- United States

- /

- IT

- /

- NYSE:KD

Kyndryl Holdings (NYSE:KD) Partners With Virginia DMV For Cloud Modernization Project

Reviewed by Simply Wall St

Kyndryl Holdings (NYSE:KD) announced a collaboration with the Virginia DMV to modernize its systems, which likely contributed to its share price rising 22% last month. During the same period, the company also made key leadership appointments and continued its share buyback program, potentially reinforcing investor confidence. Meanwhile, the overall market saw little change and remained flat as anticipation built around Nvidia's earnings. Kyndryl's initiatives, such as migrating critical applications to a cloud-native system and achieving an earnings turnaround with a reported net income of $68 million, might have provided added momentum against the broader market's stable trend.

We've spotted 2 possible red flags for Kyndryl Holdings you should be aware of.

Kyndryl Holdings' partnership with the Virginia DMV and recent leadership changes are poised to influence its long-term growth narrative positively. These strategic moves, alongside ongoing modernization initiatives such as cloud-native migrations and AI implementations, potentially bolster both revenue and earnings projections. The anticipated boost in confidence among investors may also be attributed to the company's robust three-year total shareholder return of very large, underscoring a significant increase despite currency volatility and execution risks. Over the past year, Kyndryl's stock performance surpassed the US IT industry, which returned 32.3%, highlighting its resilience and growth trajectory within a competitive landscape.

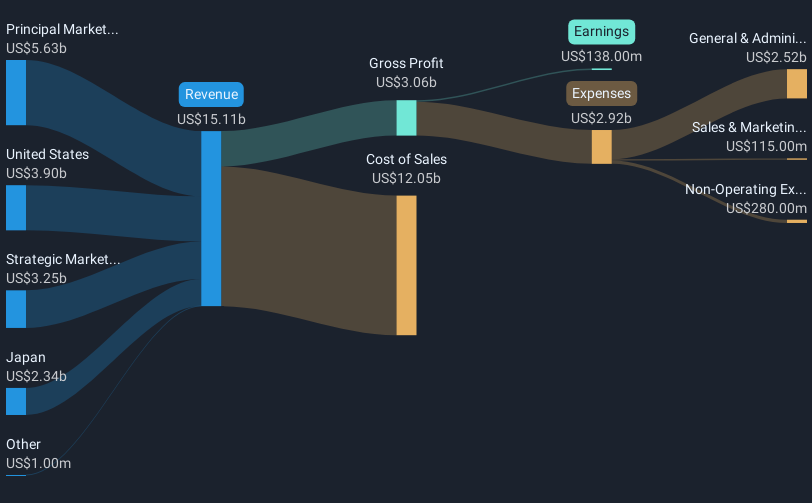

The recent surge in Kyndryl's share price must be considered in light of the analysts' consensus price target of approximately US$43.15, against the current share price around US$32.64. This represents a potential upside of 24.4%, assuming revenue grows to US$15.6 billion and earnings reach US$844 million by 2028. The collaboration with Microsoft, AWS, and Google could significantly impact these forecasts by driving revenue growth and increasing profit margins. The emphasis on IT modernization positions Kyndryl as a key player amid macroeconomic challenges, though ongoing cost increases, particularly related to IBM software, remain a headwind that could temper earnings expectations. Overall, these developments suggest a promising trajectory for Kyndryl, warranting close attention to its future market positioning and financial performance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Kyndryl Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KD

Kyndryl Holdings

Operates as a technology services company and IT infrastructure services provider in the United States, Japan, and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)