- United States

- /

- Tech Hardware

- /

- NasdaqGS:STX

Has Seagate’s 233% Surge in 2025 Pushed Its Valuation Too Far?

Reviewed by Bailey Pemberton

- Wondering if Seagate Technology Holdings is still a smart buy after its massive run, or if you would be catching the stock at the top? This breakdown is designed to cut through the noise and focus on what the current price really implies.

- The stock has surged, climbing 3.2% over the last week, 9.6% over the last month and an eye catching 233.0% year to date. This has dramatically reshaped both its growth narrative and perceived risk profile.

- Investors have been reacting to a wave of optimism around data storage demand and AI driven infrastructure spending, as Seagate is seen as a key player in supplying high capacity drives for hyperscale data centers. At the same time, headlines around the broader tech rally and renewed interest in hardware enablers of AI have helped pull more attention and capital toward the stock.

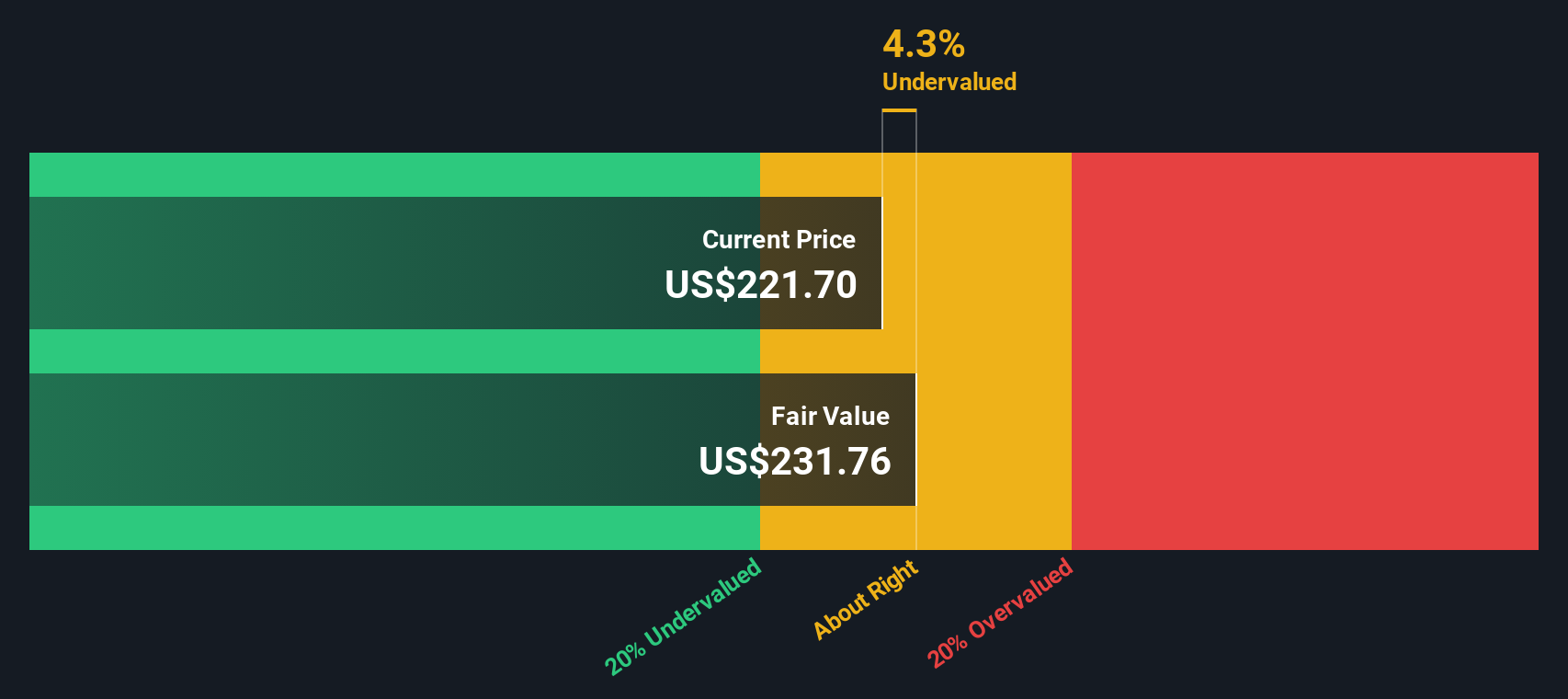

- Despite this impressive momentum, Seagate only scores a 1 out of 6 on our undervaluation checks, which might surprise anyone expecting a slam dunk value story. Next, we will walk through different valuation approaches, then wrap up with a more holistic way to think about what Seagate is truly worth beyond the usual models.

Seagate Technology Holdings scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Seagate Technology Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to today. For Seagate Technology Holdings, the model used is a 2 stage Free Cash Flow to Equity approach, based on cash flow projections in $.

Seagate is currently generating roughly $1.19 billion in free cash flow, and analyst forecasts combined with Simply Wall St extrapolations point to this rising steadily over time. By 2030, free cash flow is projected to reach about $3.85 billion, with further gradual increases assumed beyond that as growth moderates.

