- United States

- /

- Software

- /

- NYSE:CRM

Is Salesforce's Valuation Attractive After Refusing Hackers’ Ransom Demand?

Reviewed by Bailey Pemberton

Trying to make sense of Salesforce stock these days? You’re not alone. After all, this is a company that’s gone through just about every kind of headline you can imagine lately, from headline-grabbing AI launches to the kind of data breach drama that can give investors pause. If you bought in years ago, you might still be sitting on a 71.7% gain over three years, but the past year has probably tested your patience, with shares down 15.6%. Year-to-date, it’s been even rougher, dropping 26.9%. Yet, there are glimmers of resilience too. This week, Salesforce managed a modest 0.5% uptick that hints some buyers still have faith, even with the stock about flat over the last month.

So what’s really behind these moves? Partly, it’s the narrative. Recent news of Salesforce refusing to yield to a hacker’s ransom demand could be stirring up concern over risk, but it also signals confidence in their security posture. Meanwhile, dramatic staff changes and the big push into AI, like the launch of Missionforce, show a company greasing the wheels for long-term growth, even if not every headline wins over Wall Street right away.

A lot of investors are asking the same question: Is Salesforce undervalued given all these moving parts, or is there more pain ahead? Here’s where the numbers start to matter. Based on a value score of 4 out of 6, Salesforce passes several key valuation tests, which we’ll break down next. But stick around, because we’re going to look at these traditional valuation approaches, and then dig into an even smarter way to decide what Salesforce is really worth.

Why Salesforce is lagging behind its peers

Approach 1: Salesforce Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow, or DCF, model estimates the intrinsic value of a stock by projecting its future cash flows and then discounting those projections back to their present value. This approach tries to answer the question: if you could receive all the company’s expected future free cash flows today, what would that be worth?

For Salesforce, the latest reported Free Cash Flow is $12.4 billion. According to analyst forecasts, cash flow is expected to grow steadily, reaching approximately $16.98 billion by 2030. While analyst estimates typically extend only five years out, projections beyond that are extrapolated with growth estimates to help round out a ten-year forecast.

