Advertisement

- United States

- /

- Software

- /

- NYSE:HUBS

Is AI-Driven Subscription Growth Changing the Investment Case for HubSpot (HUBS)?

Simply Wall St

Reviewed by Simply Wall St

- In the second quarter of 2025, HubSpot reported a 19% year-over-year increase in subscription-based revenues and added more than 9,700 net new customers, bringing its total customer count to 267,982, up 18% from the prior year.

- The company’s integration of AI features across its product suite drove significant growth in seat upgrades, including a very large increase in Sales Hub and Service Hub seat upgrades compared to the previous year.

- We'll look at how AI-driven product adoption and strong customer growth impact HubSpot's future business outlook and growth narrative.

Find companies with promising cash flow potential yet trading below their fair value.

HubSpot Investment Narrative Recap

To be a HubSpot shareholder, you need to believe in the company's ability to drive recurring revenue through strong customer growth and steady adoption of its expanding AI-powered product suite. The recent surge in subscription revenues and new customers is encouraging, yet it does not fully address the key short-term catalyst, whether AI-based features can deliver sustained upgrades and higher spend amidst intensifying competition. The main risk remains pressure on customer acquisition costs and pricing as more competitors innovate and challenge HubSpot’s value proposition.

Among the recent announcements, the launch of HubSpot’s deep research connector with ChatGPT stands out as particularly relevant. This capability is directly tied to the company’s strategy of AI-led adoption, offering customers more advanced data insights, which supports the current narrative of AI driving seat upgrades and deeper product engagement. Whether these features can continue to attract paying users will be central to HubSpot’s near-term performance.

By contrast, investors should be aware that heightened competition among SaaS and emerging AI-first platforms could begin to...

Read the full narrative on HubSpot (it's free!)

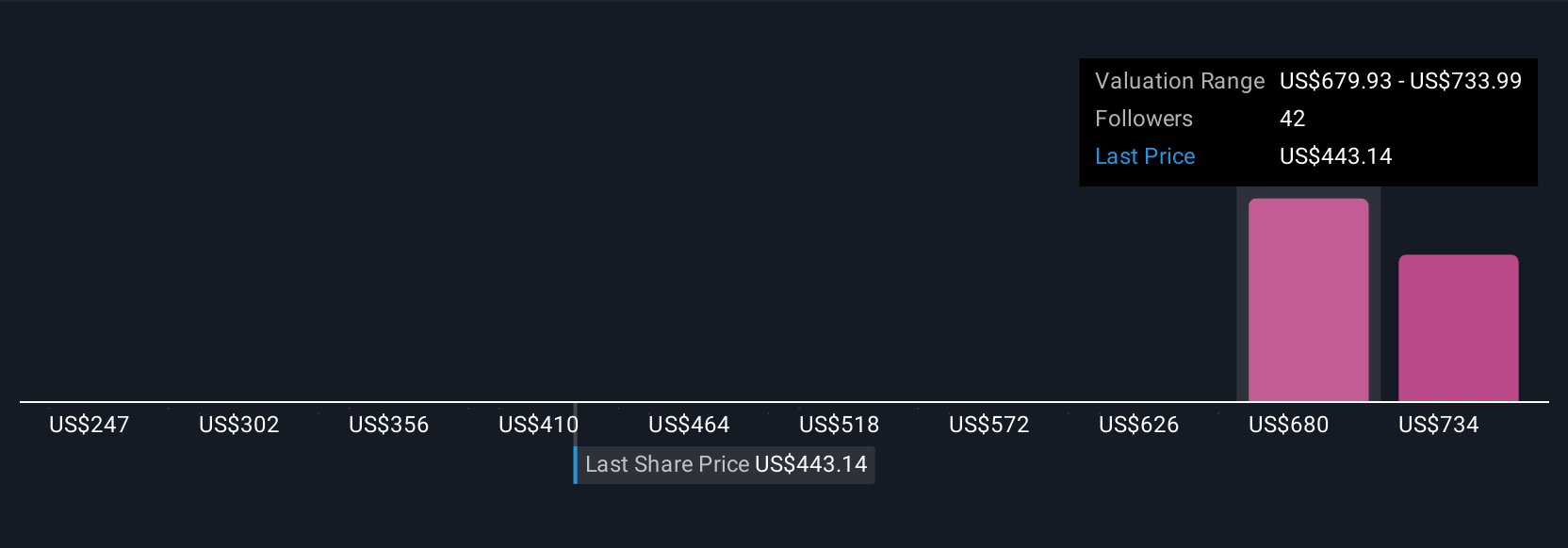

HubSpot's narrative projects $4.6 billion in revenue and $388.4 million in earnings by 2028. This requires 17.1% yearly revenue growth and a $400.3 million earnings increase from the current $-11.9 million.

Uncover how HubSpot's forecasts yield a $695.33 fair value, a 46% upside to its current price.

Exploring Other Perspectives

Five separate Simply Wall St Community fair value estimates for HubSpot range widely from US$407 to US$792, revealing strong differences in how growth prospects are modeled. While many see upside, customer acquisition costs and pricing pressure remain concerns for future profit potential, so be sure to consider these varied viewpoints before making your own assessment.

Explore 5 other fair value estimates on HubSpot - why the stock might be worth 15% less than the current price!

Build Your Own HubSpot Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your HubSpot research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free HubSpot research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate HubSpot's overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HubSpot might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HUBS

HubSpot

Provides a cloud-based customer relationship management (CRM) platform for businesses in the Americas, Europe, and the Asia Pacific.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor