Advertisement

- United States

- /

- Software

- /

- NYSE:FIG

Assessing Figma (FIG) Valuation After Unusual Options Activity And Recent Price Slide

Options activity and price slide put Figma (FIG) in the spotlight

Unusual options trading around Figma (FIG), combined with a recent share price drop and mixed analyst ratings, has pushed the design software company onto many investors radar this week.

See our latest analysis for Figma.

The recent options activity comes during a sharp reset in sentiment. The share price is at $27.07 after a 16.35% decline over 7 days and a 49.26% decline over 90 days, indicating that momentum has been fading rather than building in the short term.

If Figma’s swings have your attention, it may be a useful moment to broaden your watchlist and look at other high growth tech and AI names using high growth tech and AI stocks.

With the stock around $27 and an average analyst target of $56, plus rapid revenue and net income growth alongside heavy losses, the key question is simple: is this a genuine opportunity or is future growth already priced in?

Price to sales of 13.8x: Is it justified?

On a P/S of 13.8x at a last close of $27.07, Figma trades at a premium that stands out against both peers and the wider software space.

P/S looks at how much investors are paying for each dollar of revenue and is often used for high growth software companies that are still loss making. For Figma, the question is whether its current revenue profile and growth outlook support a valuation that high.

Simply Wall St’s checks flag that FIG is expensive on this measure compared with a peer average P/S of 7.1x, and an even lower 4.5x for the broader US Software industry. That is a wide gap, which suggests the market is pricing in stronger revenue growth or a better long term margin profile than is implied for many competitors.

Compared with the industry benchmark, the 13.8x P/S multiple is more than triple the sector average of 4.5x. This is a clear sign investors are paying a premium for exposure to Figma’s product suite and growth story. Whether that premium holds will likely depend on how closely future revenue trends track existing forecasts and how quickly losses narrow relative to those peers.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price to sales of 13.8x (OVERVALUED)

However, heavy losses of US$926.099 million, along with any slowdown in revenue growth or renewed pressure on high growth tech valuations, could quickly challenge that premium story.

Find out about the key risks to this Figma narrative.

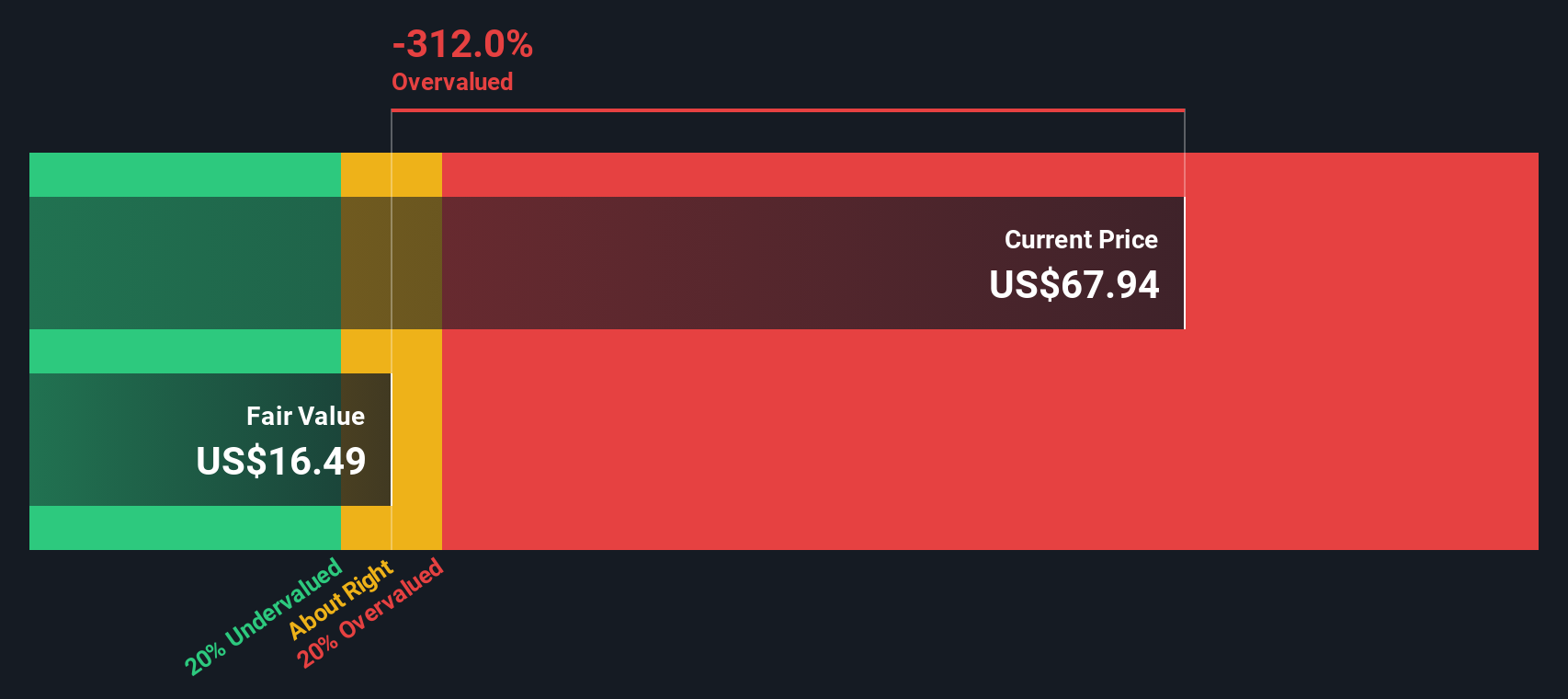

Another view using our DCF model

While the 13.8x P/S ratio suggests Figma is expensive against peers, our DCF model points in the same direction. It estimates future cash flow value at US$19.63 per share, compared with the current US$27.07 price, implying the stock is overvalued on this second yardstick too. If both methods lean the same way, what would need to change in the story for that to shift?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Figma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 878 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Figma Narrative

If you look at this and come to a different conclusion, or prefer to dig into the numbers yourself, you can shape your own view in minutes with Do it your way.

A great starting point for your Figma research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Figma is on your radar, do not stop there. Widen your opportunity set by scanning for other themes and business models that might better fit your goals.

- Spot potential value early by reviewing these 3533 penny stocks with strong financials that pair low share prices with solid underlying numbers and clear financial footing.

- Target the front line of machine learning by running through these 23 AI penny stocks that connect artificial intelligence with real revenue and business traction.

- Prioritise price discipline by focusing on these 878 undervalued stocks based on cash flows that trade below what their cash flows suggest they could be worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FIG

Figma

Develops and sells a collaborative, browser-based platform for designing, prototyping, building digital experiences, and subscriptions for access to its platform.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

69 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

9 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8210.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

5 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

69 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative