Advertisement

- United States

- /

- Communications

- /

- NasdaqGS:NTGR

NETGEAR, Inc. (NASDAQ:NTGR) Analysts Are Way More Bearish Than They Used To Be

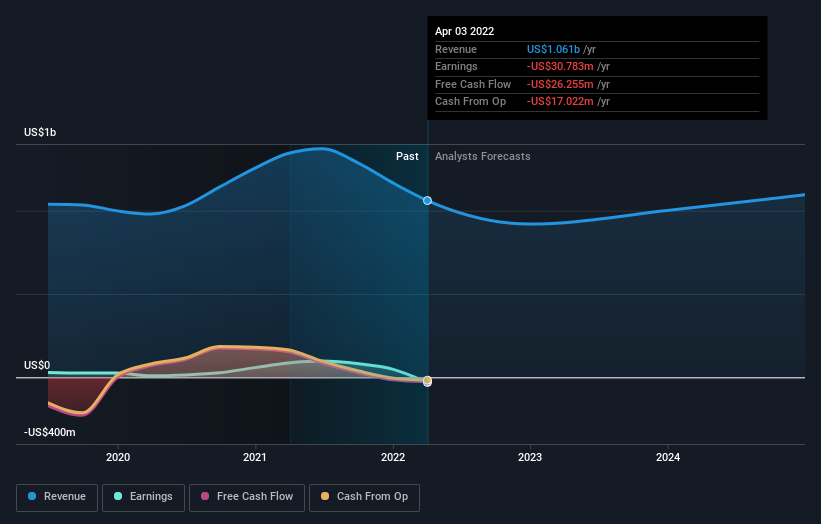

The latest analyst coverage could presage a bad day for NETGEAR, Inc. (NASDAQ:NTGR), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Both revenue and earnings per share (EPS) estimates were cut sharply as the analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

Following the latest downgrade, the four analysts covering NETGEAR provided consensus estimates of US$920m revenue in 2022, which would reflect a not inconsiderable 13% decline on its sales over the past 12 months. Losses are supposed to balloon 78% to US$1.88 per share. Prior to this update, the analysts had been forecasting revenues of US$1.0b and earnings per share (EPS) of US$1.24 in 2022. There looks to have been a major change in sentiment regarding NETGEAR's prospects, with a measurable cut to revenues and the analysts now forecasting a loss instead of a profit.

View our latest analysis for NETGEAR

The consensus price target fell 12% to US$24.50, implicitly signalling that lower earnings per share are a leading indicator for NETGEAR's valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic NETGEAR analyst has a price target of US$27.00 per share, while the most pessimistic values it at US$22.00. Still, with such a tight range of estimates, it suggests the analysts have a pretty good idea of what they think the company is worth.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 17% by the end of 2022. This indicates a significant reduction from annual growth of 1.0% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 6.7% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - NETGEAR is expected to lag the wider industry.

The Bottom Line

The biggest low-light for us was that the forecasts for NETGEAR dropped from profits to a loss this year. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that NETGEAR's revenues are expected to grow slower than the wider market. After such a stark change in sentiment from analysts, we'd understand if readers now felt a bit wary of NETGEAR.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple NETGEAR analysts - going out to 2024, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if NETGEAR might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:NTGR

NETGEAR

Provides connectivity solutions the Americas; Europe, the Middle East, Africa; and the Asia Pacific.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|11.6% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|0% overvalued

RO

Community Contributor