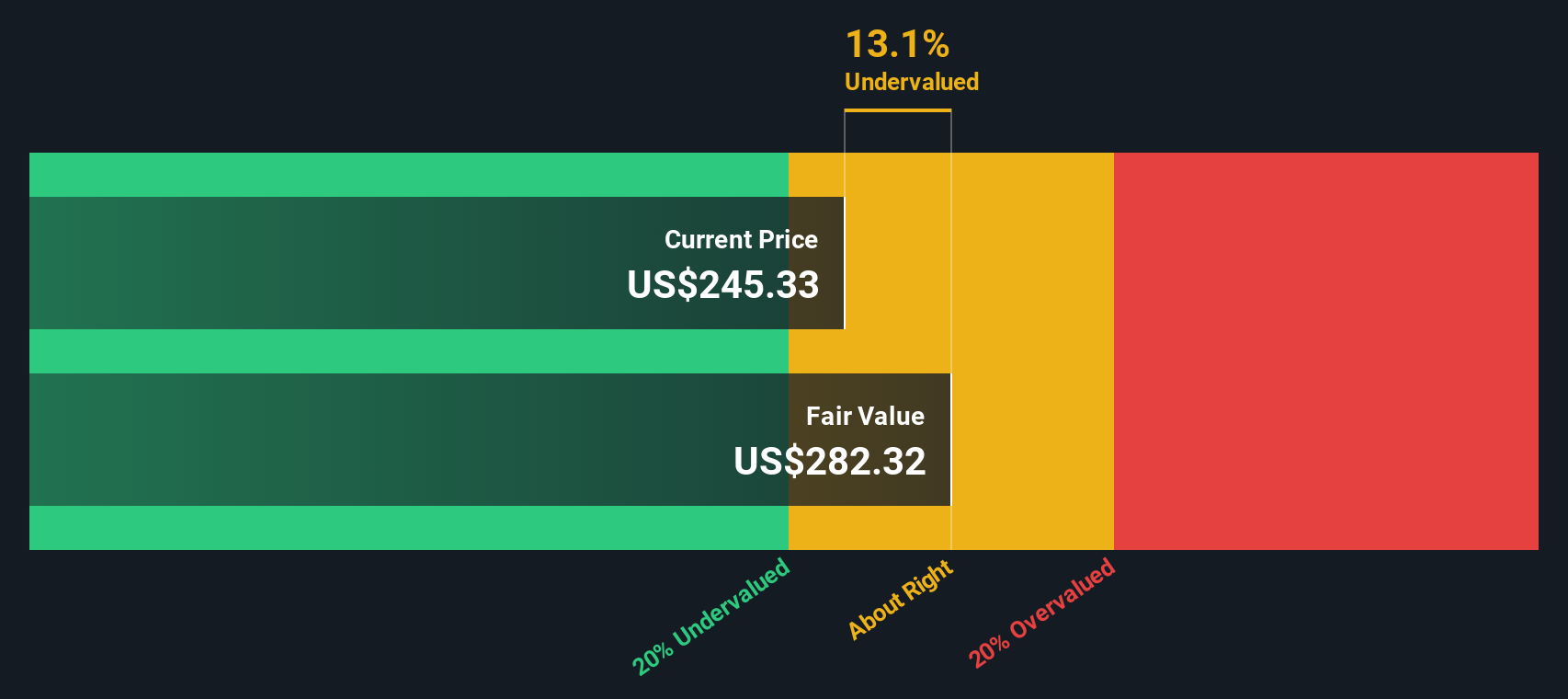

Using the 2 Stage Free Cash Flow to Equity model, the DCF analysis estimates Salesforce’s fair value at $282.48 per share. This figure is about 14.4% above the company’s current share price, suggesting the stock is undervalued based on cash flow potential.

For investors, this indicates that the market may not be fully pricing in Salesforce’s long-term capacity to generate cash, especially as the company continues investing for future growth.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Salesforce is undervalued by 14.4%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Salesforce Price vs Earnings

The Price-to-Earnings (PE) ratio is one of the most widely used valuation measures for profitable companies like Salesforce. It gives investors a quick sense of how much they’re paying for each dollar of the company’s earnings. The usefulness of the PE ratio rests on the idea that higher growth companies can command higher multiples, while more mature or riskier businesses tend to trade at lower PE ratios.

