Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:LFUS

Does Recent Growth Justify Littelfuse’s Premium Valuation in 2025?

Reviewed by Bailey Pemberton

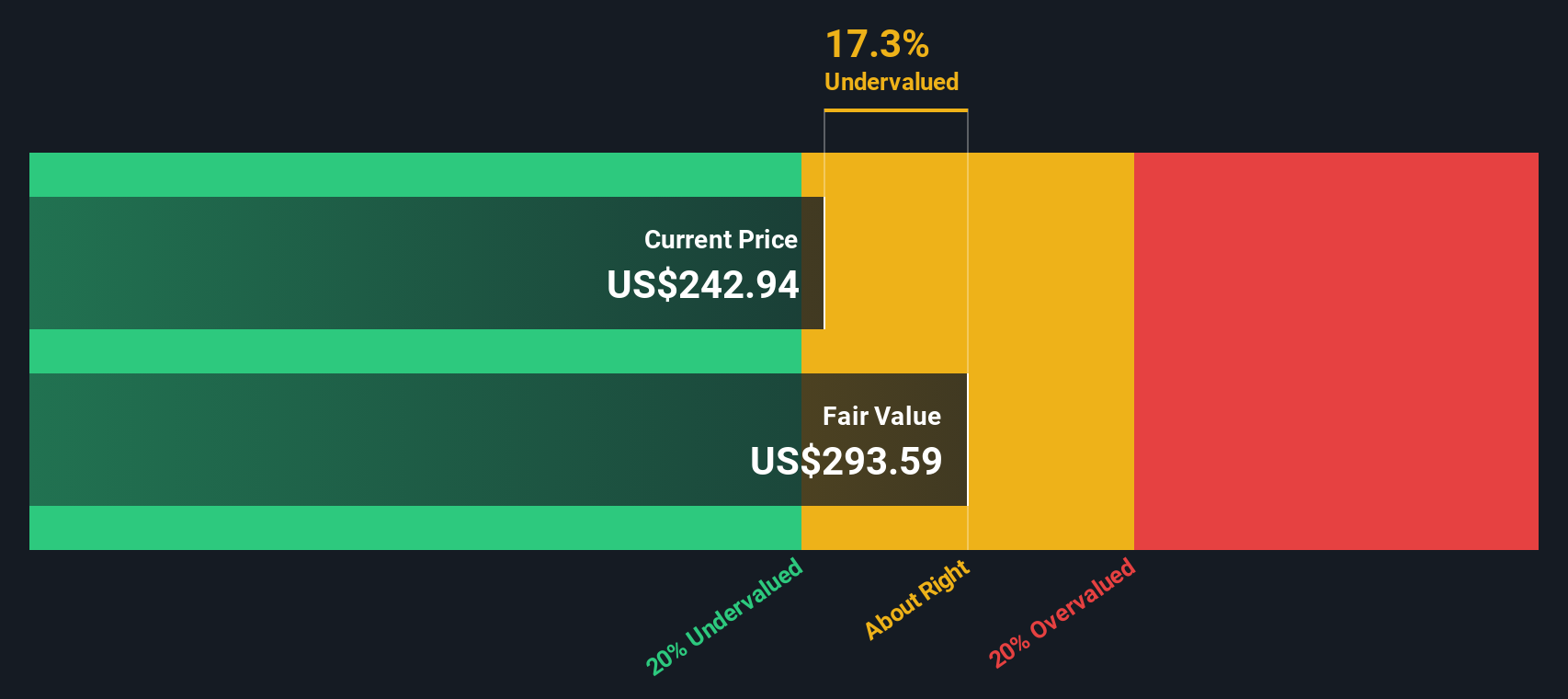

- If you have ever wondered whether Littelfuse is quietly trading below, at, or above its true worth, you are not alone and this breakdown is designed to give you a clear, no jargon answer.

- The stock has drifted a little in the short term, down 1.0% over the last week but still up 1.7% over 30 days, and it has quietly built a respectable track record with returns of 8.0% year to date and 4.1% over the past year, plus 10.1% over three years and 6.7% over five.

- Recent headlines around industrial automation demand, vehicle electrification and the ongoing build out of power management infrastructure have kept Littelfuse on the radar of investors looking for durable growth stories. At the same time, market commentary has focused on how niche component suppliers like Littelfuse can gain pricing power and margin resilience as electronics become more deeply embedded across industrial and auto end markets.

- Despite that backdrop, our valuation framework gives Littelfuse a value score of 1 out of 6, suggesting it only screens as undervalued on one of our core checks. In the next sections we will unpack what each valuation approach says about the stock and hint at a more holistic way to judge value that we will come back to at the end.

Littelfuse scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Littelfuse Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in $ terms. For Littelfuse, the 2 stage Free Cash Flow to Equity model starts from last twelve months free cash flow of about $376.5 million and uses analyst forecasts for the next few years, then gradually tapers growth beyond that. By 2029, annual free cash flow is projected to reach roughly $440.9 million, with further incremental increases extrapolated through 2035 as growth moderates.

Adding up all those future cash flows and discounting them back to today yields an estimated intrinsic value of about $294.75 per share. Compared with the current market price, this implies the stock trades at roughly a 14.0% discount, suggesting that, on cash flow grounds alone, investors are not fully pricing in Littelfuse’s long term earning power.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Littelfuse is undervalued by 14.0%. Track this in your watchlist or portfolio, or discover 927 more undervalued stocks based on cash flows.

