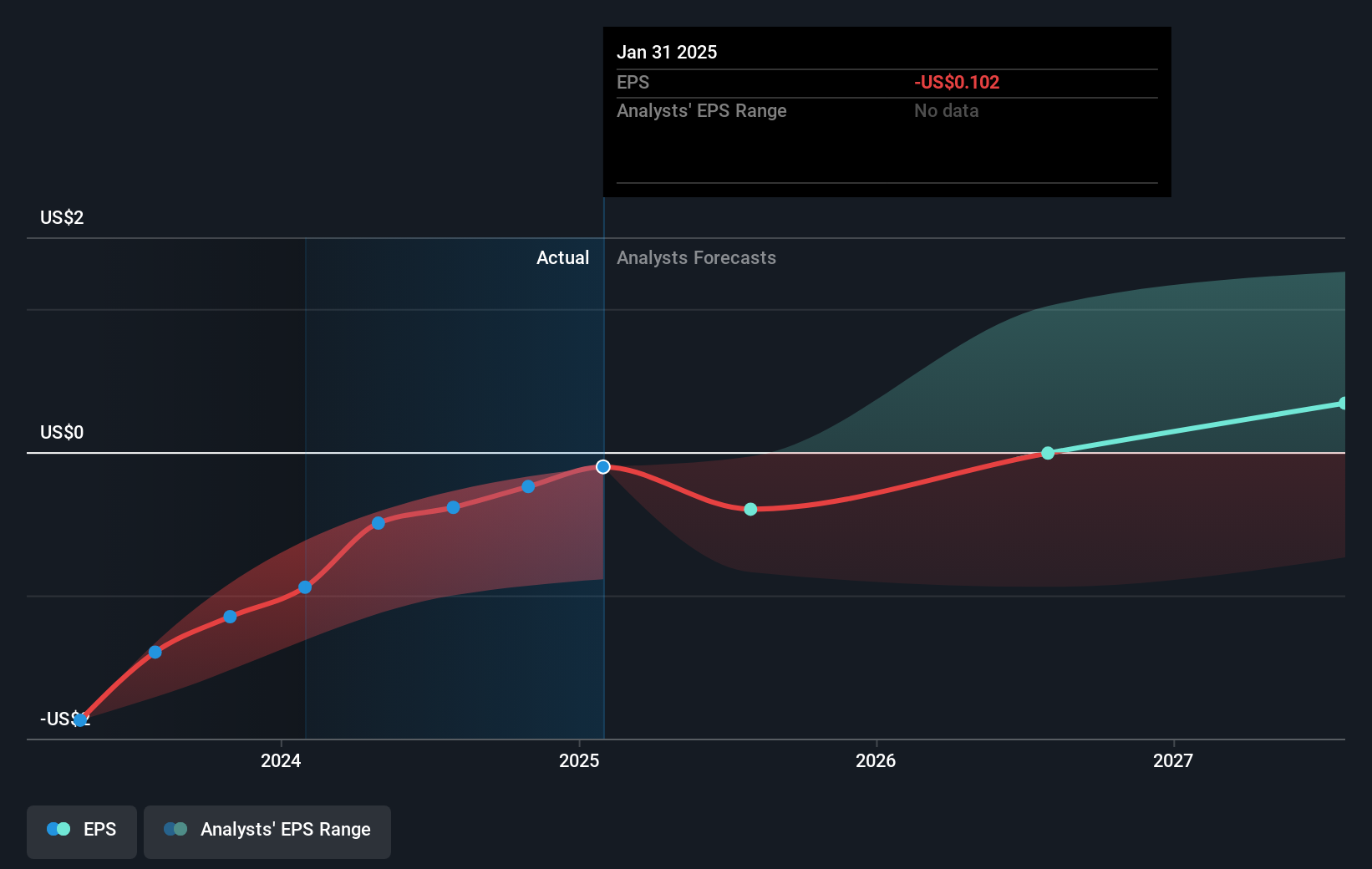

Zscaler, Inc. (NASDAQ:ZS) is possibly approaching a major achievement in its business, so we would like to shine some light on the company. Zscaler, Inc. operates as a cloud security company worldwide. The US$39b market-cap company’s loss lessened since it announced a US$58m loss in the full financial year, compared to the latest trailing-twelve-month loss of US$16m, as it approaches breakeven. The most pressing concern for investors is Zscaler's path to profitability – when will it breakeven? Below we will provide a high-level summary of the industry analysts’ expectations for the company.

Consensus from 43 of the American Software analysts is that Zscaler is on the verge of breakeven. They anticipate the company to incur a final loss in 2026, before generating positive profits of US$29m in 2027. So, the company is predicted to breakeven approximately 2 years from now. What rate will the company have to grow year-on-year in order to breakeven on this date? Using a line of best fit, we calculated an average annual growth rate of 40%, which is rather optimistic! Should the business grow at a slower rate, it will become profitable at a later date than expected.

Given this is a high-level overview, we won’t go into details of Zscaler's upcoming projects, though, take into account that generally a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

See our latest analysis for Zscaler

One thing we would like to bring into light with Zscaler is its relatively high level of debt. Generally, the rule of thumb is debt shouldn’t exceed 40% of your equity, which in Zscaler's case is 71%. A higher level of debt requires more stringent capital management which increases the risk around investing in the loss-making company.

Next Steps:

This article is not intended to be a comprehensive analysis on Zscaler, so if you are interested in understanding the company at a deeper level, take a look at Zscaler's company page on Simply Wall St. We've also compiled a list of important aspects you should further examine:

- Valuation: What is Zscaler worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether Zscaler is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Zscaler’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Zscaler might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:ZS

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)