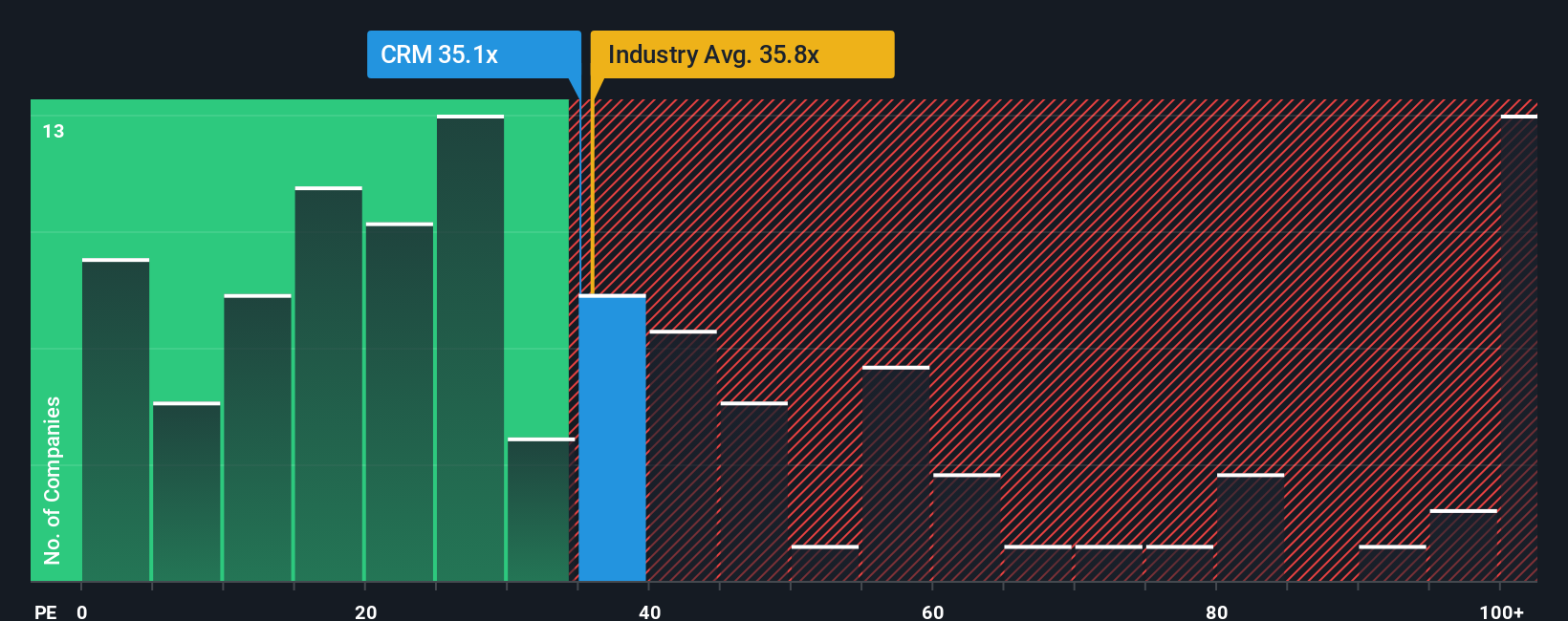

Currently, Salesforce trades at a PE ratio of 34.5x. For comparison, the average PE in the software industry is 34.8x, and Salesforce’s peer group averages an even loftier 57.8x. On paper, Salesforce looks cheaper than many of its direct peers but is roughly in line with the broader sector.

To dig deeper, Simply Wall St calculates a “Fair Ratio,” which is a proprietary version of the PE multiple that reflects not just sector averages but also company specifics such as earnings growth outlook, profit margins, risk factors, and market cap. The Fair Ratio for Salesforce currently stands at 44.2x. Unlike a simple peer or industry comparison, this view is tailored precisely to Salesforce’s fundamentals and risk profile, making it a more reliable reference point for valuation.

With Salesforce’s actual PE of 34.5x sitting notably below its Fair Ratio of 44.2x, the stock appears undervalued on an earnings multiple basis. Investors may be getting Salesforce’s growth potential at a relative discount compared to what its fundamentals suggest is fair value.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Salesforce Narrative

Earlier we mentioned that there’s an even better way to understand valuation, so let’s introduce you to Narratives, a feature that connects a company’s story with financial forecasts in a single, dynamic view. A Narrative is your investment perspective: you define what you believe Salesforce will achieve in terms of future growth, profit, and fair value, supported by your own reasoning and assumptions behind those numbers.

This approach transforms stock picking from pure number-crunching into a more powerful, accessible process. Rather than just relying on historical data or analyst estimates, Narratives let you combine your view of Salesforce’s strategy, risks, and opportunities with a built-in fair value calculation. Narratives are easy to create and compare, are hosted on Simply Wall St’s Community page (used by millions), and update automatically when new company news or earnings data arrives. This gives you a real-time sense of whether your investment thesis still holds up.

