Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqCM:DAIO

One Data I/O Corporation (NASDAQ:DAIO) Analyst Has Been Cutting Their Forecasts

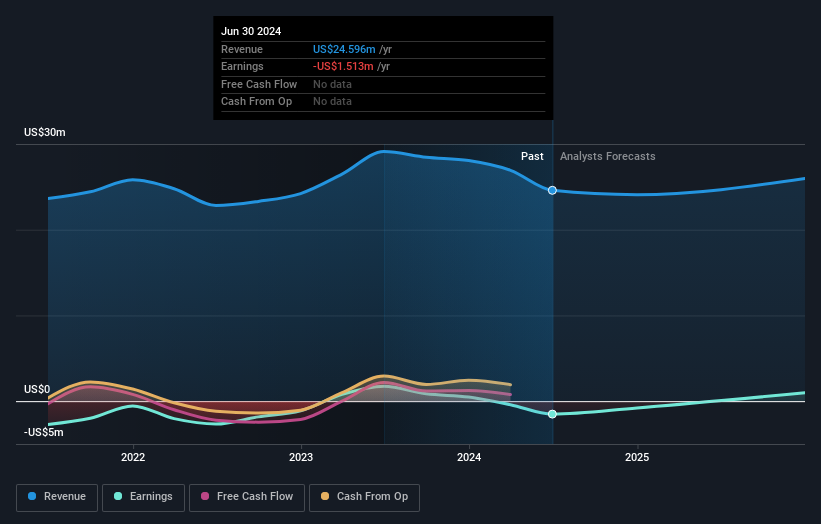

Today is shaping up negative for Data I/O Corporation (NASDAQ:DAIO) shareholders, with the covering analyst delivering a substantial negative revision to this year's forecasts. Both revenue and earnings per share (EPS) estimates were cut sharply as the analyst factored in the latest outlook for the business, concluding that they were too optimistic previously.

Following the latest downgrade, the current consensus, from the solitary analyst covering Data I/O, is for revenues of US$24m in 2024, which would reflect a noticeable 2.1% reduction in Data I/O's sales over the past 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 45% to US$0.09. Prior to this update, the analyst had been forecasting revenues of US$29m and earnings per share (EPS) of US$0.10 in 2024. So we can see that the consensus has become notably more bearish on Data I/O's outlook with these numbers, making a substantial drop in this year's revenue estimates. Furthermore, they expect the business to be loss-making this year, compared to their previous forecasts of a profit.

View our latest analysis for Data I/O

The consensus price target fell 20% to US$4.00, implicitly signalling that lower earnings per share are a leading indicator for Data I/O's valuation.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that sales are expected to reverse, with a forecast 4.1% annualised revenue decline to the end of 2024. That is a notable change from historical growth of 4.9% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 7.0% per year. It's pretty clear that Data I/O's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest low-light for us was that the forecasts for Data I/O dropped from profits to a loss this year. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. After such a stark change in sentiment from the analyst, we'd understand if readers now felt a bit wary of Data I/O.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2025, which can be seen for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:DAIO

Data I/O

Engages in the design, manufacture, and sale of programming and security deployment systems and services for electronic device manufacturers in the United States, Germany, China, Mexico, and Korea.

Flawless balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2552.0% undervalued

120 followersusers have followed this narrative

0 commentsusers have commented on this narrative

25 likesusers have liked this narrative

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4848.5% undervalued

221 followersusers have followed this narrative

9 commentsusers have commented on this narrative

33 likesusers have liked this narrative

HE

HedgeY on Arm Holdings ·

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Fair Value:US$43044.3% undervalued

23 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9955.0% undervalued

31 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

AR

ariz_scribe on Marti Technologies ·

$MRT at Roth - Pick of the Panel

Fair Value:US$1.965.6% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on Vistance Networks ·

VISN trades at $11.83 with roughly $1.88 billion of cash and zero debt after closing the sale of its Ruckus division to Belden on July 1

Fair Value:US$1626.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on Vertiv Holdings Co ·

Everyone's Favorite Stock Just Fell 17% in a Day. It Still Isn't Cheap.

Fair Value:US$21313.4% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28028.3% undervalued

220 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9110.7% overvalued

98 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23054.8% overvalued

115 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

1

|0

BL

Blegells on Terra Balcanica Resources ·

⏫42X THE AVERAGE DAILY TRADING VOLUME TODAY, JULY 28 🐂🐂🐂 FORTY-TWO!

1

|0