Advertisement

- United States

- /

- IT

- /

- NYSE:EPAM

EPAM Systems (EPAM): Exploring Valuation After Analyst Upgrade and Strong AI-Driven Results

Reviewed by Simply Wall St

EPAM Systems (NYSE:EPAM) is back in the spotlight after reporting quarterly results that beat forecasts, powered by strong demand for AI-focused services and digital modernization. The company also gave its outlook a lift, projecting annual revenue growth of 13% to 15%. Adding to the momentum, EPAM received an analyst upgrade to ‘Buy’, highlighting how three straight quarters of faster organic revenue and its completed post-Ukraine restructuring have changed the conversation for both investors and clients.

The news has injected some new energy into a stock that has seen mixed performance over the past year. EPAM’s return for the year sits at about -10%, and longer-term holders are still in the red over three and five years. However, the past month has delivered a 17% gain, suggesting that the market is starting to see potential as the company accelerates in its core and emerging business lines. There is an undercurrent of shifting risk perceptions here, with improvements in sales execution and expanding margins getting recognition even as sector challenges remain.

With the share price rallying on upgraded expectations, the key question for investors is whether EPAM Systems still trades at an attractive valuation or if the market is already pricing in the next phase of growth.

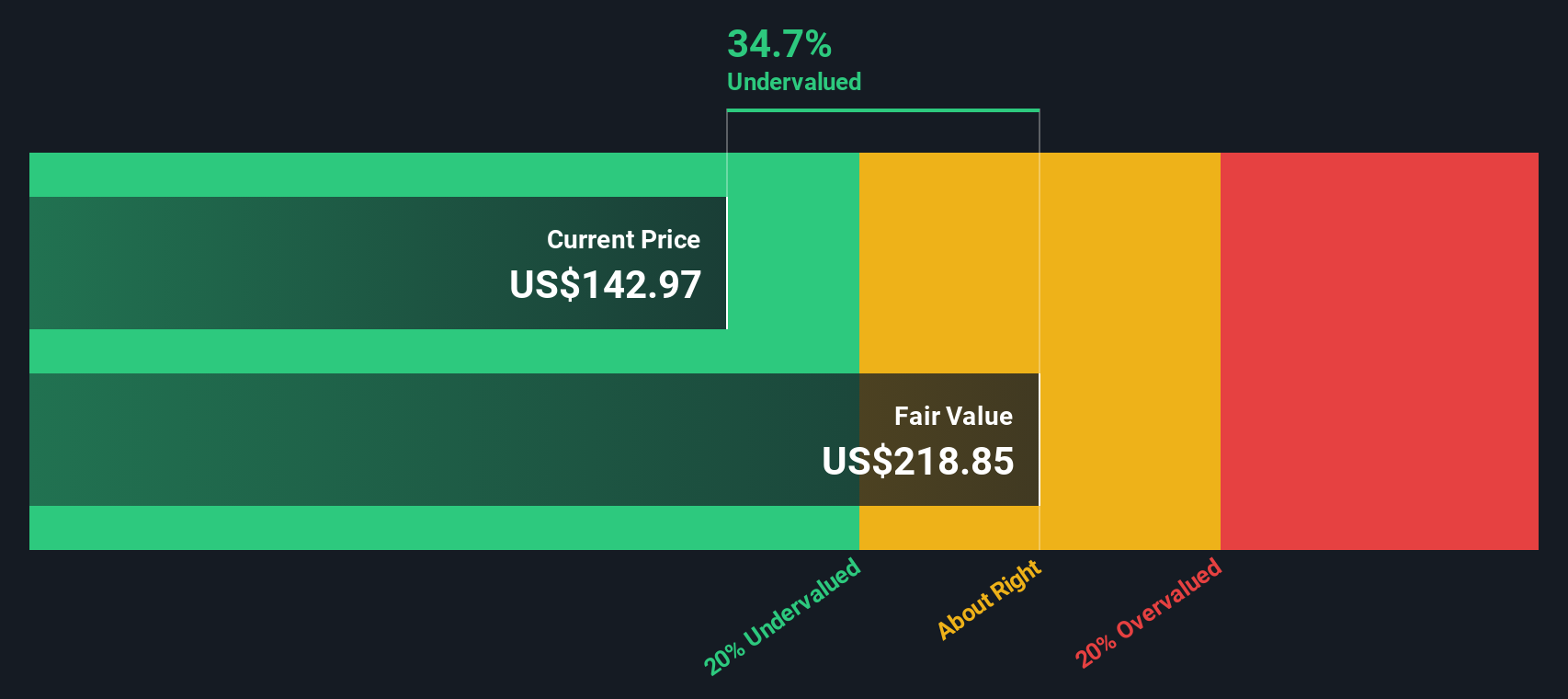

Most Popular Narrative: 17% Undervalued

According to the most widely followed narrative, EPAM Systems is currently considered undervalued. Analysts expect a multi-year earnings expansion, with the company's share price trading well below consensus fair value based on future growth projections.

"EPAM's strategic investments in AI-native services, proprietary platforms (such as DIAL and AI/RUN), and upskilling of over 80% of its workforce have positioned it as a transformation partner for clients moving beyond pilot AI programs to large-scale deployments. This supports sustainable revenue growth and the potential for improved net margins as EPAM moves up the value chain."

Want to know what’s fueling the narrative that EPAM is poised for a rebound? Most valuation models hinge on bold projections about future revenues and profits, as well as a shifting mix of business lines. Curious which assumptions justify a double-digit discount to fair value? Find out which surprising financial forecasts are powering this bullish consensus.

Result: Fair Value of $212.69 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, rising automation and persistent wage inflation could threaten EPAM’s margins. These factors could potentially challenge the bullish outlook if these headwinds intensify.

Find out about the key risks to this EPAM Systems narrative.Another View: Our DCF Model

Taking a different approach, our SWS DCF model also suggests EPAM might be undervalued by looking at future cash flows instead of focusing solely on earnings multiples. Does this second check strengthen the bullish case, or does it raise new questions?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out EPAM Systems for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own EPAM Systems Narrative

If you’d rather rely on your own analysis or simply want a second opinion, it’s easy to craft a personal perspective in under three minutes. Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding EPAM Systems.

Looking for more investment ideas?

Why stop at one winner? Take your strategy up a notch and put your watchlist to work with three standout opportunities you won’t want to overlook.

- Unlock high-yield potential by checking out top companies delivering reliable income with attractive returns using our handpicked dividend stocks with yields > 3%.

- Tap into emerging breakthroughs by seeking out trends in medical innovation and patient care advancements with our leading healthcare AI stocks.

- Get ahead of the curve with future-focused companies at bargain prices, each featured in the smart undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EPAM Systems might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NYSE:EPAM

EPAM Systems

Provides digital platform engineering and software development services worldwide.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7065.0% undervalued

42 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.2% undervalued

46 followersusers have followed this narrative

8 commentsusers have commented on this narrative

16 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0541.3% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.0% undervalued

91 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.3% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$907.3243.6% undervalued

36 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

JA

Janpeo on Space Exploration Technologies ·

The trap for retailers that can evaporate more than 80% of the value.

Fair Value:US$28.55463.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.4% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.5% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1931.2% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative