Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:PSFE

Earnings Release: Here's Why Analysts Cut Their Paysafe Limited (NYSE:PSFE) Price Target To US$3.25

Shareholders might have noticed that Paysafe Limited (NYSE:PSFE) filed its quarterly result this time last week. The early response was not positive, with shares down 8.9% to US$2.06 in the past week. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

See our latest analysis for Paysafe

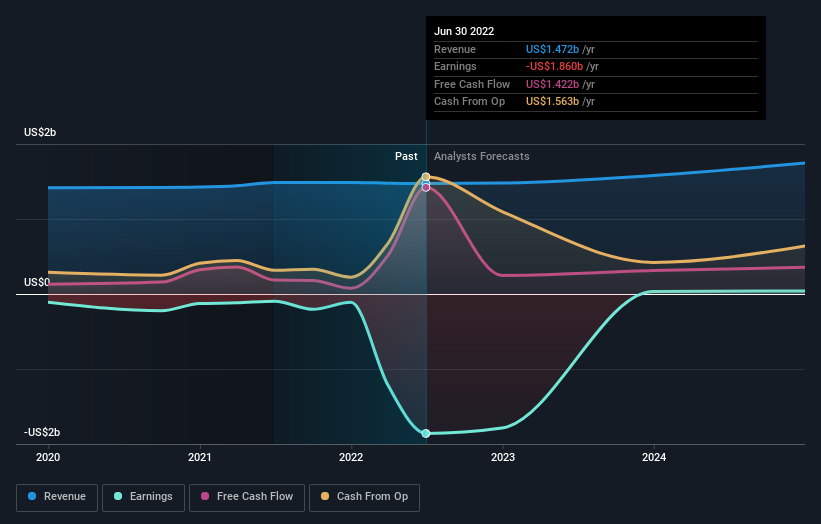

Taking into account the latest results, Paysafe's seven analysts currently expect revenues in 2022 to be US$1.48b, approximately in line with the last 12 months. The loss per share is expected to ameliorate slightly, reducing to US$2.47. Before this earnings announcement, the analysts had been modelling revenues of US$1.53b and losses of US$1.58 per share in 2022. While this year's revenue estimates dropped there was also a sizeable expansion in loss per share expectations, suggesting the consensus has a bit of a mixed view on the stock.

The consensus price target fell 10% to US$3.25, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Paysafe at US$5.00 per share, while the most bearish prices it at US$2.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. It's also worth noting that the years of declining sales look to have come to an end, with the forecast for flat revenues to the end of 2022. Historically, Paysafe's sales have shrunk approximately 1.1% annually over the past year. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 12% per year. So it's pretty clear that, although revenues are improving, Paysafe is still expected to grow slower than the industry.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. Unfortunately, they also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Paysafe's future valuation.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Paysafe analysts - going out to 2024, and you can see them free on our platform here.

You can also view our analysis of Paysafe's balance sheet, and whether we think Paysafe is carrying too much debt, for free on our platform here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:PSFE

Paysafe

Provides end-to-end payment solutions in the United States, Germany, the United Kingdom, and internationally.

Moderate growth potential with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor