Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:SMCI

Super Micro Computer, Inc. (NASDAQ:SMCI) Looks Just Right With A 28% Price Jump

Super Micro Computer, Inc. (NASDAQ:SMCI) shares have continued their recent momentum with a 28% gain in the last month alone. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 39% in the last twelve months.

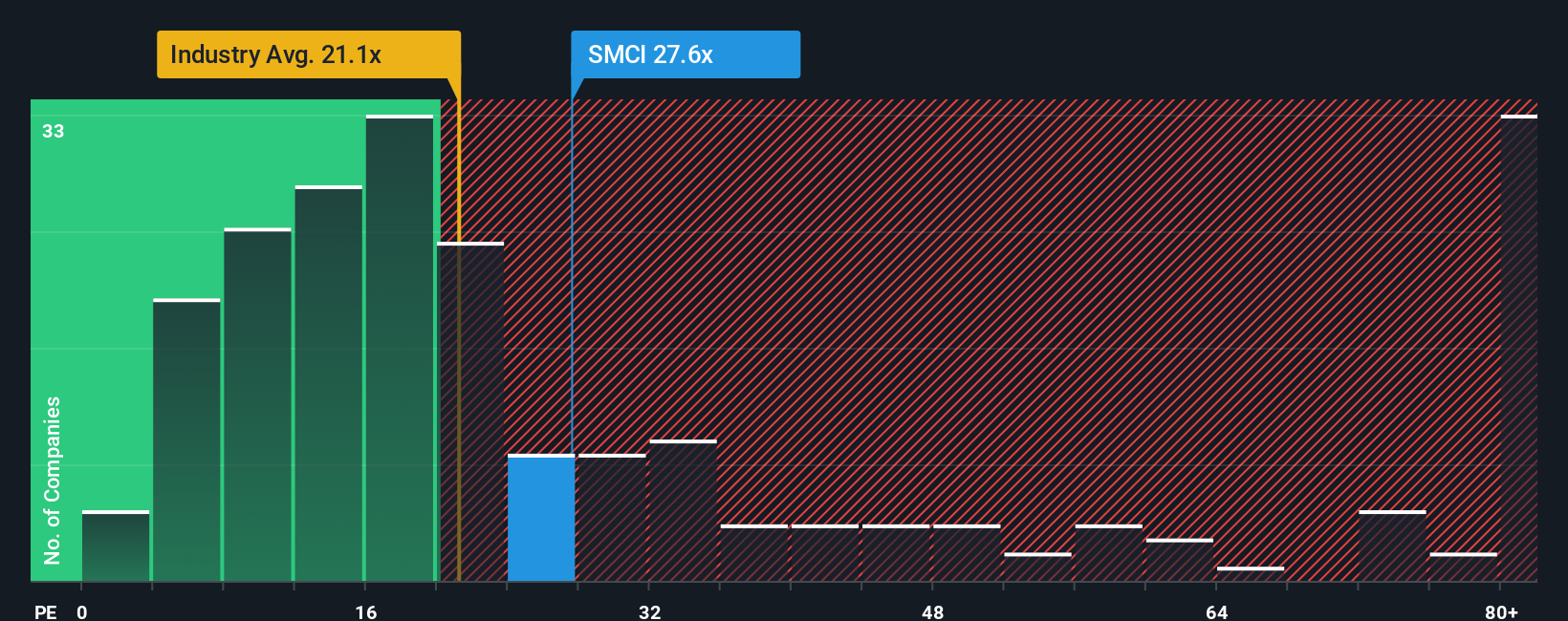

Following the firm bounce in price, Super Micro Computer may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 27.6x, since almost half of all companies in the United States have P/E ratios under 18x and even P/E's lower than 11x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Super Micro Computer could be doing better as it's been growing earnings less than most other companies lately. It might be that many expect the uninspiring earnings performance to recover significantly, which has kept the P/E from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

See our latest analysis for Super Micro Computer

Is There Enough Growth For Super Micro Computer?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Super Micro Computer's to be considered reasonable.

If we review the last year of earnings, the company posted a result that saw barely any deviation from a year ago. However, a few strong years before that means that it was still able to grow EPS by an impressive 436% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 17% over the next year. That's shaping up to be materially higher than the 13% growth forecast for the broader market.

With this information, we can see why Super Micro Computer is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Super Micro Computer's P/E

Shares in Super Micro Computer have built up some good momentum lately, which has really inflated its P/E. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Super Micro Computer's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

It is also worth noting that we have found 4 warning signs for Super Micro Computer (1 is potentially serious!) that you need to take into consideration.

If these risks are making you reconsider your opinion on Super Micro Computer, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SMCI

Super Micro Computer

Develops and sells server and storage solutions based on modular and open-standard architecture in the United States, Asia, Europe, and internationally.

Exceptional growth potential and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1158.7% undervalued

32 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.6% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9220.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$1908.3% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

RE

Reex on Unibap Space Solutions ·

Long-term bet on Europe's strategic space autonomy (2030–2055)

Fair Value:SEK 36.0176.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AV

Averagemike on Samsara ·

Samsara's Future PE Will Soar to 337.7x and the Future is Bright

Fair Value:US$57.34k99.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on ServiceNow ·

The Company Nobody Brags About

Fair Value:US$266.0164.1% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

103 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5449.5% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual income — with every assumption published and tagged as fact or assumption. The interesting result isn't a number, it's a disagreement: the point estimates run from €20,03 (RIM) through €27,64 (DDM) to €64,91 (DCF), and the pairwise overlaps form two disjoint segments — €20,36–€21,54 and €39,60–€44,56. Between €21,54 and €39,60, no two of the three models agree. [img]https://staticm.fastcomments.com/1784197249786-1000x1000-ad-range-strip.png[/img] Most of the spread is lens properties rather than company drama. A dividend model structurally can't see the roughly half of shareholder returns Ahold pays through buybacks. The book is ~96 % goodwill from the 2016 merger, which pins the residual-income reading low. And ~83 % of the DCF's value sits beyond the explicit five years, so it leans hard on the terminal assumptions. Three honest lenses, three honest answers — the disagreement is the information. Disclosures Position disclosure: The author holds no position in Ahold Delhaize as at 9 July 2026. This valuation is a StoxEurope opinion, based on honest research. Mistakes are possible. This is not investment advice. Do your own research. This article demonstrates a valuation methodology. It is not an investment recommendation, is not personalised to any reader's circumstances, and every figure in it depends entirely on the stated assumptions

1

|0

ST

stephen_iwu3c on CK Hutchison Holdings ·

Hutchsion 3 UK has been sold to vodafone, why is there an integration costs, is the analysis outdated?

0

|0