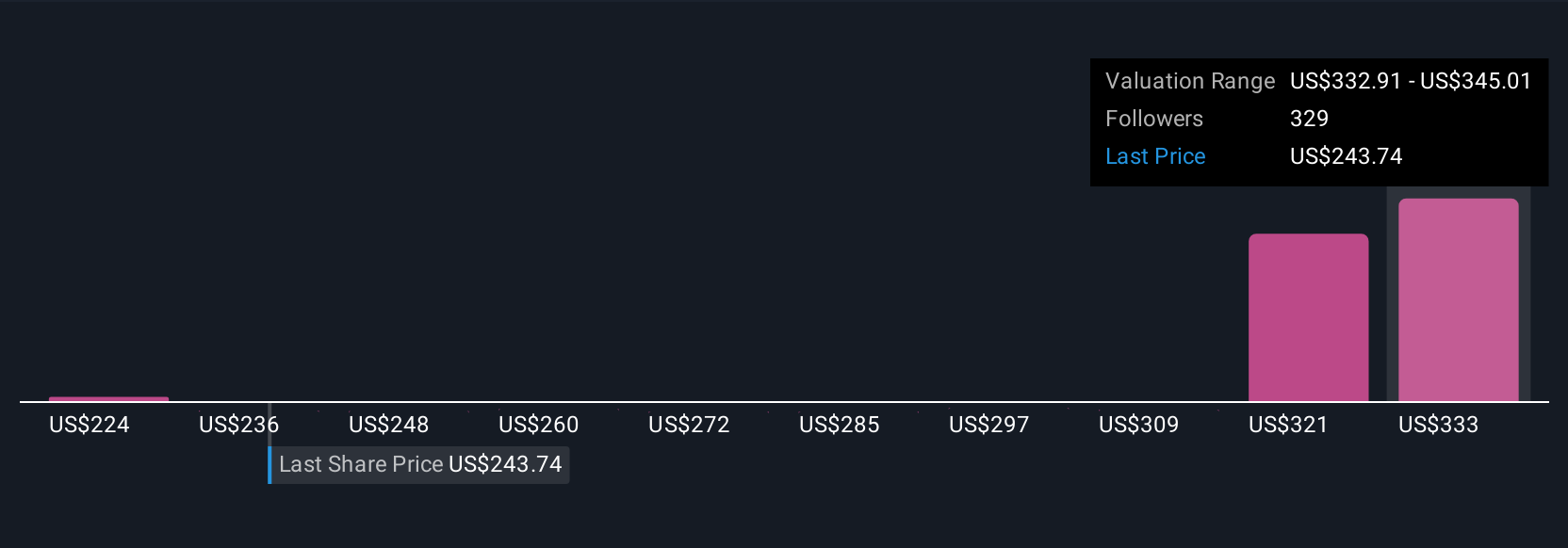

For example, one Salesforce Narrative might forecast aggressive AI-fueled growth and peg fair value at $430 per share, while a more skeptical investor, wary of market saturation and competition, sees $221 as fair. This provides a clear side-by-side benchmark you can use to evaluate your own stance and decide when Salesforce is a buy (current price below your fair value) or a sell (price above your fair value).

For Salesforce, however, we'll make it really easy for you with previews of two leading Salesforce Narratives:

Fair Value: $334.68

24% undervalued versus current price

Forecast Revenue Growth: 9.6%

- AI-driven automation and workflow integration are deepening customer adoption and paving the way for sustained revenue and margin growth.

- Success in mid-market and SMB segments, coupled with ongoing operating discipline and capital returns, is supporting scalable profitability.

- Key risks include regulatory challenges, integration risk from acquisitions, and intensifying competition from hyperscalers and large technology companies.

Fair Value: $223.99

8% overvalued versus current price

Forecast Revenue Growth: 13.0%

- Salesforce’s leadership is solid in enterprise cloud, but high market expectations may be difficult to meet given market saturation and already-realized efficiency gains.

- Concentration in large enterprise customers exposes the company to volatility if not offset by new growth opportunities or diversification.

- While AI adoption and acquisitions may drive future growth, they also bring potential pressure on free cash flows and margin sustainability as competition intensifies.

Do you think there's more to the story for Salesforce? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CRM

Salesforce

Provides customer relationship management technology that connects companies and customers together worldwide.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)