Advertisement

- United States

- /

- Software

- /

- NYSE:BMNR

Can Bitmine’s Soaring 709% Rise Continue After New Cooling Tech Drives Buzz?

Reviewed by Bailey Pemberton

Thinking about what to do with Bitmine Immersion Technologies stock? You're not alone. With its headline-grabbing returns, up a staggering 12.2% in just the last week and a jaw-dropping 709.3% for the year to date, investors are buzzing about what’s fueling this crypto-adjacent powerhouse and, more importantly, whether there's still room to grow. The momentum does not feel random, either. Market chatter has zeroed in on the company’s expansion into next-generation cooling tech for mining facilities, a move that’s earning applause as concerns about energy efficiency ramp up across the industry.

But let's address the elephant in the room: valuation. For all the excitement, Bitmine Immersion Technologies currently scores a 0 out of 6 on our valuation check, meaning it is not undervalued by any of the traditional metrics we track. While past performance has certainly been spectacular (a blistering 746.8% return over the past year), the numbers suggest that investors may already be pricing in a lot of optimism, or perhaps a new perception of lower risk.

So, how does a stock with such a meteoric rise stack up once we dig into different valuation methods? Plenty of analysts rely on the familiar yardsticks, but stay tuned as we walk through these approaches and explore what really matters when assessing Bitmine’s value in today’s market.

Bitmine Immersion Technologies scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Bitmine Immersion Technologies Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting future cash flows and discounting them back to their present value. This helps determine what the company could be worth today, based purely on its expected ability to generate cash.

