Advertisement

- United States

- /

- Communications

- /

- NasdaqGS:CSCO

Assessing Cisco Systems (CSCO) Valuation After Recent Share Price Pullback Without Clear News Catalyst

Cisco Systems stock moves without a clear news catalyst

Cisco Systems (CSCO) shares have been moving without a clear single event driving sentiment, which can prompt investors to look more closely at the company’s recent returns and financial profile.

See our latest analysis for Cisco Systems.

Cisco’s recent share price pullback, including a 5.55% 1 month share price return and 3.09% year to date share price return, contrasts with a stronger 21.29% 1 year total shareholder return and 65.98% 3 year total shareholder return. This hints at cooling short term momentum against a broader record of gains.

If this kind of shift in sentiment has you rethinking your watchlist, it could be a good moment to widen your radar with high growth tech and AI stocks.

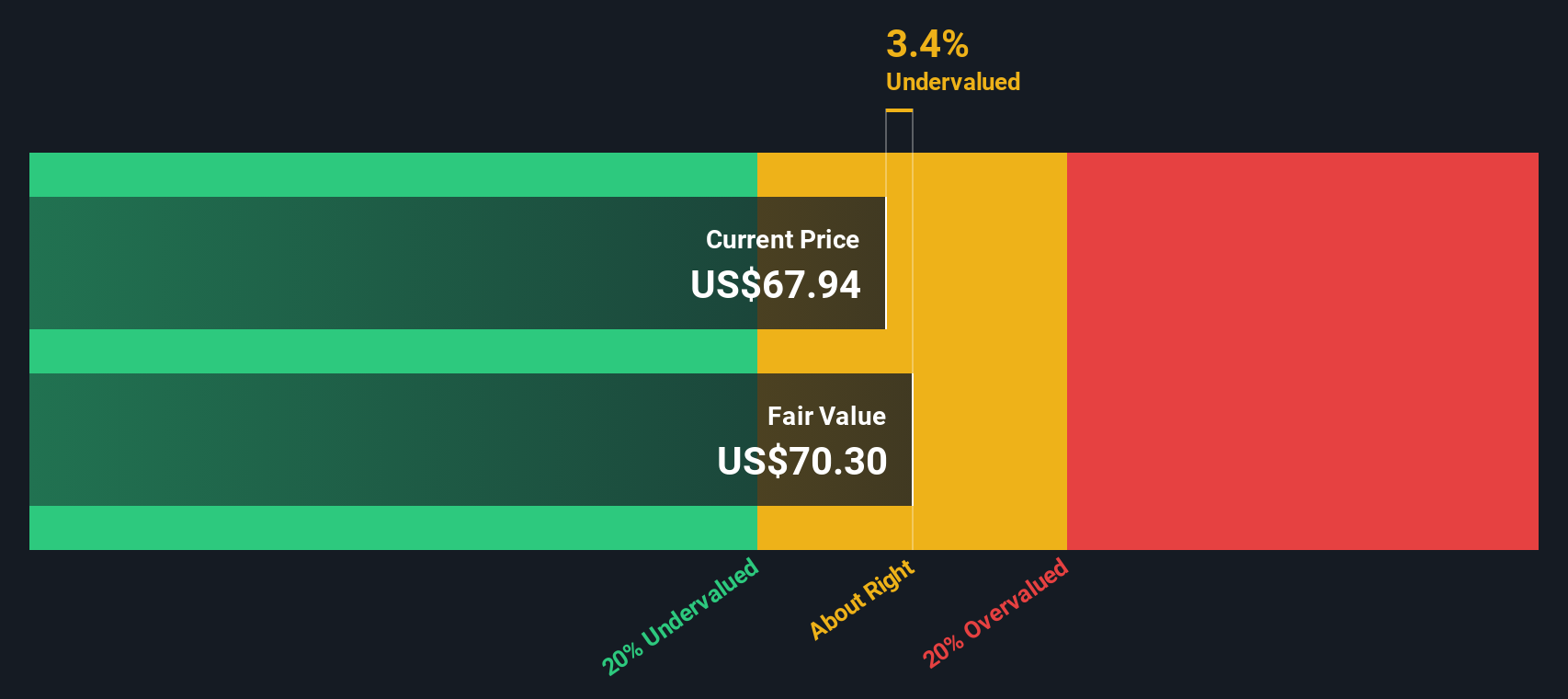

With Cisco trading at $73.69 and sitting at an estimated 12.09% intrinsic discount and 16.70% below its US$85.999 price target, you have to ask: is this a genuine entry point, or is the market already factoring in future growth?

Price-to-Earnings of 28.2x: Is it justified?

At a last close of US$73.69, Cisco is trading on a P/E of 28.2x, which screens as good value both against its own fair ratio and its peers.

The P/E multiple compares Cisco’s share price to its earnings per share, so it is a quick way to see how much investors are paying for each dollar of profit.

CSCO is flagged as good value based on its P/E of 28.2x versus an estimated fair P/E of 29.8x, which suggests the market price is slightly below the level the fair ratio model points to. Cisco also has high quality earnings and a Return on Equity of 22%, which can help explain why the earnings multiple is not at a steep discount.

Against the broader US Communications industry, Cisco’s 28.2x P/E is described as good value both versus the industry average and the peer average of 35.6x, so the stock changes hands at a lower earnings multiple than many comparable companies even after a strong multi year total return profile.

Explore the SWS fair ratio for Cisco Systems

Result: Price-to-Earnings of 28.2x (UNDERVALUED)

However, you also have to weigh risks such as slower revenue growth at 5.25% annually, as well as the possibility that tech hardware spending cycles cool sentiment further.

Find out about the key risks to this Cisco Systems narrative.

Another View: What Our DCF Model Suggests

Cisco screens as good value on its 28.2x P/E, and our DCF model also points to undervaluation, with the shares at US$73.69 versus an estimated future cash flow value of US$83.82. That is roughly a 12% gap, which raises a simple question: is the market being too cautious about Cisco’s cash generation?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Cisco Systems for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 883 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Cisco Systems Narrative

If you see the numbers differently or want to rely on your own view of Cisco, you can build a complete story in just a few minutes with Do it your way.

A great starting point for your Cisco Systems research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one company. Use the Simply Wall St Screener to spot fresh ideas before others notice them.

- Target growth potential early by reviewing these 3528 penny stocks with strong financials that already show stronger financials than many expect at this end of the market.

- Tap into long term tech themes by scanning these 24 AI penny stocks that are tied to artificial intelligence trends across multiple sectors.

- Focus on price and quality together by sifting through these 883 undervalued stocks based on cash flows that our models flag as trading below their estimated cash flow value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CSCO

Cisco Systems

Designs, develops, and sells technologies that help to power, secure, and draw insights from the internet in the Americas, Europe, the Middle East, Africa, the Asia Pacific, Japan, and China.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4342.5% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7833.2% undervalued

31 followersusers have followed this narrative

5 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1752.7% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6435.3% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

17 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Quanta Services ·

Quanta Services (PWR): Strengthening the Backbone of the AI Power Grid.

Fair Value:US$5464.0% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on KLA ·

KLA Corporation (KLAC): Engineering Yield in the Age of Chiplets and Sub-2nm Nodes.

Fair Value:US$1.5k4.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Monolithic Power Systems ·

Monolithic Power Systems (MPWR): The AI "Power Play" Facing a Transition from Scarcity to Scale.

Fair Value:US$1.27k16.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.2% undervalued

51 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.8% undervalued

1102 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.3% undervalued

1302 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative