Advertisement

- United States

- /

- Software

- /

- NYSE:ORCL

Does Mythics' Multi‑Cloud Move Clarify Oracle's (ORCL) Enterprise AI Strategy Or Complicate It?

Reviewed by Sasha Jovanovic

- In early December 2025, Mythics announced expanded support for Oracle’s multi-cloud strategy, enabling Oracle AI Database services to run across Google Cloud, Microsoft Azure, Amazon Web Services, and Oracle Cloud Infrastructure to help enterprises modernize infrastructure and integrate AI across environments.

- At the same time, large AI infrastructure collaborations and very large, multi‑year cloud contracts with partners such as OpenAI have intensified analyst focus on Oracle’s growing AI backlog, rising debt load, and its push to become a leading provider of enterprise AI computing power.

- We’ll now examine how Mythics’ expanded multi‑cloud support for Oracle AI Database reshapes Oracle’s investment narrative around enterprise AI adoption.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Oracle Investment Narrative Recap

To own Oracle today, you need to believe its huge AI and cloud backlog can be converted into profitable revenue without overextending the balance sheet. The key near term catalyst remains evidence of sustainable, diversified AI demand in upcoming earnings, while the biggest risk is heavy spending and leverage tied to a small number of hyperscale AI customers. Mythics’ expanded multi cloud support helps Oracle’s AI Database show up where customers already run workloads, but does not materially change that core risk reward trade off.

The most relevant recent announcement is Oracle’s nearly US$500 billion in contracted AI related deals, including the US$300 billion OpenAI collaboration and other hyperscale agreements. Against that backdrop, Mythics’ move to run Oracle AI Database across AWS, Azure, Google Cloud, and OCI speaks directly to the main catalyst: turning that backlog into live, multi cloud enterprise AI workloads at scale.

Read the full narrative on Oracle (it's free!)

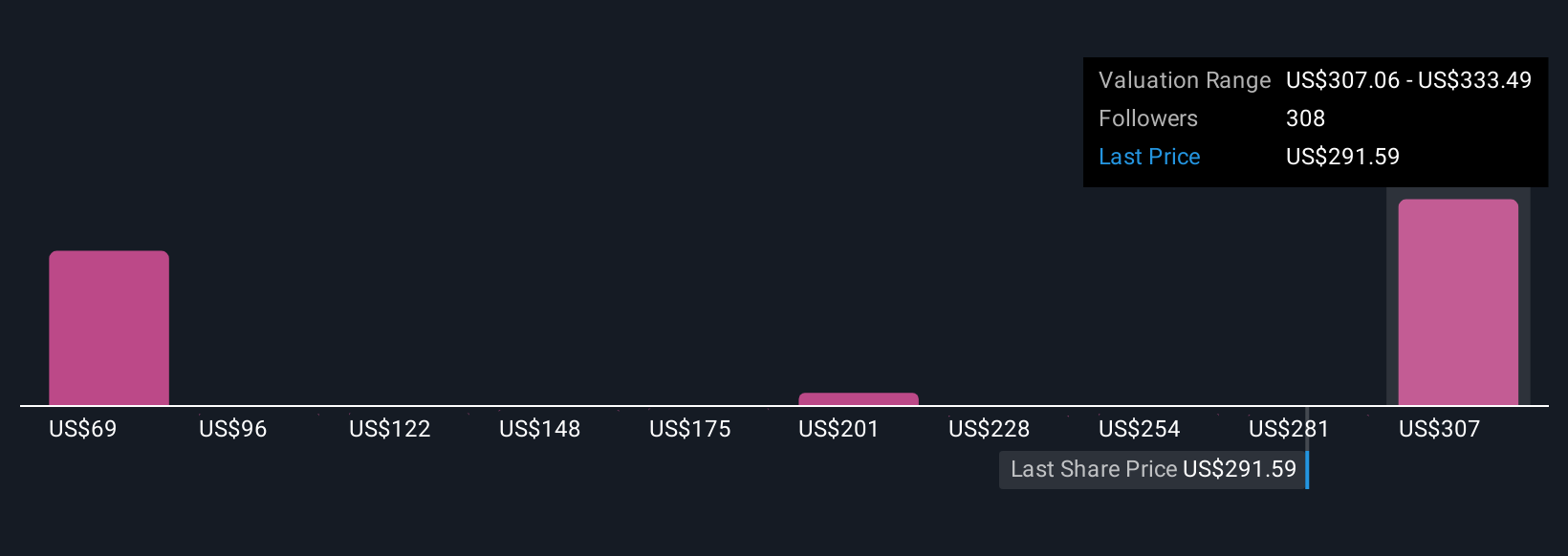

Oracle's narrative projects $99.5 billion revenue and $25.3 billion earnings by 2028. This requires 20.1% yearly revenue growth and about a $12.9 billion earnings increase from $12.4 billion today.

Uncover how Oracle's forecasts yield a $342.28 fair value, a 57% upside to its current price.

Exploring Other Perspectives

Yet while enthusiasm is high, investors should also be aware of how concentrated AI demand and heavy capex could impact Oracle if growth expectations shift...

Simply Wall St Community members have 26 distinct fair value estimates for Oracle, ranging from US$170.68 to US$389.81, underscoring how far apart views can be. Set against this, the reliance on massive AI infrastructure demand from a few headline customers raises important questions about how robust those long term expectations really are.

Explore 26 other fair value estimates on Oracle - why the stock might be worth as much as 79% more than the current price!

Build Your Own Oracle Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Oracle research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Oracle research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Oracle's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ORCL

Oracle

Offers products and services that address enterprise information technology environments worldwide.

Exceptional growth potential and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$466.3% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9720.3% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1927.6% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.252.0% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7071.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TH

TheInternationalInvestor on Scicom (MSC) Berhad ·

I Found a Hidden Quality Compounder in a Kuala Lumpur Vinyl and Vibes Lounge

Fair Value:RM 2.9541.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.252.0% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.8% undervalued

116 followersusers have followed this narrative

2 commentsusers have commented on this narrative

33 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.1% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6120.0% undervalued

1193 followersusers have followed this narrative

7 commentsusers have commented on this narrative

35 likesusers have liked this narrative