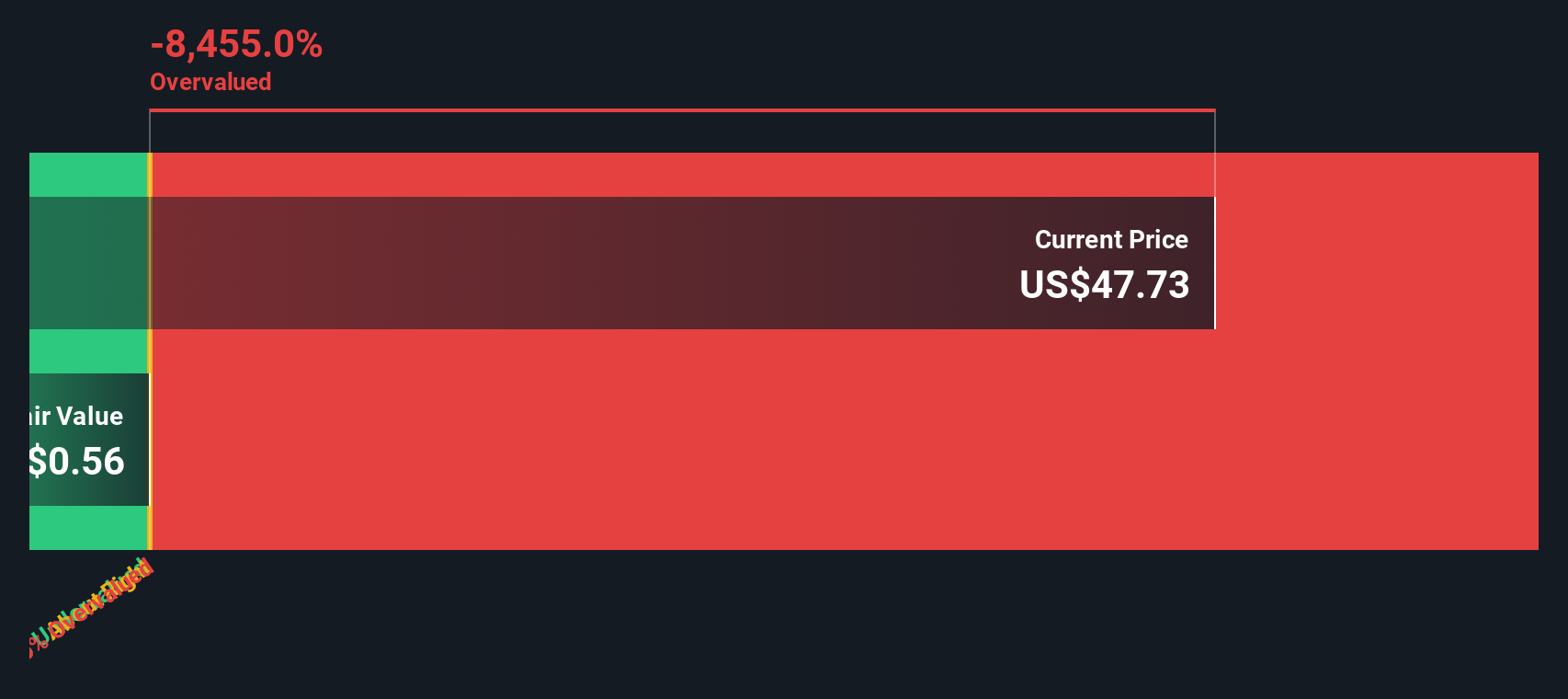

For Bitmine Immersion Technologies, the reported Free Cash Flow (FCF) over the last twelve months is $0.84 million. Projections suggest robust growth, with FCF rising to around $7.75 million by 2035. Analysts typically provide FCF estimates for up to five years, while later projections, such as these, are extrapolated based on current trends and industry expectations.

Using these cash flow estimates and a two-stage free cash flow to equity model, the DCF analysis yields a fair value of $0.53 per share. However, with the market pricing in significantly more optimism, the DCF calculation indicates that Bitmine shares are trading about 10,537.6 percent above their estimated intrinsic value. This suggests the stock is extremely overvalued by this metric.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Bitmine Immersion Technologies may be overvalued by 10537.6%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Bitmine Immersion Technologies Price vs Book

