Advertisement

- United States

- /

- IT

- /

- NYSE:DAVA

Endava plc's (NYSE:DAVA) Most Important Factor To Consider

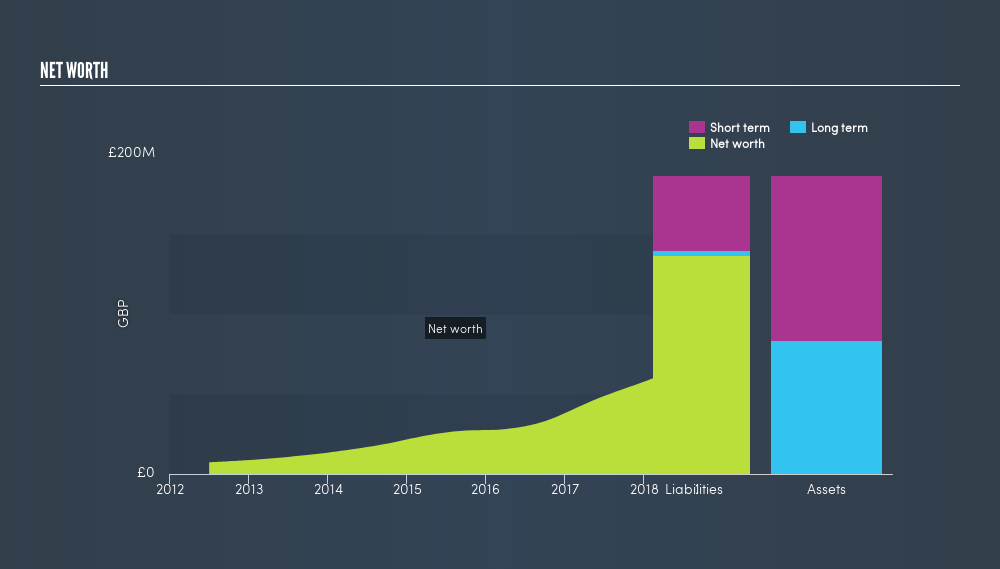

Two important questions to ask before you buy Endava plc (NYSE:DAVA) is, how it makes money and how it spends its cash. After investment, what’s left over is what belongs to you, the investor. This also determines how much the stock is worth. Today we will examine Endava’s ability to generate cash flows, as well as the level of capital expenditure it is expected to incur over the next couple of years, which will result in how much money goes to you.

See our latest analysis for Endava

Is Endava generating enough cash?

Endava generates cash through its day-to-day business, which needs to be reinvested into the company in order for it to continue operating. What remains after this expenditure, is known as its free cash flow, or FCF, for short.

There are two methods I will use to evaluate the quality of Endava’s FCF: firstly, I will measure its FCF yield relative to the market index yield; secondly, I will examine whether its operating cash flow will continue to grow into the future, which will give us a sense of sustainability.

Free Cash Flow = Operating Cash Flows – Net Capital Expenditure

Free Cash Flow Yield = Free Cash Flow / Enterprise Value

where Enterprise Value = Market Capitalisation + Net Debt

Along with a positive operating cash flow, Endava also generates a positive free cash flow. However, the yield of 1.84% is not sufficient to compensate for the level of risk investors are taking on. This is because Endava’s yield is well-below the market yield, in addition to serving higher risk compared to the well-diversified market index.

What’s the cash flow outlook for Endava?

Another important consideration is whether this return is likely to be maintained over the next couple of years. We can gauge this by looking at Endava’s expected operating cash flows. Over the next two years, a double-digit growth in operating cash of 44% is expected. The future seems buoyant if Endava can maintain its levels of capital expenditure as well. Below is a table of Endava’s operating cash flow in the past year, as well as the anticipated level going forward.| Current | +1 year | +2 year | |

|---|---|---|---|

| Operating Cash Flow (OCF) | UK£32m | UK£30m | UK£46m |

| OCF Growth Year-On-Year | -5.9% | 53% | |

| OCF Growth From Current Year | 44% |

Next Steps:

Given a low free cash flow yield, on the basis of cash, Endava becomes a less appealing investment. This is because you would be better compensated in terms of cash yield, by investing in the market index, as well as take on lower diversification risk. However, cash is only one aspect of investing. Now you know to keep cash flows in mind, I recommend you continue to research Endava to get a better picture of the company by looking at:

- Valuation: What is DAVA worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether DAVA is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Endava’s board and the CEO’s back ground.

- Other High-Performing Stocks: If you believe you should cushion your portfolio with something less risky, scroll through our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:DAVA

Endava

Provides technology services in North America, Europe, the United Kingdom, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.563.5% undervalued

49 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.826.3% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23055.3% overvalued

53 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

LI

Lijo on Accenture ·

A value stock that's undervalued.

Fair Value:US$18326.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Rox Resources ·

Developer to Producer: Debt-Free Path, A$965M Post-Tax NPV, and Massive Gold Leverage

Fair Value:AU$6.1693.3% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

JO

John_Eric on MercadoLibre ·

MercadoLibre and the Spreadsheet Trick That Decides Everything

Fair Value:US$4.72k60.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.8% undervalued

86 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5448.2% undervalued

60 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7107.2% undervalued

53 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative