Advertisement

- United States

- /

- Software

- /

- NYSE:U

Is Piper Sandler’s Vector-Focused Optimism Altering The Investment Case For Unity Software (U)?

Reviewed by Sasha Jovanovic

- Piper Sandler recently issued a positive research note on Unity Software, highlighting strong progress in rebuilding its Grow segment around the AI-powered advertising platform Vector.

- The broker’s view that competitive and AI-related risks are less severe than feared underscores Unity’s strengthening position within AI-driven advertising technology.

- We’ll now examine how this upbeat assessment of Unity’s Vector-powered Grow business fits into and potentially reshapes the broader investment narrative.

Find 45 companies with promising cash flow potential yet trading below their fair value.

Unity Software Investment Narrative Recap

To own Unity today, you need to believe its engine and ad tools can turn rapid product innovation into a path toward profitability, despite large current losses. Piper Sandler’s upbeat view on Vector suggests Unity’s rebuilt Grow segment might be a nearer term support for sentiment, but it does not erase the key risk that heavy AI and R&D spending could still keep margins under pressure.

The recent decision to sunset the ironSource Ads Network and divest Supersonic is particularly relevant here, because it concentrates Unity’s ad efforts around Vector and higher margin services. If this transition executes smoothly, it could reinforce the broker’s confidence in the Grow segment as an important catalyst, while also testing Unity’s ability to simplify its portfolio without adding new operational or customer concentration risks.

Yet against these positives, investors should still pay close attention to how rising data privacy and compliance demands might affect Unity’s AI driven ad products and...

Read the full narrative on Unity Software (it's free!)

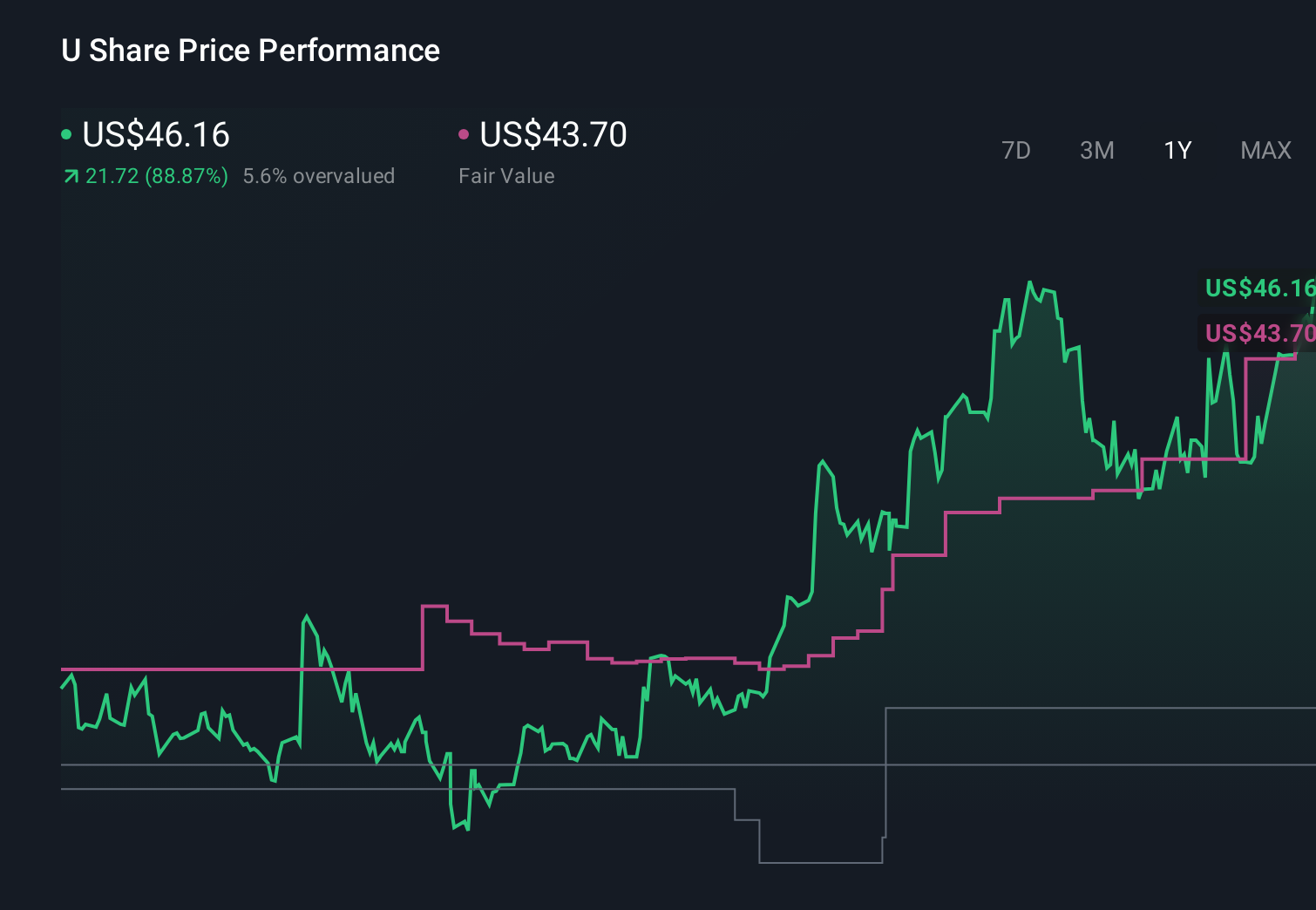

Unity Software’s narrative projects $2.9 billion revenue and $711.1 million earnings by 2029. This requires 14.2% yearly revenue growth and about a $1.38 billion earnings increase from -$672.7 million today.

Uncover how Unity Software's forecasts yield a $34.39 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already projecting Unity to reach about US$3.1 billion in revenue and around US$334.6 million in earnings, which assumes strong AI and VR driven growth. Compared with the baseline concerns around spending and competition, this is a much more optimistic narrative. You should expect that upbeat Vector news could either reinforce or challenge those forecasts once expectations reset.

Explore 7 other fair value estimates on Unity Software - why the stock might be worth as much as 97% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Unity Software research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Unity Software research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Unity Software's overall financial health at a glance.

No Opportunity In Unity Software?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Explore 31 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:U

Unity Software

Operates a platform to develop, deploy, and grow games and interactive experiences for mobile phones, PCs, consoles, and extended reality devices in the United States, China, Hong Kong, Taiwan, Europe, the Middle East, Africa, the Asia Pacific, Canada, and Latin America.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

13 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on American Resources ·

American Resources, $263M Market Cap + 19% ReElement Stake, From Coal to Critical Minerals

Fair Value:US$557.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on EPB Group Berhad ·

EPB: Strong Shareholder Backing, Continuous Insider Buying and Growth Opportunities Ahead

Fair Value:RM 0.548.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YO

youwakeup on Harvest Strategy Enhanced High Income Shares ETF ·

MSTE: Turning Bitcoin Volatility Into Monthly Cash Flow

Fair Value:CA$11.7579.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

58 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative