Advertisement

- United States

- /

- Software

- /

- NasdaqGS:TRMB

Trimble (TRMB): Evaluating Valuation After a Steady Year-to-Date Share Price Climb

Trimble (TRMB) has been quietly grinding higher this year, and that alone is enough to get investors asking whether the current price still leaves meaningful upside or if expectations are finally catching up.

See our latest analysis for Trimble.

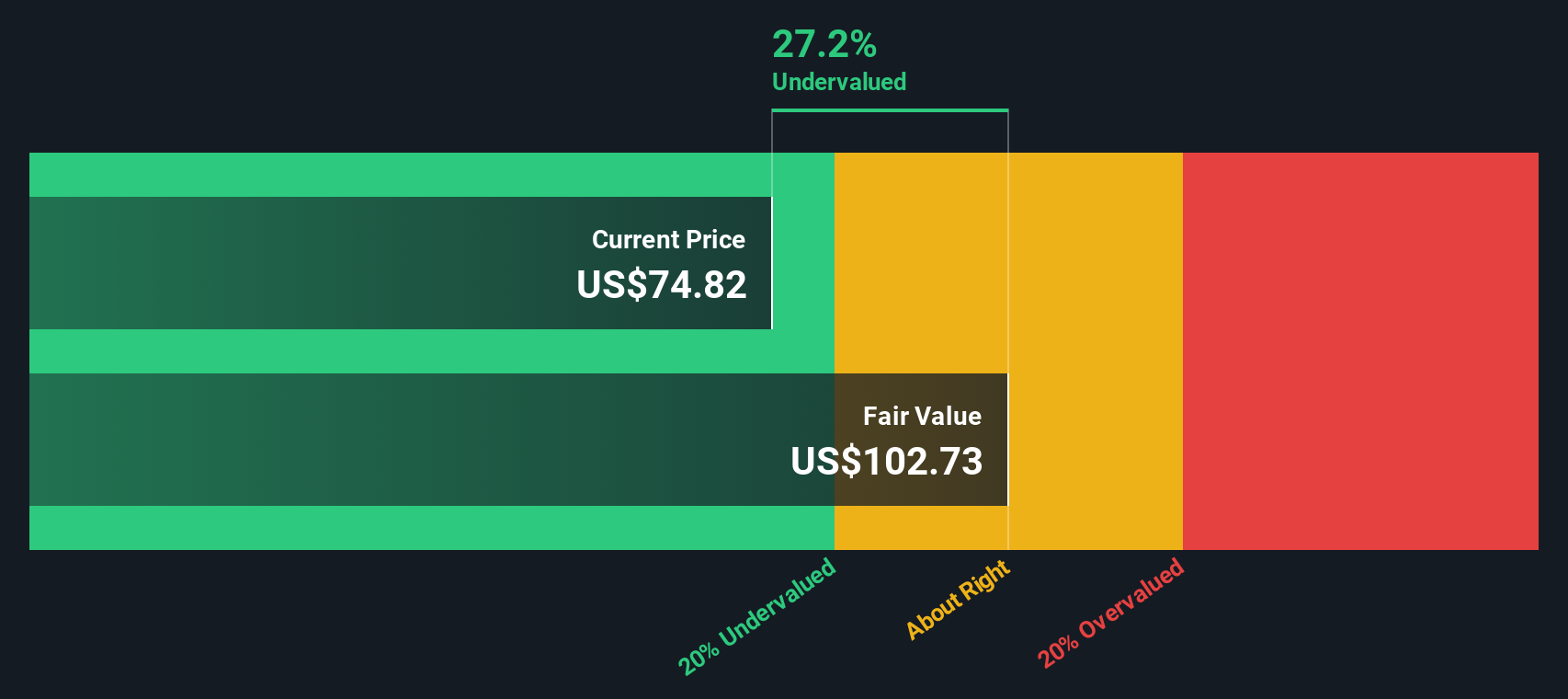

Recent gains have been steady rather than flashy, with the share price at $82.46 and an 18.29 percent year to date share price return echoing Trimble’s improving growth story. This is supported by a solid three year total shareholder return of 58.97 percent.

If Trimble’s trajectory has you thinking about what else might be quietly compounding in tech, this could be a good moment to explore high growth tech and AI stocks for more ideas.

With revenue and earnings both advancing and the share price still sitting at a near 19 percent discount to analyst targets, the key question now is simple: is Trimble a buy or is future growth already priced in?

Most Popular Narrative: 16.2% Undervalued

With Trimble’s fair value pegged near $98.45 against a recent close of $82.46, the most followed narrative points to a meaningful valuation gap.

The migration from hardware-focused, CapEx models to bundled, subscription-based offerings even in traditionally hardware-oriented segments expands the addressable market, improves revenue visibility, and increases recurring revenue mix, driving greater predictability and enhanced long-term earnings.

Want to see the engine behind that valuation gap? The narrative leans on rising recurring revenue, sharply higher margins, and a bold earnings power reset. Curious?

Result: Fair Value of $98.45 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, extended weakness in government spending and faster moving, AI driven competitors could easily derail Trimble’s margin expansion and recurring revenue ambitions.

Find out about the key risks to this Trimble narrative.

Another Lens on Value

Our SWS DCF model paints an even stronger case than the narrative based fair value. On that view, Trimble at $82.46 screens as about 19 percent undervalued versus an intrinsic value near $102.10. If cash flows line up with forecasts, is the market giving you a margin of safety or signaling hidden risks?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Trimble Narrative

If you see the story differently or want to dig into the numbers yourself, you can quickly craft a custom view in under three minutes: Do it your way.

A great starting point for your Trimble research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, consider scanning targeted stock ideas that could sharpen your next investing move.

- Explore potential multi-baggers early by reviewing these 3599 penny stocks with strong financials that already show strong balance sheets and resilient cash flows.

- Focus on these 26 AI penny stocks positioned at the intersection of innovation, scalability, and accelerating demand.

- Identify value-focused opportunities by screening these 906 undervalued stocks based on cash flows where current prices still trail long term cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Trimble might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TRMB

Trimble

Offers technology solutions and platform that enable office professionals and field workers to connect workflows and industry lifecycles in North America, Europe, the Asia Pacific, and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

133 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on MasTec ·

MasTec Inc. (MTZ): The Infrastructure Super-Cycle and the $19 Billion Backlog Milestone

Fair Value:US$33613.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SA

Sax on Super Retail Group ·

Fair Value Intriguingly Set at $11.54 for SUL Investors

Fair Value:AU$13.431.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Dell Technologies ·

Dell Technologies (DELL): The AI Infrastructure Super-Cycle and the $50 Billion Server Milestone

Fair Value:US$193.521.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1308 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0