- United States

- /

- IT

- /

- NYSE:EPAM

Will AI-Led Growth and Analyst Upgrade Change EPAM Systems' (EPAM) Investment Narrative?

Reviewed by Simply Wall St

- In August 2025, EPAM Systems reported fiscal second quarter results that exceeded analyst expectations and raised its full-year revenue growth forecast, supported by AI-led solutions and modernization initiatives.

- The company's recent delivery restructuring and a three-quarter streak of organic revenue acceleration prompted TD Cowen to upgrade its analyst rating, highlighting EPAM's renewed focus on sales execution and client expansion.

- We’ll examine how EPAM’s momentum in AI-led revenue growth and recent upgrade could reshape its long-term investment narrative.

AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

EPAM Systems Investment Narrative Recap

To be comfortable as an EPAM Systems shareholder, I believe one needs confidence in the company's ability to sustain growth through enterprise adoption of AI and modernization services. The recent results and analyst upgrade confirm momentum in AI-led revenue and sales execution, supporting a key near-term catalyst. However, margin recovery remains the biggest risk, as wage inflation and talent competition could persist; the latest update does not materially reduce this concern.

Of the recent announcements, EPAM's expanded generative AI partnership with AWS closely aligns with current growth drivers highlighted by analysts. This collaboration reinforces EPAM’s positioning at the intersection of cloud migration and enterprise AI, supporting potential revenue acceleration while customers increase reliance on transformation expertise.

Yet, in contrast to this AI-driven momentum, wage inflation and competition for engineers continue to be risks that investors should be aware of if...

Read the full narrative on EPAM Systems (it's free!)

EPAM Systems' outlook forecasts $6.5 billion in revenue and $582.4 million in earnings by 2028. This implies an 8.8% annual revenue growth and a $181.2 million increase in earnings from the current $401.2 million.

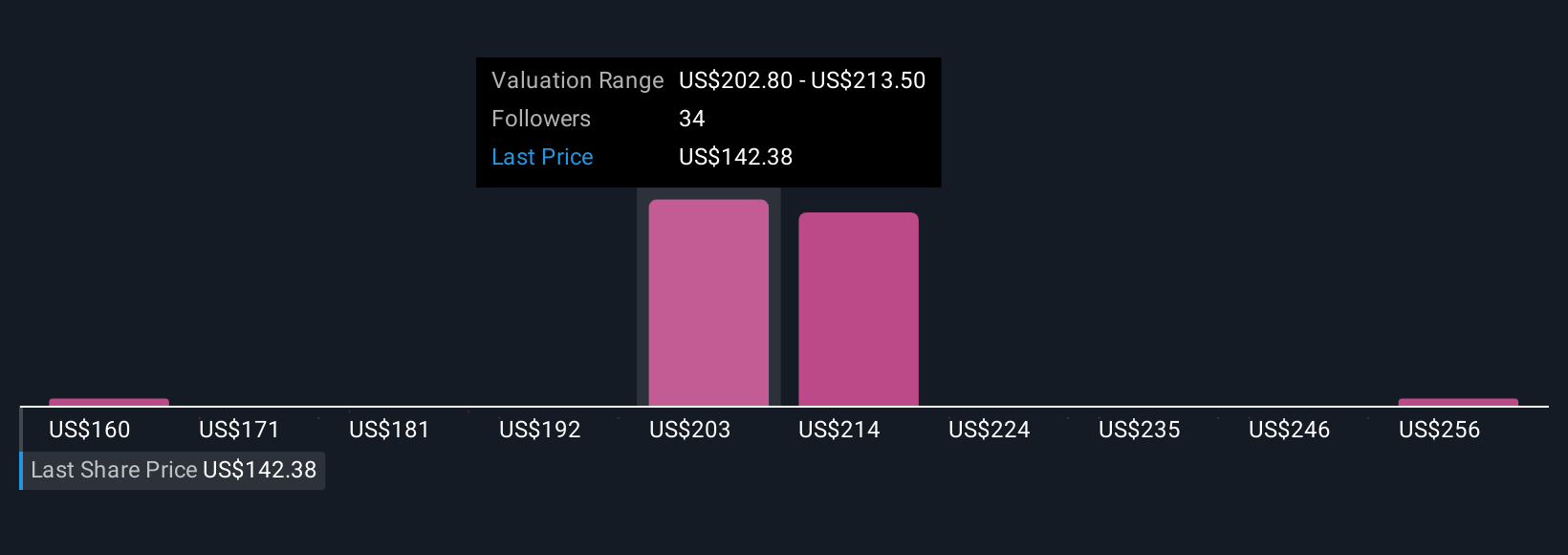

Uncover how EPAM Systems' forecasts yield a $212.69 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community span US$160 to US$267 per share, showing a wide spectrum of outlooks. While AI solutions fuel new growth opportunities, the persistent margin pressures from wage inflation may weigh on future performance and are top of mind for many participants.

Explore 6 other fair value estimates on EPAM Systems - why the stock might be worth 9% less than the current price!

Build Your Own EPAM Systems Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your EPAM Systems research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free EPAM Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EPAM Systems' overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Outshine the giants: these 23 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if EPAM Systems might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EPAM

EPAM Systems

Provides digital platform engineering and software development services worldwide.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)