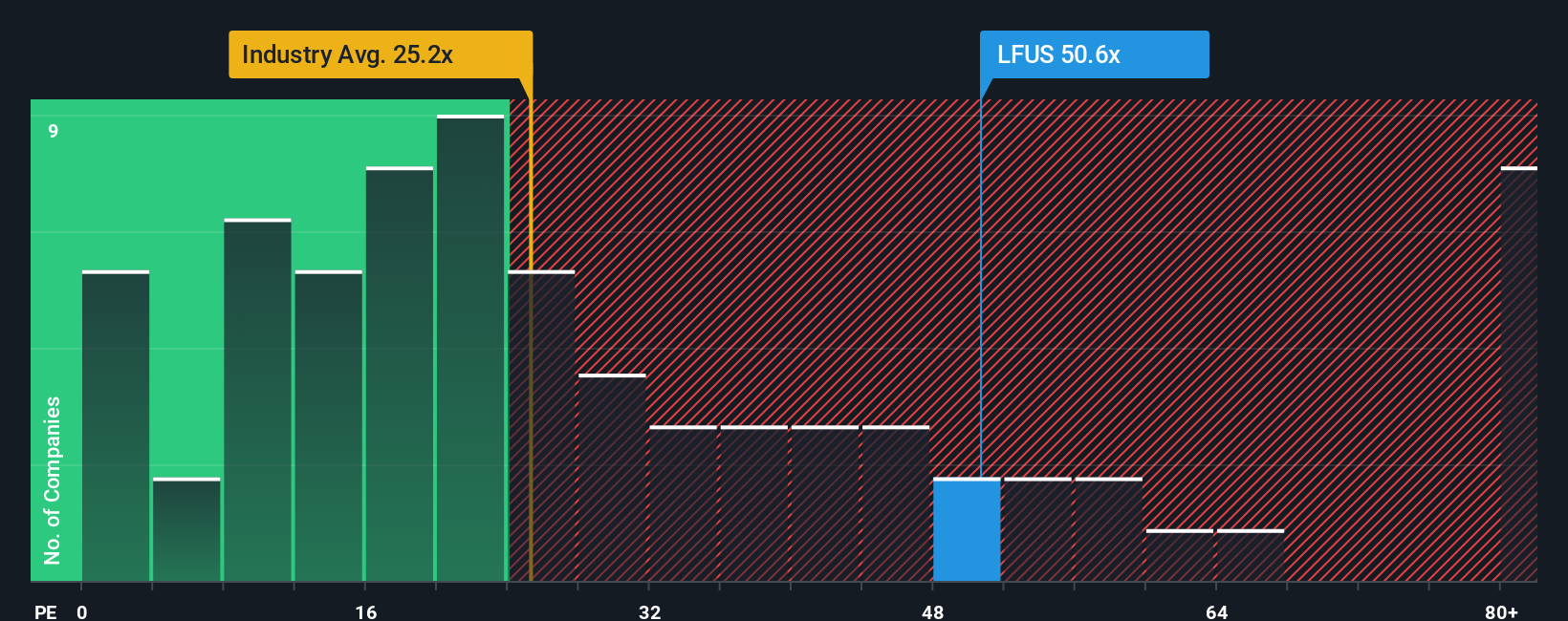

Approach 2: Littelfuse Price vs Earnings

For profitable companies like Littelfuse, the price to earnings (PE) ratio is a straightforward way to gauge how much investors are paying for each dollar of current profit. A higher PE can be justified when a business is expected to grow earnings quickly and has relatively low risk, while slower growth or higher uncertainty usually calls for a lower, more conservative multiple.

Littelfuse currently trades on a PE of about 53.2x, which is well above both the broader Electronic industry average of roughly 23.5x and the peer group average of about 38.2x. On the surface, that suggests investors are paying a premium for its earnings profile relative to many sector alternatives.

Simply Wall St’s Fair Ratio framework refines this comparison by estimating what a more tailored PE should be, given Littelfuse’s specific earnings growth outlook, profitability, risk factors, industry positioning and market cap. On that basis, the stock’s Fair Ratio is calculated at around 29.0x, which is significantly lower than the current 53.2x. This gap indicates that, even after accounting for its strengths and growth prospects, the market is pricing Littelfuse well above what our fundamentals based model would suggest.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Littelfuse Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework that lets you attach a clear story to your numbers by spelling out your view of a company’s future revenue, earnings and margins, linking that story to a financial forecast and then to a fair value estimate.

On Simply Wall St’s Community page, used by millions of investors, Narratives turn this into an accessible tool, so you can quickly see whether your Fair Value sits above or below today’s price and decide how Littelfuse fits into your portfolio strategy.

Because each Narrative automatically updates when new data, news, or earnings arrive, your view stays dynamic rather than static, which is essential in a fast moving market.

For example, one Littelfuse Narrative might emphasize potential benefits from electrification trends, rising margins and a fair value estimate above the current price. Another more cautious Narrative could focus on competitive pressures and execution risks, leading to a lower growth path, thinner margins and a fair value estimate below where the stock trades today. Both are transparent, comparable views you can explore and adapt to fit your own conviction.

Do you think there's more to the story for Littelfuse? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LFUS

Littelfuse

Designs, manufactures, and sells electronic components, modules, and subassemblies.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1939.7% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6527.1% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.6% undervalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30155.3% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

TI

Tiguidou on NanoXplore ·

NanoXplore et le le Noir de Carbone

Fair Value:CA$14.5789.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Silver Mines ·

Australia’s Largest Undeveloped Silver Project Just Got a Low-Cost Makeover

Fair Value:AU$4.1996.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VA

Valtersa on Saudi National Bank ·

Projected Fair Value of Saudi National Bank Reaches 52

Fair Value:ر.س5228.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.3% undervalued

90 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5451.0% undervalued

62 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3462.5% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

MA

Marek_Trnka on Space Exploration Technologies ·

I was right -15/7/2026 a return to the IPO price.

0

|0