Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:WDC

Will Analyst Momentum and AI Demand Sustain Western Digital’s (WDC) Long-Term Edge in Data Storage?

Simply Wall St

Reviewed by Sasha Jovanovic

- Western Digital Corporation recently presented at the 17th Annual Silicon Valley C-Level Technology Leadership Summit, with Chief Information Officer Sesh Tirumala sharing updates at the Hyatt Centric Mountain View in California on October 7, 2025.

- The company's momentum is fueled by robust institutional sentiment, analyst upgrades, and surging demand for high-capacity data storage driven by expanding AI and cloud adoption.

- We'll explore how Western Digital's record-setting storage shipments and strong analyst sentiment affect its long-term growth narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Western Digital Investment Narrative Recap

To own Western Digital, you need to believe in sustained demand for large-scale data storage powered by AI and cloud applications, with strong partnerships among major hyperscale customers. The recent leadership summit presentation underscores the company’s focus on innovation and data center expansion, but the event itself does not materially change the top short-term catalyst: accelerating shipments of high-capacity HDD and UltraSMR drives. The biggest risk remains Western Digital’s heavy customer concentration, as losing even one major hyperscaler could have a significant impact.

Among recent announcements, the completion of a 2.8 million share buyback for US$151.12 million stands out. This action signals management’s confidence in the company’s long-term prospects while reinforcing Western Digital’s commitment to returning capital to shareholders, a relevant point for investors watching near-term catalysts like new product launches and margin expansion in cloud storage.

However, despite robust growth drivers, investors should carefully consider the concentration risk tied to hyperscale customer relationships...

Read the full narrative on Western Digital (it's free!)

Western Digital is projected to reach $11.9 billion in revenue and $2.2 billion in earnings by 2028. This outlook reflects an expected annual revenue growth rate of 7.6% and a $0.6 billion increase in earnings from the current $1.6 billion level.

Uncover how Western Digital's forecasts yield a $103.59 fair value, a 10% downside to its current price.

Exploring Other Perspectives

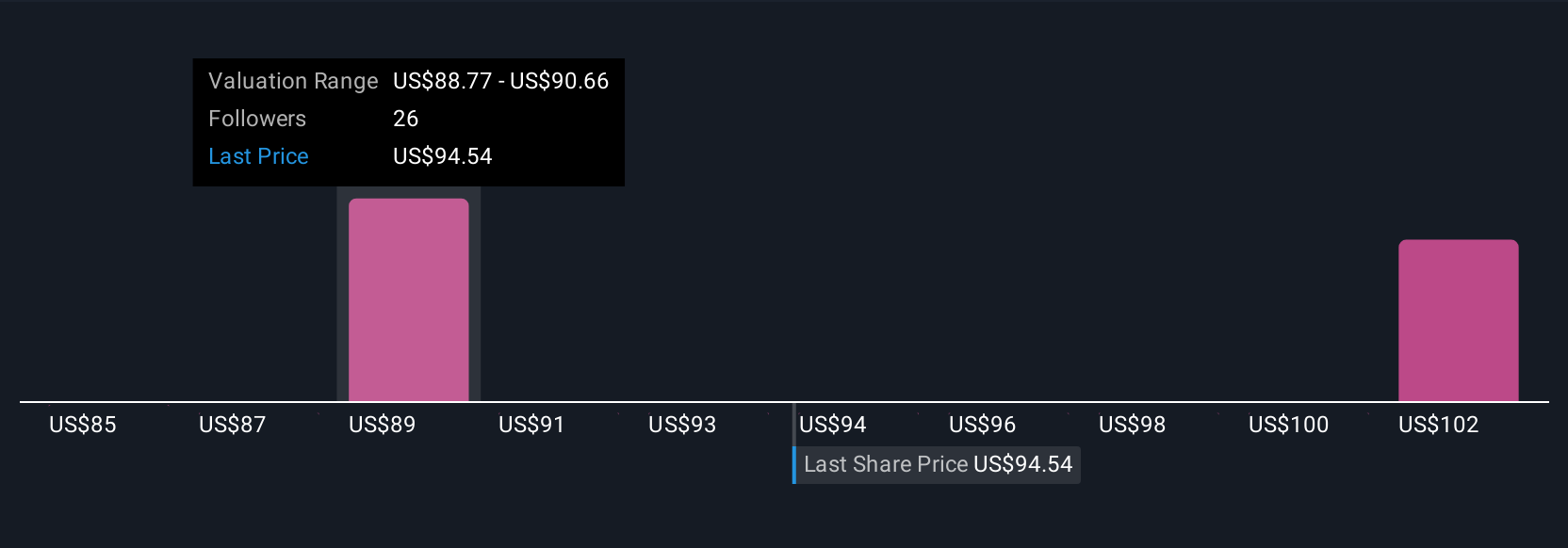

Four members of the Simply Wall St Community placed their fair value estimates for Western Digital between US$85 and US$108.94 per share. While opinions span over a US$20 range, the company’s deep integration with hyperscale customers shapes expectations for both growth potential and concentration risk, review how these competing views might change your outlook.

Explore 4 other fair value estimates on Western Digital - why the stock might be worth as much as $108.94!

Build Your Own Western Digital Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Western Digital research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Western Digital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Western Digital's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Western Digital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WDC

Western Digital

Develops, manufactures, and sells data storage devices and solutions based on hard disk drive (HDD) technology in the United States, Asia, Europe, the Middle East, and Africa.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor