nokia Mobile Networks.

- This deal positions HPE as a key technology provider to leading telecom players and underscores its growing presence in AI-powered network automation.

- We'll examine how HPE's expanded technology role in AI-driven telecom automation impacts its long-term growth narrative and competitive positioning.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Hewlett Packard Enterprise Investment Narrative Recap

To be a shareholder in Hewlett Packard Enterprise, you need confidence in its ability to expand in AI-driven networking and high-performance infrastructure, particularly as it integrates acquisitions like Juniper. The recent licensing deal with Nokia reinforces HPE's technology leadership but does not materially alter the core short-term catalyst: successful Juniper integration remains the biggest driver, while execution risk on that front continues to be the main uncertainty for near-term performance.

Among recent announcements, the launch of new Juniper Networking capabilities in August is most relevant to the Nokia agreement, as both highlight HPE’s push into autonomous, AI-centric network solutions. These moves broaden HPE’s reach in enterprise and telecom, aiming to capture share in higher-value software and services while providing crucial proof points for its margin expansion ambitions.

Yet, investors should also keep in mind that, while HPE is gaining momentum in next-generation network automation, the risk around integrating its major Juniper deal is far from resolved...

Read the full narrative on Hewlett Packard Enterprise (it's free!)

Hewlett Packard Enterprise's outlook anticipates $44.4 billion in revenue and $2.7 billion in earnings by 2028. This is based on revenue growing at 10.3% per year and a $1.6 billion increase in earnings from the current $1.1 billion.

Uncover how Hewlett Packard Enterprise's forecasts yield a $25.82 fair value, a 5% upside to its current price.

Exploring Other Perspectives

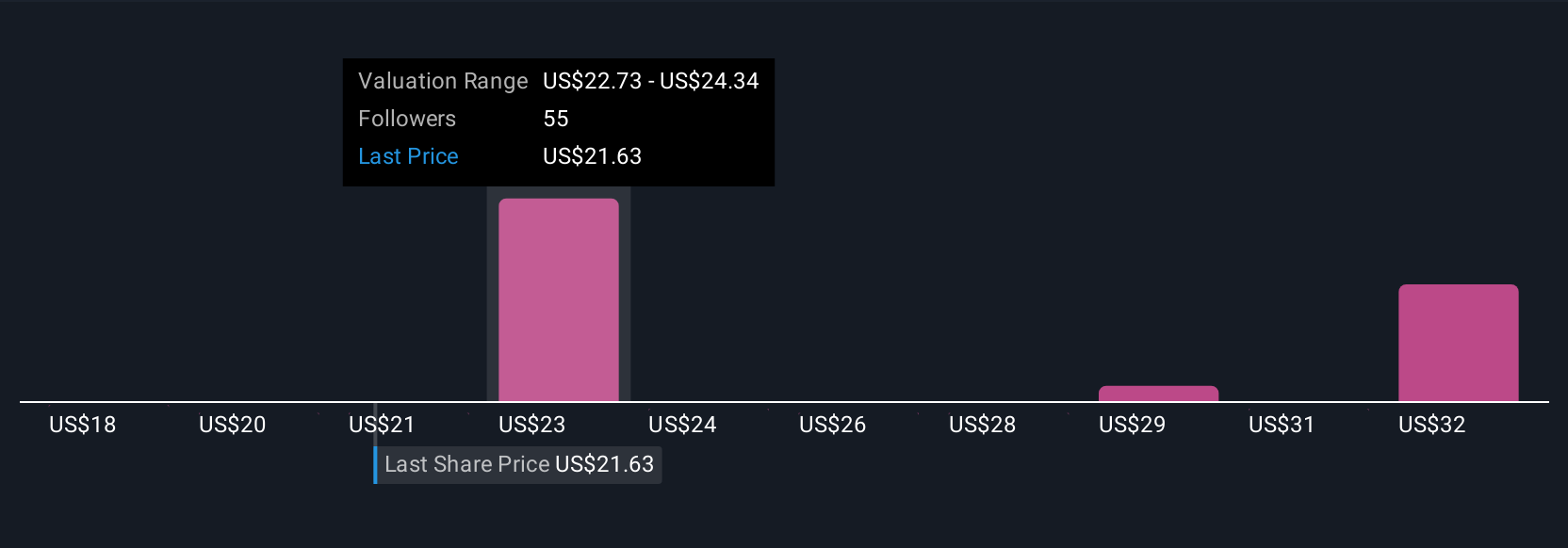

Seven private investors from the Simply Wall St Community estimate HPE’s fair value between US$17.90 and US$48.08, with several seeing a significant discount to market price. As these outlooks diverge sharply, be mindful that integration execution risk could weigh heavily on future earnings and your own assessment of HPE’s potential.

Explore 7 other fair value estimates on Hewlett Packard Enterprise - why the stock might be worth 27% less than the current price!

Build Your Own Hewlett Packard Enterprise Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Hewlett Packard Enterprise research is our analysis highlighting 2 key rewards and 5 important warning signs that could impact your investment decision.

- Our free Hewlett Packard Enterprise research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hewlett Packard Enterprise's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 33 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hewlett Packard Enterprise might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HPE

Hewlett Packard Enterprise

Provides solutions that allow customers to capture, analyze, and act upon data seamlessly.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)