Advertisement

- United States

- /

- Software

- /

- NYSE:PATH

UiPath (NYSE:PATH) Doesn't Need to Worry About the Negative Market Sentiment Yet

UiPath(NYSE: PATH) made a promising public trading debut early this year, but after rising 30% at one point, the stock is now down 25% YTD. It seems that, despite the growing revenues, the market remains concerned by the possible dilution and insider selling due to high stock-based compensation.

See our latest analysis for UiPath.

Q3 Earnings Results

- Non-GAAP EPS: US$0.00 (beat by US$0.04)

- GAAP EPS: -US$0.23 (miss by US$0.11)

- Revenue: US$220.82M (beat by US$11.59m)

Other Highlights

- Annual recurring revenue (ARR) increased 58% Y/Y to US$818m

- Non-GAAP gross margin at 85%

- Cash and cash equivalents: US$1.9b as of October 31

- For Q4, the company sees ARR in the range of US$901m to 903M, with non-GAAP operating income at US$10m-20m.

Meanwhile, Morgan Stanley took a contrarian position, upgrading the stock to Overweight, with a price target of US$74. Despite the growing competition, their analyst Keith Weiss believes that UiPath's strong positioning for a broader Enterprise Automation platform presents a valuable long-term opportunity.

While the robotic process automation (RPA) market is currently worth around US$2b, Mr.Weiss believes it could reach as much as US$56b.

Given this risk, we thought we'd look at whether UiPath shareholders should be worried about its cash burn. For this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow.

How Long Is UiPath's Cash Runway?

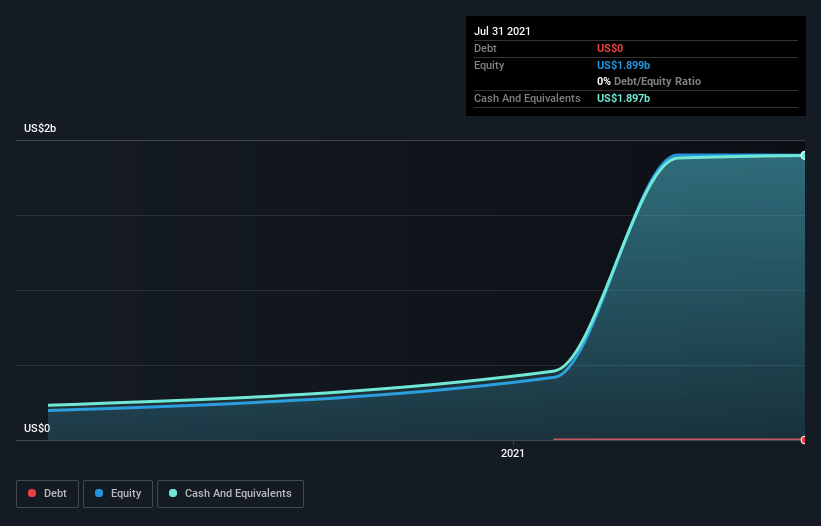

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As of October 2021, UiPath had cash of US$1.9b and no debt.

In the last year, its cash burn was US$5.4m. That means it had no problem with the cash runaway. While this is only one measure of its cash burn situation, it certainly gives us the impression that holders have nothing to worry about.

The image below shows how its cash balance has changed over the last few years.

How Well Is UiPath Growing?

Given our focus on UiPath's cash burn, we're delighted to see that it reduced its cash burn by 97%. And it is also great to see that the revenue is up 119% in the same time period. Considering these factors, we're fairly impressed by its growth trajectory.

While the past is always worth studying, it is the future that matters most. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Hard Would It Be For UiPath To Raise More Cash For Growth?

There's no doubt UiPath seems to be in a fairly good position when it comes to managing its cash burn, but even if it's only hypothetical, it's always worth asking how easily it could raise more money to fund growth. Companies can raise capital through either debt or equity.

Since it has a market capitalization of US$25b, UiPath's US$5.4m in cash burn equates to about 0.02% of its market value. That means it could easily issue a few shares to fund more growth and might well be in a position to borrow cheaply.

Is UiPath's Cash Burn A Worry?

It may already be apparent to you that we're relatively comfortable with the way UiPath is burning through its cash. For example, we think its cash burn reduction suggests that the company is on a good path. And even its cash burn relative to its market cap was very encouraging.

However, there is one thing to consider. Given the high stock-based compensation, the company may prefer issuing new shares (dilution) over debt - if there is a need to raise the money in the near future.

After considering a range of factors, we're pretty relaxed about its cash burn since the company seems to be in a good position to continue to fund its growth. Taking an in-depth view of risks, we've identified 2 warning signs for UiPath that you should be aware of before investing.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NYSE:PATH

UiPath

Provides an automation platform that offers a range of robotic process automation (RPA) solutions primarily in the United States, Romania, the United Kingdom, the Netherlands, and internationally.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

14 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on Oracle ·

Oracle - A Fundamental and Historical Valuation

Fair Value:US$192.594.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Maronan Metals ·

Australia’s Next Silver Giant, PEA Delivers A$377M NPV & 37% IRR on Just 22% of Resource

Fair Value:AU$21.1297.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on American Resources ·

American Resources, $263M Market Cap + 19% ReElement Stake, From Coal to Critical Minerals

Fair Value:US$557.0% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

60 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative