- United States

- /

- Software

- /

- NYSE:S

Assessing SentinelOne (S) Valuation as Purple AI Momentum and $1B ARR Shift Focus Beyond Endpoint Security

Reviewed by Simply Wall St

SentinelOne (S) has landed squarely in the spotlight after crossing $1 billion in annual recurring revenue and showcasing its Purple AI driven platform in high profile breach investigations, giving investors fresh reasons to revisit the stock.

See our latest analysis for SentinelOne.

Despite the excitement around its AI platform and high profile breach work, SentinelOne’s 1 year total shareholder return of around negative 37% and year to date share price return of roughly negative 33% show sentiment has cooled, even as its 3 year total shareholder return stays modestly positive.

If you like SentinelOne’s AI driven angle but want to see what else is out there, this is a good moment to explore high growth tech and AI stocks for fresh ideas.

With shares trading at a discount to both analyst targets and high growth peers, yet still loss making as it pivots into a broader AI platform, is SentinelOne quietly undervalued, or is the market already discounting all that future growth?

Most Popular Narrative Narrative: 30.0% Undervalued

With the most followed narrative pointing to a fair value near 21.55 dollars against a 15.08 dollar last close, the valuation hinges on aggressive improvement in growth and margins over the next few years.

The new SentinelOne Flex licensing model is accelerating multi product adoption, leading to larger deal sizes, increased platform retention, and rising recurring revenue, all of which support both near term and long term net margin expansion through reduced sales friction and deeper customer integration.

Curious how recurring revenue, rising margins, and a premium future earnings multiple all line up to justify that upside case? The narrative’s math is far bolder than it first appears.

Result: Fair Value of $21.55 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, execution risks around international expansion, combined with heavy reliance on hyperscaler partnerships, could pressure margins and growth if regulatory or competitive dynamics turn less favorable.

Find out about the key risks to this SentinelOne narrative.

Another Angle on Valuation

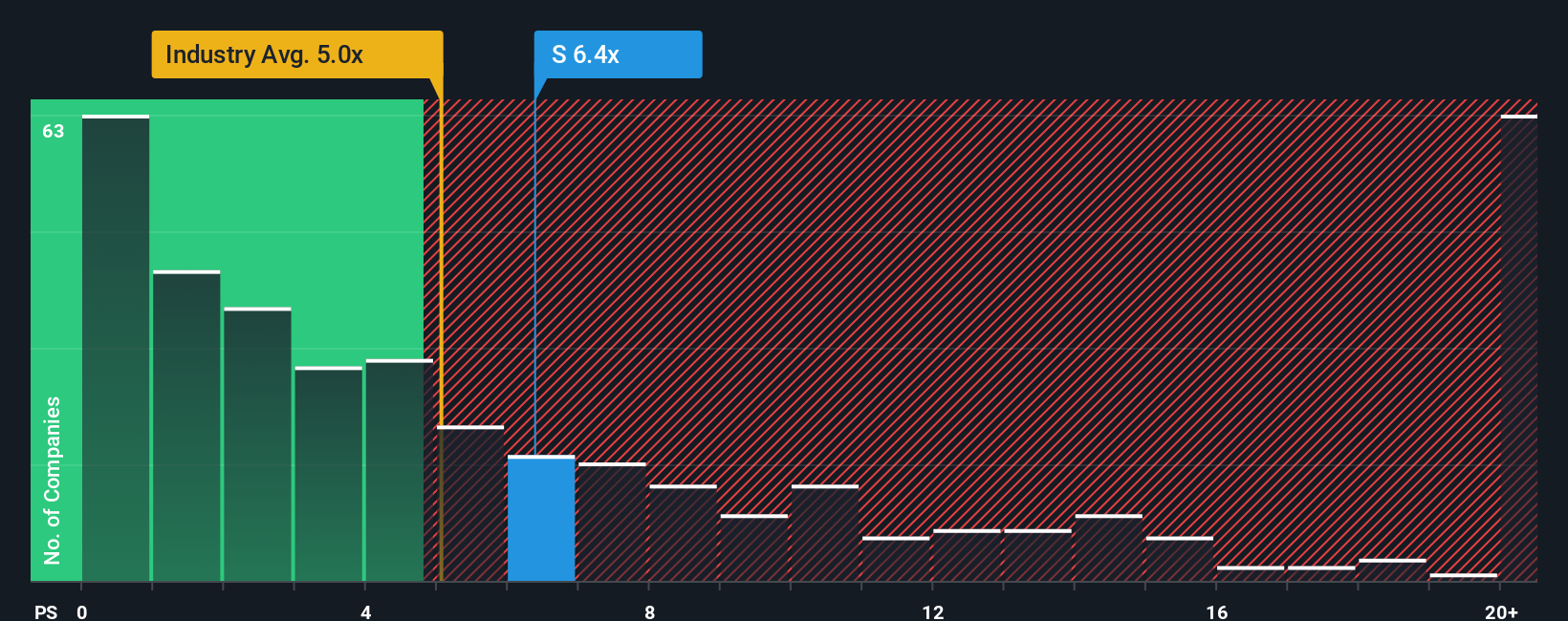

On sales based metrics, SentinelOne looks far less cheap. Its price to sales ratio of 5.4 times tops the US Software industry at 4.9 times, even though our fair ratio suggests the market could justify 6 times. Is this a margin of safety, or a value trap in disguise?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own SentinelOne Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a personalized view in just minutes, Do it your way.

A great starting point for your SentinelOne research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

Do not stop at one compelling story. Use the Simply Wall Street Screener now and line up your next smart moves before the market catches on.

- Review these 13 dividend stocks with yields > 3% that aim to balance yield with business strength and long term sustainability.

- Explore these 26 AI penny stocks that focus on innovation in artificial intelligence across software, hardware, and everyday workflows.

- Consider these 907 undervalued stocks based on cash flows where cash flow strength and sentiment mispricing may be creating uncommon opportunities.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:S

SentinelOne

Operates as a cybersecurity provider in the United States and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)