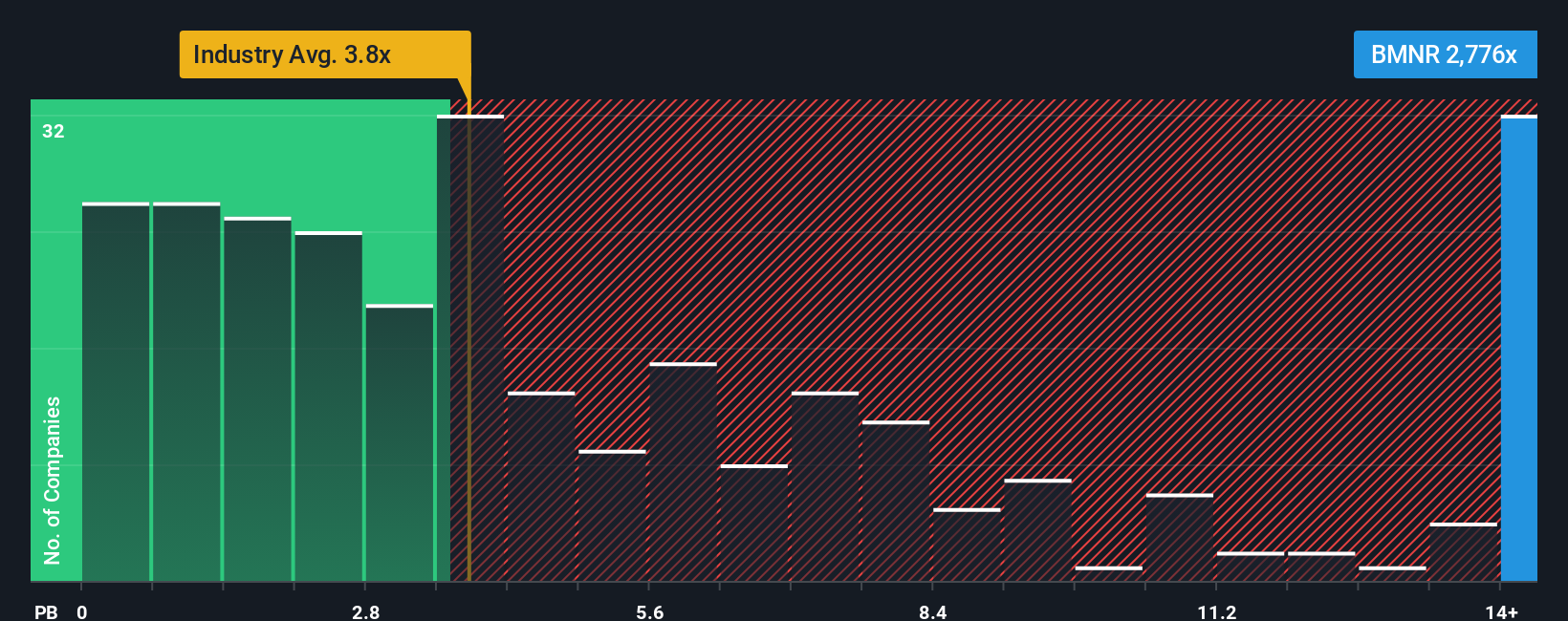

When assessing the value of a profitable business like Bitmine Immersion Technologies, the Price-to-Book (PB) ratio is often a reliable starting point. This metric helps investors determine how much they are paying for each dollar of the company’s net assets, which can be particularly relevant for companies in capital-intensive or asset-heavy sectors.

Market optimism and expectations for rapid growth or reduced risk tend to justify higher PB ratios, whereas caution about the future will pull these multiples closer to or below industry norms. Understanding what baseline is considered “fair” matters, especially given the sector’s tendency for big swings in sentiment.

Currently, Bitmine trades at a PB multiple of 3,517.89x, a figure that dramatically outpaces both the industry average of 3.99x and the peer average of 11.55x. These eye-popping multiples raise immediate questions about whether the market’s exuberance is warranted based only on tangible book value.

This is where Simply Wall St’s proprietary “Fair Ratio” comes into play. Unlike a basic peer or industry comparison, the Fair Ratio considers not just growth and risk levels, but also factors such as margins, size, and the company’s specific operating environment. By tailoring the expectation of a “normal” PB multiple to the full context, the Fair Ratio aims to spot situations where traditional benchmarks might miss the mark.

In this case, Bitmine’s actual PB ratio is vastly higher than what the Fair Ratio would justify, suggesting the shares are commanding a premium far in excess of their fundamental value.

Result: OVERVALUED

PB ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Bitmine Immersion Technologies Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is a simple, story-driven approach that lets you connect your perspective on a company with real numbers, such as your fair value estimate and assumptions for future revenue, profit margins, and more. Instead of only relying on ratios and past performance, Narratives empower you to tie Bitmine’s evolving story directly to a financial forecast and fair value. This makes your investment decisions more meaningful and personal.

Available right now on Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors. They help you decide when to buy or sell by instantly comparing your calculated fair value against the live share price. Narratives also keep you updated automatically when new data, news, or earnings are released, ensuring your outlook stays current. For Bitmine Immersion Technologies, you might see one investor’s bullish Narrative with aggressive growth assumptions and a high fair value, while another, more cautious Narrative projects a much lower price based on conservative estimates. Narratives bring your investment decisions to life, giving you clarity, flexibility, and control.

Do you think there's more to the story for Bitmine Immersion Technologies? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bitmine Immersion Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BMNR

Bitmine Immersion Technologies

Operates as a blockchain technology company primarily in the United States.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2537.3% undervalued

140 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0330.9% undervalued

12 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.528.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.725.6% undervalued

12 followersusers have followed this narrative

3 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on A2 Gold ·

Nevada Gold Silver Giant: 1.4Moz Gold + 20Moz Silver Potential, Kinross-Backed Nevada Play Exploding?

Fair Value:CA$4.2484.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RC

rcb9 on DocuSign ·

Strip The Tax Benefit And Earnings Grew 36%

Fair Value:US$60.995.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RC

rcb9 on Boeing ·

The Operations Turned Profitable, The Balance Sheet Has Not

Fair Value:US$160.0148.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28024.3% undervalued

248 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9117.4% overvalued

118 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$202.6286.4% overvalued

133 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

4

|0

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0