- United States

- /

- Software

- /

- NYSE:CRM

Salesforce (CRM) Declares US$0.42 Per Share Quarterly Dividend

Reviewed by Simply Wall St

Salesforce (CRM) recently reaffirmed its commitment to shareholder value with a quarterly dividend and continued to build investor confidence through robust Q2 earnings results, showing impressive revenue and net income growth. The dividend announcement, coupled with a $20 billion increase in buyback authorization, reflects the company's strategic focus on rewarding shareholders. Despite these positive moves, Salesforce's stock remained largely flat over the past month, in line with broader market trends. This stability might also derive from the modest overall performance of major indexes, despite recent fluctuations in bond yields and rate-cut speculations.

Buy, Hold or Sell Salesforce? View our complete analysis and fair value estimate and you decide.

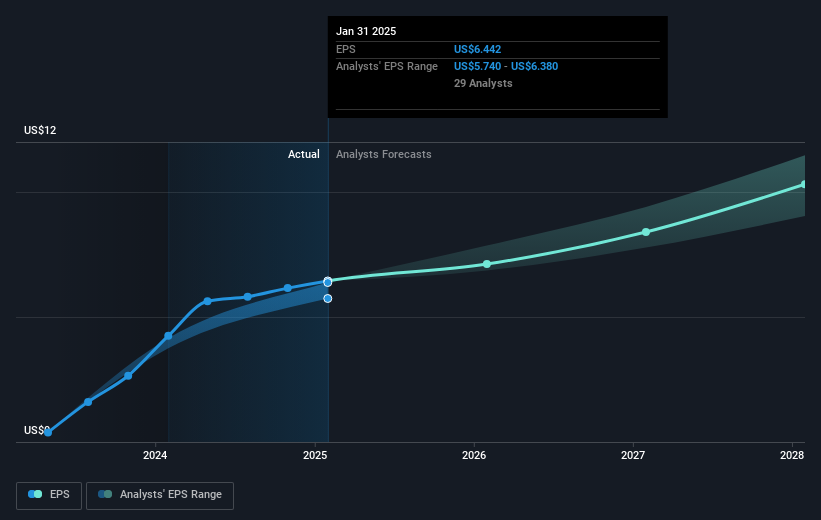

The recent reaffirmation of Salesforce's commitment to shareholder rewards through dividends and a robust buyback program supports the company's narrative of enhancing long-term shareholder value. Over the past three years, Salesforce's total return, including share price gains and dividends, was 55.58%, underscoring solid long-term performance against the backdrop of an evolving technology sector. However, over the past year, Salesforce has underperformed the US Software industry, which returned 29.3%, reflecting broader market dynamics and specific challenges faced by the company.

Despite its substantial return over three years, Salesforce's shares remain below the consensus price target of $334.97, trading at a discount of approximately 33.6%. This price target hinges on analysts' expectations of revenue reaching $50.8 billion and earnings of $10.2 billion by 2028. The recent news, highlighting Salesforce's intensified focus on AI-driven automation and digital transformation, could potentially bolster revenue and earnings, aligning closer with these forecasts. However, moving from current earnings of $6.66 billion requires navigating competition and regulatory challenges. Furthermore, the commitment to returning cash to shareholders reflects confidence in Salesforce's earnings trajectory, potentially supporting near-term valuation improvements.

Dive into the specifics of Salesforce here with our thorough balance sheet health report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CRM

Salesforce

Provides customer relationship management technology that connects companies and customers together worldwide.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)