- United States

- /

- Communications

- /

- NasdaqGS:CRNT

Ceragon Networks (NasdaqGS:CRNT) Dips 12% Over Last Week Amid Escalating US-China Trade Tensions

Reviewed by Simply Wall St

Ceragon Networks (NasdaqGS:CRNT) experienced a 12.13% decline in its share price over the past week. This sharp drop aligns with broader market turbulence, driven by significant declines in major indexes. The Dow plunged 7.9% and the Nasdaq Composite slipped 10%, both rattled by escalating trade tensions following U.S. and Chinese tariff announcements. The market's sell-off was largely driven by the fear of reduced corporate profits and slowed economic growth, affecting sentiments across sectors. In tandem with this market-wide downturn, Ceragon's stock performance reflects the heightened volatility and economic uncertainty impacting technology and communication stocks like CRNT.

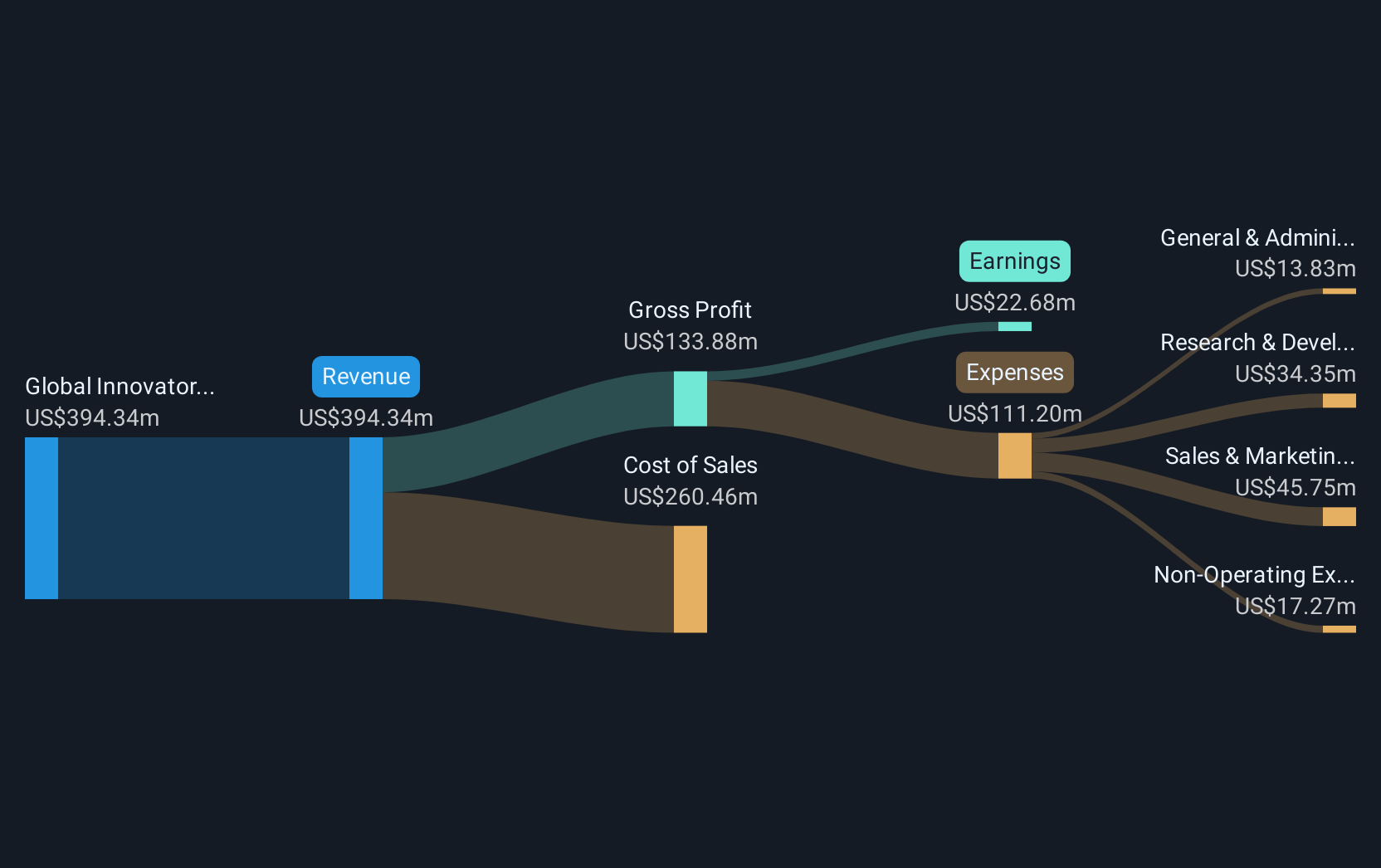

The last five years have seen Ceragon Networks deliver a total return of 18.64%, including share price gains and dividends. Key developments contributing to this performance include the launch of new products such as the millimeter-wave backhaul EtherHaul 8020FX and the IP-50EXA, enhancing Ceragon’s market presence. Additionally, a significant multi-million-dollar order from a U.S. ISP in July 2024 indicated strong demand for Ceragon's solutions, further supporting revenue growth. Ceragon's earnings over the past year have also been resilient, as seen in the Q3 2024 earnings report, which reflected an increase in sales to US$102.67 million, with net income rising to US$12.22 million from the prior year.

Despite these achievements, Ceragon faced challenges including geopolitical tensions and economic uncertainties such as inflation and supply chain issues that have impacted overall growth. Furthermore, the company's one-year return underperformed both the US Communications industry and the broader market. This underperformance highlights the complex landscape in which the company operates, even as it continues to grow its earnings substantially. With 2025 revenue guidance ranging between US$390 million and US$430 million, Ceragon remains focused on expanding its footprint through strategic initiatives and acquisitions.

Our valuation report here indicates Ceragon Networks may be undervalued.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CRNT

Ceragon Networks

Provides wireless transport solutions for cellular operators and other wireless service providers in North America, Europe, Africa, the Asia Pacific, the Middle East, India, and Latin America.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives