Advertisement

- United States

- /

- Software

- /

- NYSE:ORCL

Is Oracle (ORCL) Fairly Priced After Recent Share Pullback?

Reviewed by Bailey Pemberton

- If you are wondering whether Oracle's current share price reflects its true worth, you are not alone. The stock has been on many investors' watchlists as they reassess what counts as fair value.

- Oracle shares last closed at US$149.25, with returns of 5.6% over the past week, a 9.3% decline over 30 days, a 23.7% decline year to date and a 6.9% decline over 1 year, set against gains of 72.4% over 3 years and 121.5% over 5 years.

- Recent news coverage has focused on Oracle's role as a major software and cloud infrastructure provider, including its position in large scale enterprise systems and data management. This attention helps explain why shorter term moves can differ from the longer term record, as investors reassess expectations and risks.

- On our framework, Oracle earns a valuation score of 3 out of 6. The sections that follow will walk through what different valuation methods say about that score, before finishing with a broader way to think about what "fair value" really means for you as a shareholder.

Approach 1: Oracle Discounted Cash Flow (DCF) Analysis

A DCF model estimates what a company might be worth by projecting its future cash flows and then discounting those back to today, so you can compare that value with the current share price.

For Oracle, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $2.9b. Analyst estimates and Simply Wall St extrapolations then project free cash flow out over the next decade, with the 2030 figure forecast at around $22.7b, all in $. Some of the interim years are projected to include free cash flow shortfalls and later years to show higher free cash flow, which is reflected in the discounted ten year projection path.

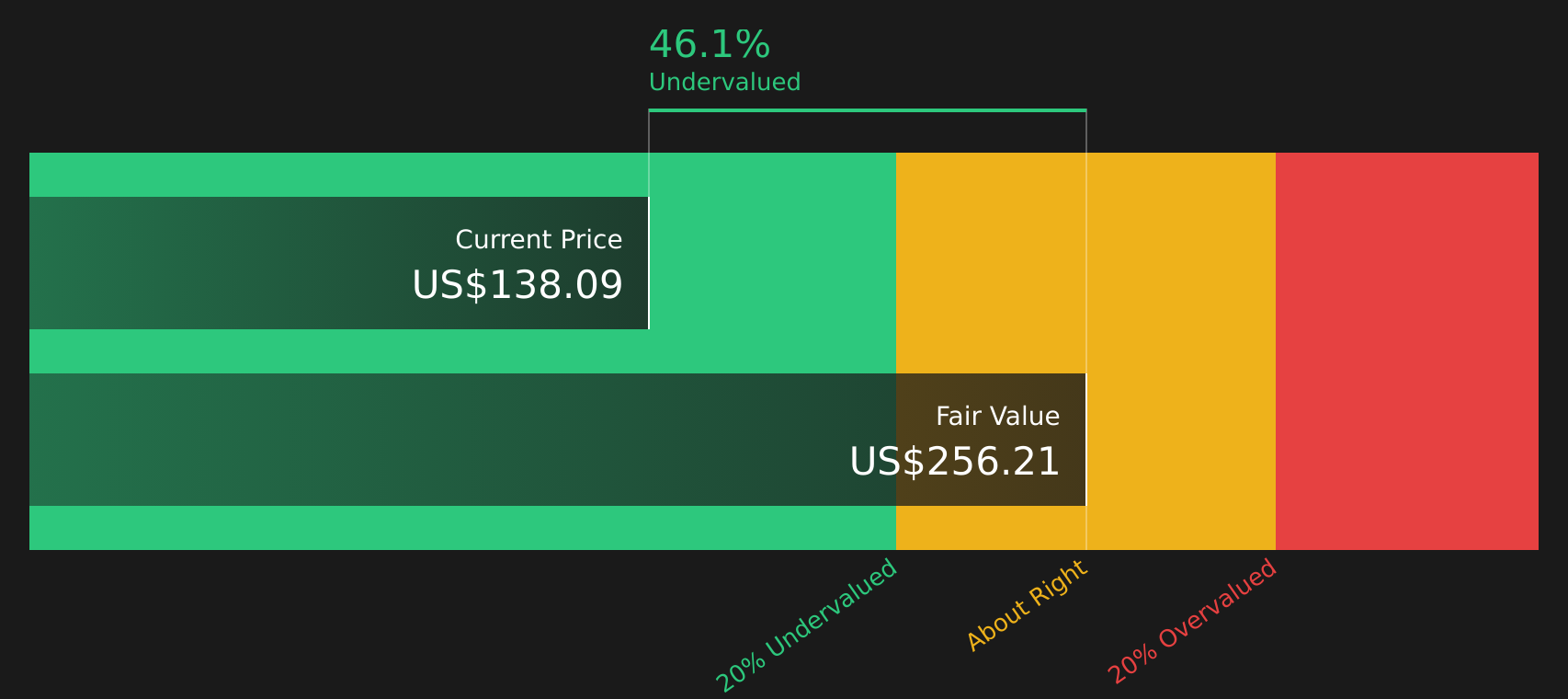

When all those future cash flows are discounted back, the DCF model arrives at an estimated intrinsic value of about $163.27 per share. Compared with the recent share price of $149.25, this implies Oracle is trading at roughly an 8.6% discount to that estimate, so the model suggests the shares are close to fair value with a modest margin.