When all these future cash flows are discounted back to their present value, the DCF model suggests an intrinsic value of around $358.27 per share. Compared to the current share price, this implies Seagate is trading at a 19.7% discount to its estimated fair value. This indicates the market may still be underpricing its long term cash generation potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Seagate Technology Holdings is undervalued by 19.7%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

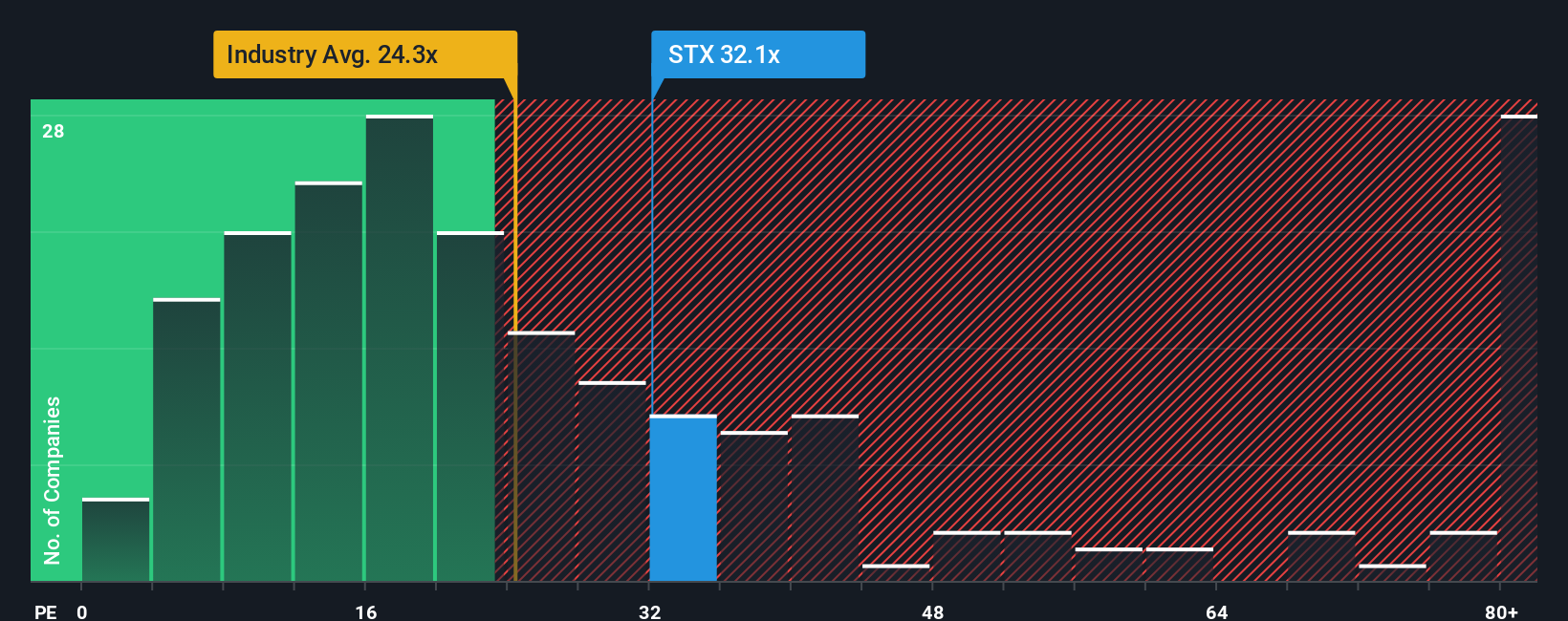

Approach 2: Seagate Technology Holdings Price vs Earnings

For a profitable business like Seagate, the price to earnings (PE) ratio is a useful yardstick because it links what investors are paying directly to the company’s current earnings power. In general, faster growth and lower perceived risk justify a higher PE, while slower growth or greater uncertainty should translate into a lower, more conservative multiple.

Seagate currently trades on a PE of about 36.6x, which is well above both the broader Tech industry average of roughly 22.7x and the peer group average of around 17.0x. At first glance, that premium suggests the market is baking in strong growth and a robust AI driven demand cycle for storage, as well as confidence that earnings will hold up through industry swings.

Simply Wall St’s proprietary Fair Ratio for Seagate is 36.3x. This metric estimates the multiple the stock should command once you factor in its specific earnings growth outlook, margins, risk profile, industry positioning and market cap. This makes it more tailored than simple peer or industry comparisons. With the current PE sitting very close to this Fair Ratio, the stock looks reasonably priced on an earnings basis rather than meaningfully stretched or cheap.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1444 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Seagate Technology Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple tool on Simply Wall St’s Community page that lets you turn your view of Seagate into a story backed by numbers. It does this by linking what you believe about its AI storage opportunity, competition and risks to a concrete forecast for revenue, earnings and margins. It then converts that forecast into a Fair Value you can compare with today’s Price to consider whether to buy, hold or sell. The platform keeps your Narrative dynamically updated as new news or earnings arrive. For example, one investor might build a bullish Seagate Narrative that assumes earnings reach $2.5 billion by 2028 and justifies a Fair Value near the top of analyst targets at about $200. A more cautious investor, worried about supply catching up and AI demand normalizing, could set more modest growth and margin assumptions that point to a Fair Value closer to the low end near $80. Both perspectives are made explicit, comparable and actionable.

Do you think there's more to the story for Seagate Technology Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:STX

Seagate Technology Holdings

Engages in the provision of data storage technology and infrastructure solutions in Singapore, the United States, the Netherlands, and internationally.

Reasonable growth potential with proven track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)