Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:SCSC

We Think ScanSource (NASDAQ:SCSC) Is Taking Some Risk With Its Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that ScanSource, Inc. (NASDAQ:SCSC) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for ScanSource

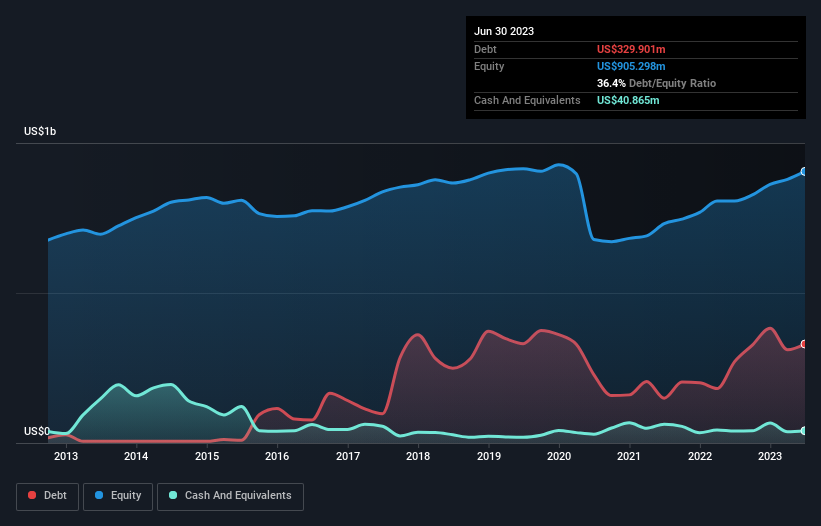

What Is ScanSource's Debt?

The image below, which you can click on for greater detail, shows that at June 2023 ScanSource had debt of US$329.9m, up from US$271.2m in one year. However, it also had US$40.9m in cash, and so its net debt is US$289.0m.

A Look At ScanSource's Liabilities

The latest balance sheet data shows that ScanSource had liabilities of US$786.8m due within a year, and liabilities of US$376.1m falling due after that. On the other hand, it had cash of US$40.9m and US$833.3m worth of receivables due within a year. So its liabilities total US$288.7m more than the combination of its cash and short-term receivables.

ScanSource has a market capitalization of US$792.3m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

ScanSource's net debt to EBITDA ratio of about 1.7 suggests only moderate use of debt. And its strong interest cover of 11.1 times, makes us even more comfortable. One way ScanSource could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 12%, as it did over the last year. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine ScanSource's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, ScanSource recorded negative free cash flow, in total. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

Neither ScanSource's ability to convert EBIT to free cash flow nor its level of total liabilities gave us confidence in its ability to take on more debt. But its interest cover tells a very different story, and suggests some resilience. Looking at all the angles mentioned above, it does seem to us that ScanSource is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. Over time, share prices tend to follow earnings per share, so if you're interested in ScanSource, you may well want to click here to check an interactive graph of its earnings per share history.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SCSC

ScanSource

Engages in the distribution of technology products and solutions in the United States and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4347.9% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

23 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.2k% overvalued

31 followersusers have followed this narrative

7 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AH

AHaron on Eli Lilly ·

Eli Lilly: A Pipeline-Driven Growth Story Trading 30% Below What the Business Is Actually Worth

Fair Value:US$1.48k35.4% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

IN

InvestingNurse on Lucid Diagnostics ·

Poised for success

Fair Value:US$577.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LO

Lou_Basenese on Gain Therapeutics ·

The Market Is Sleeping on This Parkinson's Biotech - And I Think That's a Mistake

Fair Value:US$7.674.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

OS

osborne820 on Grid Metals ·

Grid Metals will see a transformative 21.5x future PE change

Fair Value:CA$0.7584.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9832.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6436.5% undervalued

40 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.2k% overvalued

31 followersusers have followed this narrative

7 commentsusers have commented on this narrative

24 likesusers have liked this narrative