Result: ABOUT RIGHT

Oracle is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Oracle Price vs Earnings

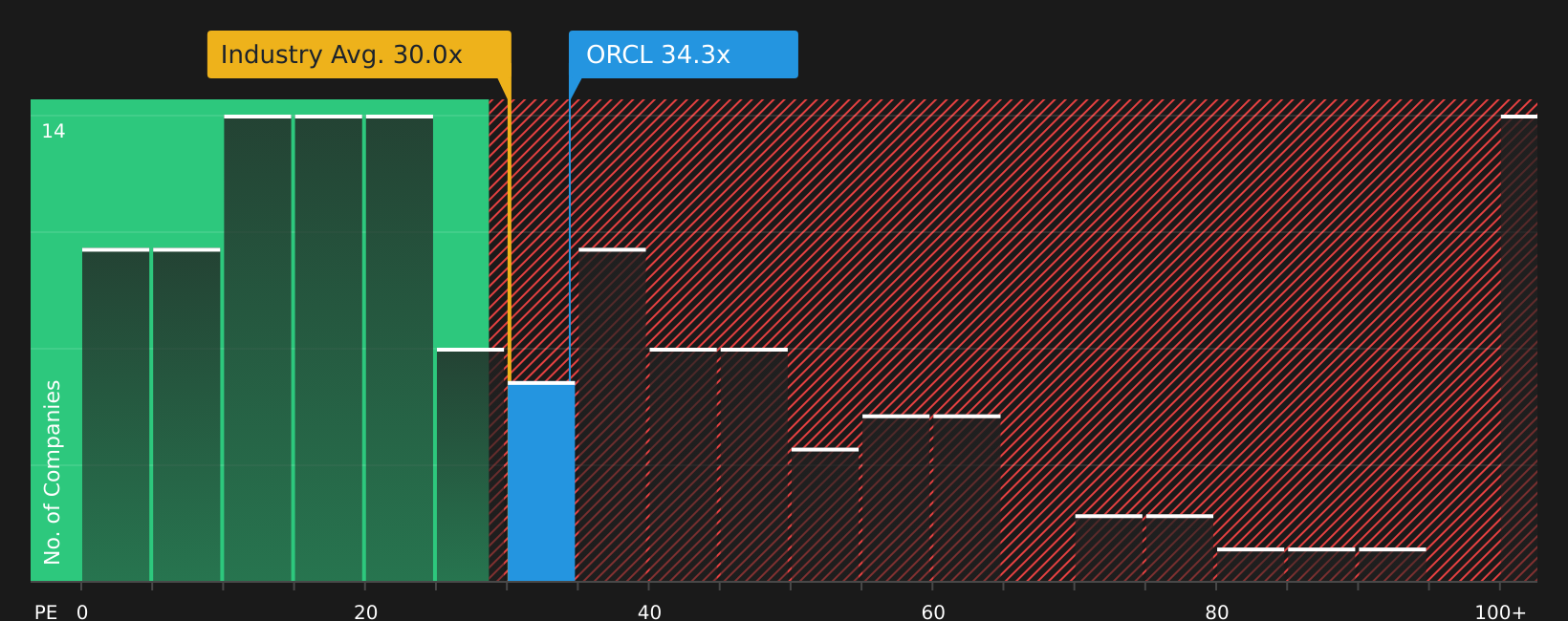

For a profitable company like Oracle, the P/E ratio is a useful cross check on the DCF work because it ties the share price directly to the earnings the business is currently generating.

What counts as a “normal” P/E depends on how quickly investors expect earnings to grow and how much risk they see in those earnings. Higher expected growth and lower perceived risk can justify a higher P/E, while slower growth or higher risk usually mean a lower multiple is more reasonable.

Oracle currently trades on a P/E of 27.8x, compared with the Software industry average of 26.4x and a peer group average of 54.4x. Simply Wall St also calculates a proprietary “Fair Ratio” for Oracle of 55.3x, which is the P/E that would be expected given factors like its earnings growth profile, industry, profit margins, market cap and key risks.

This Fair Ratio is a more tailored yardstick than a simple industry or peer comparison, because it adjusts for Oracle specific characteristics rather than assuming every software company should trade on the same multiple. With the current P/E of 27.8x well below the Fair Ratio of 55.3x, this framework suggests the shares may be undervalued on an earnings basis.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Oracle Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce Narratives, which are simple stories you create around a company that tie your view of its future revenue, earnings and margins to a forecast and a fair value, then compare that to the current share price to help you decide whether it looks attractive or stretched.

On Simply Wall St, Narratives live on the Community page and are easy to use, allowing you to set your own assumptions while the platform handles the forecasts, fair value estimate and automatic updates when new information such as earnings reports or major news arrives.

With Oracle, for example, one Narrative on the platform currently assigns a fair value of about US$170.68 per share while another uses much more optimistic assumptions and arrives at around US$400 per share. This shows how two investors looking at the same company can reach very different, yet structured, conclusions about what they think the shares are worth.

Do you think there's more to the story for Oracle? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ORCL

Oracle

Offers products and services that address enterprise information technology environments worldwide.

Exceptional growth potential and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

77 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

28 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8166.9% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

DE

DeathSmiIes on New Horizon Aircraft ·

HORIZON AIRCRAFT (HOVR)

Fair Value:US$2084.3% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

berkdnd on Yeo Teknoloji Enerji Ve Endustri Anonim Sirketi ·

Yeo Teknoloji Enerji için hedef fiyat analizi

Fair Value:₺152.726.4% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Janpeo on Stellantis ·

IA Analysis

Fair Value:€1140.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

113 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.8% undervalued

1194 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

28 likesusers have liked this narrative