Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:FLEX

How Flex’s Liquid Cooling Deployment with Equinix Could Reshape the FLEX Investment Story

Reviewed by Sasha Jovanovic

- Flex announced it has deployed a fully integrated, rack-level liquid cooling solution at the Equinix Co-Innovation Facility in Ashburn, Virginia, incorporating JetCool’s advanced liquid cooling technologies and demonstrating significant reductions in data center water and power consumption.

- This collaboration underscores Flex’s unique ability to address global data center challenges with end-to-end manufacturing, supply chain expertise, and lifecycle support for next-generation high-density computing environments.

- We will examine how Flex’s new liquid cooling deployment with Equinix could impact its investment narrative, especially as demand for efficient data center solutions grows.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Flex Investment Narrative Recap

To be a shareholder in Flex, you need to believe that the company’s end-to-end manufacturing strength and rapid innovation in data center cooling are well positioned to catch the ongoing demand for AI and cloud infrastructure. The recent Equinix liquid cooling deployment showcases Flex's technical expertise, but does not substantially alter the key short-term catalyst, which remains continued revenue growth from major hyperscale clients. The biggest risk continues to be Flex’s exposure to customer concentration within the data center segment; this news does not mitigate that challenge in a material way.

Among Flex’s recent announcements, its expanding partnership with NVIDIA to create modular AI factory systems is the most relevant complement to the Equinix news. Both highlight how Flex is deepening relationships with leaders in high-performance computing. These collaborations tie directly into the company’s major growth catalyst, the global shift toward more intensive, energy-efficient data center infrastructure, and reinforce Flex’s importance in that supply chain.

Yet, unlike near-term growth drivers, investors should also be mindful of the ongoing risk from customers pursuing their own in-house cooling and power manufacturing solutions...

Read the full narrative on Flex (it's free!)

Flex is projected to reach $29.1 billion in revenue and $1.3 billion in earnings by 2028. This outlook assumes a 3.7% annual revenue growth rate and an increase in earnings of approximately $409 million from the current $891 million.

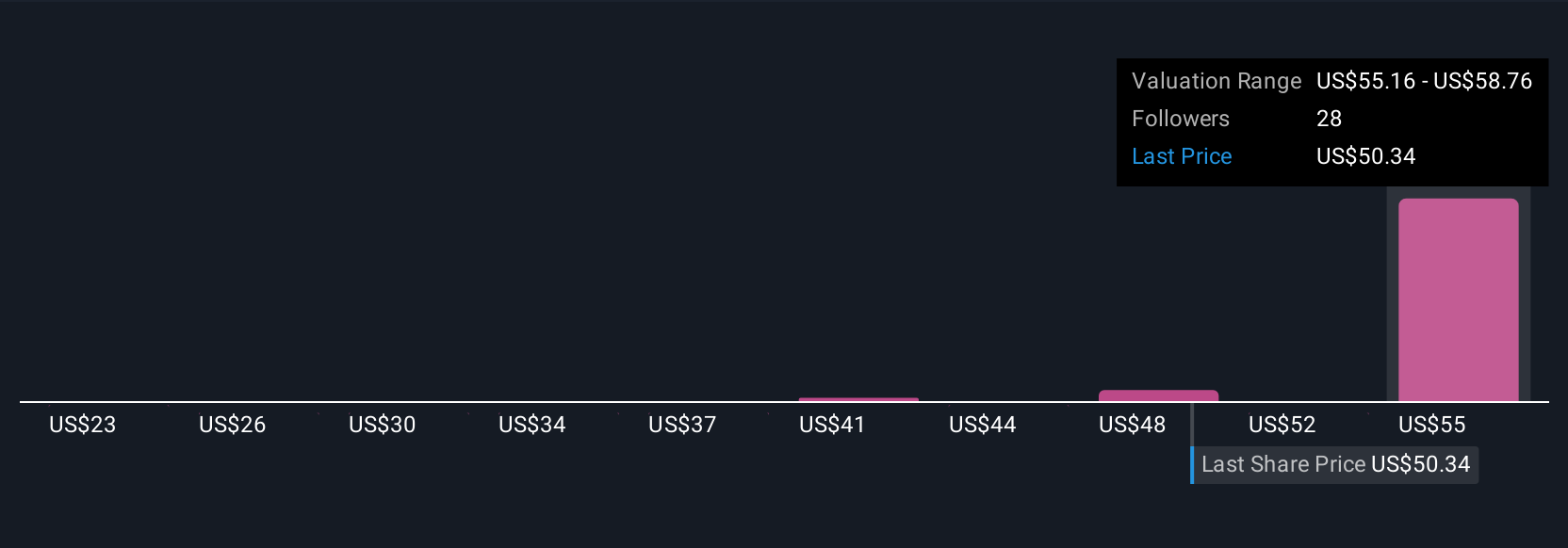

Uncover how Flex's forecasts yield a $74.37 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Five fair value estimates for Flex from the Simply Wall St Community range widely from US$45.00 to US$74.37 per share. While many see upside in Flex riding industry demand for data center innovation, opinions differ on the company’s ability to manage customer concentration and margin risks, take a closer look at these contrasting views.

Explore 5 other fair value estimates on Flex - why the stock might be worth as much as 24% more than the current price!

Build Your Own Flex Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Flex research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Flex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Flex's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FLEX

Flex

Provides technology innovation, supply chain, and manufacturing solutions to data center, communications, enterprise, consumer, automotive, industrial, healthcare, industrial, and power industries.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0777.3% undervalued

156 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k10.0% overvalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9412.5% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87179.9% overvalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

AB

Abhishekgarg on Pidilite Industries ·

High quality compounder, but current valuation leaves limited margin of safety.

Fair Value:₹1.31k2.4% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PA

Paddy_Ho on PaySauce ·

NZ company with gumption aims to provide services to SMEs across The Ditch

Fair Value:NZ$0.3623.6% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JC

JCAPITAL on Security Bank ·

YoY Percentage Growth: +5.8%

Fair Value:₱22169.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

55 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9826.5% undervalued

47 followersusers have followed this narrative

0 commentsusers have commented on this narrative

35 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6437.4% undervalued

38 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0